Ratemaking is the process of establishing rates or prices for insurance products. Most actuaries regard this task as being focused on the estimation of future losses, loss adjustment expense, and various other expenses associated with the provision of coverage. Profit is usually treated as an additional expense loading, with little debate about how large this loading should be and only rather vague requirements that it should be “reasonable.” Profit is something of an afterthought in this view.[1] To an economist this approach would seem very odd. Economists generally assume that firms set prices so as to maximize profits. The level of profit that results is a function of pricing and market conditions. In economic terms, the standard actuarial provision for profit is perhaps best thought of as a specification of the economic concept of “normal profit,” introduced by Marshall (1920) and sometimes called the opportunity cost of capital. While economists may view normal profit as a minimum necessary threshold rate for participation in a market, and often as an equilibrium outcome of competitive behavior in a market, it would be extremely unusual for an economist to set a price simply by summing expenses and adding a “normal profit” rate.[2] This article will show one good reason why this is the case, for it shows that in a simple economic model of an insurance sale, the standard actuarial approach not only would fail to generate additional profit that the insurers could enjoy in equilibrium but actually would lead to the insurers’ making less than their target profit rate![3]

Modeling profit maximization in the context of insurance sales is complicated by the fact that most insurance sales are in some important respects unique. Individual clients seeking insurance have unique risk characteristics, and ratemaking is often bespoke to each client. This kind of situation is not well represented by standard neoclassical economic models of competition in which there are usually assumed to be a large number of buyers seeking to buy very similar products.[4] The competitive environment in a typical insurance sale is better modeled as an auction, in which the insurance buyer chooses the low bidder among insurers who issue bids, or quotes, for the business. In this article, I will look at a type of auction known as a first-price sealed bid procurement auction. I will show that what is known about this type of auction is hugely important in insurance.

The history of auctions is long and varied. Herodotus (1862) reports their use by Babylonian traders in the fifth century B.C.E. The ancient Romans used them widely, and on one occasion, in A.D. 193, the Praetorian Guard actually sold the position of Emperor in an auction. The unlucky winner, Didius Julianus, was assassinated shortly after his proclamation and before he could make good on his promised payment, which was about $2 billion in modern terms (see Gibbon 1776). Auctions faded somewhat in popularity between the fall of the Roman Empire and a return to prominence in the seventeenth and eighteenth centuries. Their subsequent growth has been huge, and the twentieth century saw the price record set by Didius Julianus finally surpassed. Exactly when it was surpassed is difficult to say since it begs the question of what exactly an auction is, and that is more subtle than it might first appear. Many types of auctions have been used at various times, and it is hard to see what they have in common other than that they are all processes mediated by an auctioneer, who may be a buyer or seller, to buy or sell goods or services by encouraging competing bids. In recent decades, the study of auctions has developed out of game theory into an organized field of its own within economics called auction theory.[5] The initial growth of auction theory was due to the work of a handful of economists, among whom William Vickrey, Robert Wilson, Paul Milgrom, Roger Myerson, and Eric Maskin have been awarded Nobel Prizes in Economics. Subsequent growth was driven by practical successes in the 1990s and 2000s as auction theorists got involved in the design of some actual and extremely successful auctions, notably the UK government’s auction of five 3G licenses in 2000, which ultimately raised a total of $34 billion (about 2.5% of UK gross national product at the time). The use of auction theory has become widespread in the design and monitoring of many kinds of auctions in many industries. Auction theorists are now frequently employed in sales of large items as diverse as mineral rights, radio spectrum, and entire companies. They commonly are involved in the design of auctions used in online marketplaces to sell a huge variety of smaller items. They also are involved in the design of procurement auctions, wherein instead of a seller’s looking for the highest revenue from a range of potential buyers, a buyer looks for the lowest cost from a range of potential sellers. Procurement auctions are themselves common in a variety of industries such as shipbuilding, construction, information technology, and insurance. In most of these industries, auction theoretic analysis is now commonplace—but not in insurance. In insurance, a buyer or the buyer’s agent sets out a desired level of coverage and then invites different insurance companies to bid for the business by issuing quotes. Clearly, very many insurance sales can be characterized as procurement auctions. Nonetheless, to my knowledge, auction theory has so far made very limited inroads into the analysis of insurance sales.

This article begins the process of applying auction theory to the mechanisms of insurance sales, explaining how its role should combine with traditional actuarial and underwriting methods of pricing insurance. I first describe a few common situations in the sale of insurance that are procurement auctions and compare correct bidding strategies derived from auction theory with the usual actuarial approach. The basic lesson is that traditional actuarial pricing may be too aggressive, but the proper use of auction theoretic considerations can correct such bias. The article proceeds as follows. Section 1 describes a simplified example of an insurance product that is typically priced based on considerations that we would recognize as actuarial in nature, with the work being done by either actuaries or underwriters, and gives example results of the standard actuarial pricing method. Section 2 gives a brief introduction to game theory that should be sufficient to understand the game theoretic foundations of this article. Section 3 explains how the usual method by which the product described in Section 1 is sold can be described as an auction and analyzes in detail a simple example of such an auction, highlighting the differences between actuarial pricing and equilibrium bidding strategies as well as the potential shortcomings of the standard actuarial approach. Section 4 includes some conclusions and discussion of further potential applications.

1. Actuarial Pricing

The methods of analysis outlined in this article could be applied with some modifications to many if not all insurance lines and products, but for my example, I will pick a middle market commercial enterprise looking to buy statutory guaranteed-cost workers compensation coverage. I’ll assume this client is big enough to be able to provide a complex submission replete with details about loss control, past losses, the history and prospects of the business, and so forth: in other words, grist for the mill of schedule rating. However, I’ll assume the client is too small to be eligible for any large-risk alternative rating plans or retrospective rating plans (such as a large deductible or classic retro plan). I’ll assume for simplicity that the client operates in a state where all carriers use the same filed rates and rating plan and are all filed with a schedule rating plan that permits a deviation in final rate of plus or minus 25%. I’ll express calculations in terms of net rate in dollars per hundred dollars of client payroll. All these assumptions serve to keep the analysis relatively simple and easy to follow, and they are all quite plausible for a large segment of the workers compensation market and for some other commercial lines too, but I could progressively loosen all of them, if required, without sharply changing any key conclusions.

Though I’m assuming base rates are given for the example, it still may be helpful to consider the components of such rates.[6] First assume that a bureau has made base pure premium rates that equal the expected sum of discounted loss and loss adjustment expense (LAE) to be incurred per hundred dollars of earned payroll exposure, using appropriate analysis of past losses, developed and trended, and trended past exposure together with expected future loss and exposure trends and interest rates. Next, assume that each carrier has formulated a loss cost multiplier (LCM) by including the following loadings, all of which are typically expressed as fractions of final premium: other acquisition expense, commissions, general expense, premium taxes, and contingencies and profit, Assume each carrier formulates a base premium rate for the client’s class as shown in Table 1.

“Contingencies” is defined in Actuarial Standards Board (2011) as a “provision for the expected differences, if any, between the estimated costs and the average actual costs, that cannot be eliminated by changes in other components of the ratemaking process.” It can be required if another component of cost (typically loss) is estimated using techniques that result in a biased estimate. The probability distribution of aggregate loss typically has a strong right skew, and losses are commonly estimated using methods that do not adequately sample the right tail, so in many cases, a contingencies provision may be justified. I will not dwell here on the question of whether it is better in general to ensure that is an unbiased estimate or to include a separate contingencies load. It will be sufficient to note that because workers compensation bureaus generally try very hard to ensure that is an unbiased estimate of loss and LAE, it is completely reasonable to make no provision for contingencies in our example. “Profit” is the sum of underwriting profit and investment income from insurance operations. See Actuarial Standards Board (2011) for further details. Note, however, that is the only place in the standard actuarial calculation where any explicit allowance for profit is allowed.

Assume no other rating plans have any impact on the rate for this client, other than a schedule rating plan that is available for all insurers and that has symmetric maximum debits and credits of 25% of the premium base rate. The final premium that any insurer can offer to the client thus ranges between $1.50 and $2.50 per hundred dollars of payroll. It is the role of an underwriter (who in practice may be an actuary) to work confidentially for the insurer to determine the appropriate schedule rating factor between 0.75 and 1.25. For notational convenience, I will express the final premium base rate indicated by an underwriter as a sum, such as where is a continuously variable increment in the interval

I will assume that each underwriter’s assessment of the schedule-rating increment is drawn from a probability distribution on the unit interval. What I intend to represent by this is that the characteristics of the client and the underwriter and the process of schedule rating are subject to random variation and that before the process of underwriting is complete, it is reasonable to model the number that is the outcome of schedule rating as a random variable. Typically, I will assume the distribution of the increment is uniform on the unit interval. Using game theoretic terms that will be explained in the next section, I interpret an underwriter’s indicated schedule-rating increment as the signal received by the insurer in a Bayesian game in which the insurer is a player. The prior distribution of the signal will be the distribution from which the schedule-rating increment is drawn. We can think of the insurer’s decisions in the game as being made by some employee who receives a report from the underwriter.

2. Game Theory

In game theory, a game is a mathematical model of behavior between decision makers, represented as players.[7] A game can model any situation in which

-

there is a nonempty set of players (Examples with a single player are sometimes described as games, but generally speaking the set includes at least two players.);

-

each player has a set of available courses of action, or strategies (Each strategy describes what a player would do in every possible circumstance that might occur in the game.);

-

each player must choose exactly one of their available strategies;

-

the outcome of the game is determined by the players’ strategy choices; and

-

each possible outcome of the game gives a specific expected utility payoff to each player, and each player seeks to maximize their subjective expected utility (If a player is risk neutral, then outcomes can be specified as amounts of money instead of utility, and expected net revenue or profit can be used as the maximand, instead of expected utility.).

I will represent competing insurers as players maximizing their expected profit in a game. The client does not need to be represented as a separate player because the client always follows a simple rule: they take the best deal offered.

In some games, known as games with complete information, all the players know the entire structure of the game, including how many players there are, the potential action choices of each player, and their payoffs consequent on each profile of choices by the players. Auction games don’t generally fit this description. In particular, bidders typically have an indication of the value to them of the item being auctioned but are not privy to the indications possessed by other bidders. A game in which players have some private information is usually modeled by introducing an additional player called Nature, which makes a single move at the start of the game, before any other player and according to a specified probability distribution.[8] The probability distribution used by Nature is assumed to be known by the other players, but the outcome from that distribution may or may not be known. By manipulating the rest of the structure of the game, we can allow for Nature’s move to affect the other players’ payoffs, action choices, and knowledge about each other. This results in what is usually called a Bayesian game. The attributes for each player that are set by Nature’s move are known as the player’s type, and information that Nature’s move may give to a player is known as that player’s signal.

Any game can be analyzed as either a cooperative game or a noncooperative game. A cooperative game is one in which the players can make binding side agreements; in a noncooperative game, they cannot. This article is exclusively concerned with noncooperative game theory.[9]

Noncooperative game theory is concerned primarily with accurately modeling the interactions between players and their choice of strategies in equilibrium. The most important noncooperative equilibrium concepts are Nash equilibrium and its refinements. A Nash equilibrium of a game with complete information is a set of strategies, one for each player (such a mapping is often called a strategy profile), such that each player’s subjective expected utility is maximized by using their strategy in this profile if the structure of the game is common knowledge and they believe that each other player will use their strategy from this profile.[10] Since we are assuming that players seek to maximize their expected payoffs, the Nash equilibrium concept can obviously be applied to Bayesian games as well as games of complete information, whereby each player maximizes their expected payoff given their beliefs about other players’ strategy choices and also the probability of each of Nature’s moves. A Nash equilibrium of a Bayesian game is often called a Bayesian Nash equilibrium.

3. Auctions in Insurance

Among the many types of auctions studied by auction theorists, the simplest representation of most insurance sales is the first-price sealed bid procurement auction. In such an auction, each bidder submits a first and final bid amount to the auctioneer without first seeing the amounts of any other bids, though they may be aware of the number of bidders.[11] The winner is the bidder with the lowest bid, and that bidder receives the amount of the bid in exchange for providing the requested goods or services.[12] We will use “insurance auction” without qualification to refer to a first-price sealed bid auction wherein the service to be provided is some form of insurance coverage and submitting a bid is synonymous with issuing a quote.

In an insurance auction, the customer, or an agent or broker acting on the customer’s behalf, acts as the auctioneer. Since any agent who shares the same interests as the customer can be treated as one party with the customer and any agent representing an insurer can be treated as one with the insurer, this representation is not materially distinct from any other pattern of intermediation so long as each intermediary is acting solely in the interests of either the customer or some insurer. The auctioneer puts together details of a request for coverage and then solicits bids from insurers. When an insurer is approached, it first obtains a report (a signal in the terms of Section 1 before considering the totality of what it knows and issuing a quote. The strategy of the auctioneer is straightforward in my examples, and I will focus on the strategies of the insurers. I will assume that the insurers are all risk neutral. I do not need to make any assumptions about the risk preferences of the buyer, nor do my results depend in any important way on such preferences, as I am assuming their strategy is fixed.

I shall assume that the actual value of providing coverage under an insurance policy for a particular client does not vary with the covering insurer (in other words, ultimate losses and other expenses are the same, no matter which insurer writes the coverage). This means that the costs of providing coverage and the residual value (i.e., profit) to the insurer depend only on the premium charged and not on the particular insurer charging the premium. This describes what is known as a common value auction. No insurer knows, of course, when it writes a policy of insurance, what the total ultimate cost of providing the coverage will be. I will represent this amount, the sum of actual final loss and other expense from the insurance policy, as a random variable with mean Assume that, prior to considering what price to set, each insurer ’s underwriter or actuary gives it a numeric report, on the risk. This report will be represented in a Bayesian game as the insurer’s signal. The expected value of denoted can be found from a function of all the signals: the form of which function is common knowledge. If any insurer knew all the signals, then no other information available before quoting could be used by the insurer to refine its estimate of In this sense, can be considered an ideal, actuarially fair premium or “true value” for the risk. I assume that each insurer seeks to maximize the expected value of its operating profit, where there are no costs from an unsuccessful bid and operating profit equals the amount of the accepted quote less

I will now consider a simple example that uses the coverage, rate, and rating plan details given in Section 1 and analyze it as a Bayesian game. Assume that all information about the bidders, client, coverage, and auction that is not specifically described as private is declared openly and is common knowledge. Assume two insurers, and are solicited by the auctioneer and issue quotes. Each insurer receives a signal and believes that the two signals are statistically independent and uniformly distributed on the unit interval. The insurers accept that is 1.50 plus the arithmetic mean of the two insurers’ signals:

Each insurer sees only its own signal before issuing a quote. The strategy choice of each insurer is a bid function that gives the amount of its quote as a function of its signal. I will look for a symmetric Bayesian Nash equilibrium of the auction game, i.e., an equilibrium in which each insurer uses the same bid function, and to begin with, I will conjecture that the bid function of insurer is a linear function of the signal received:

\[b_{i}\left(s_{i}\right)=2.5-\alpha\left(1-s_{i}\right)\]

If this suggests that the insurers will not give “full credit” for a low-risk indication. Also, given this conjecture, I can ignore the possibility that bids will be exactly equal, the probability of which will be zero. The expected payoff to is the probability that it wins multiplied by its expected profit conditional on winning (it earns zero if it loses the auction):

\[\pi_{i}=\Pr\left(b_{i}<b_{j}\right)\left(b_{i}-E\left[v\mid s_{i},b_{i}<b_{j}\right]\right)\]

Given my conjecture about each bidder’s bid function, I obtain by substitution that:

\[\small{\pi_{i}=\Pr\left(1+\frac{b_{i}-2.5}{\alpha}<s_{j}\right)\left(b_{i}-E\left[v\mid s_{i},1+\frac{b_{i}-2.5}{\alpha}<s_{j}\right]\right)}\]

Substituting also for yields the following:

\[\small{\begin{aligned} \pi_{i} &=\Pr\left(1+\frac{b_{i}-2.5}{\alpha}<s_{j}\right)\\ & \qquad \cdot \left(b_{i}-E\left[1.5+\frac{s_{i}+s_{j}}{2}\mid s_{i},1+\frac{b_{i}-2.5}{\alpha}<s_{j}\right]\right) \end{aligned}}\]

knows its own signal, so and:

\[\small{\begin{aligned} \pi_{i} &=\Pr\left(1+\frac{b_{i}-2.5}{\alpha}<s_{j}\right)\\ & \qquad \cdot \left(b_{i}-1.5-\frac{s_{i}}{2}-\frac{1}{2}E\left[s_{j}\mid1+\frac{b_{i}-2.5}{\alpha}<s_{j}\right]\right) \end{aligned}}\]

Since a priori, we have the following:

\[\small{\pi_{i}=\left(-\frac{b_{i}-2.5}{\alpha}\right)\left(b_{i}-1.5-\frac{s_{i}}{2}-\frac{1}{2}\left(1+\frac{b_{i}-2.5}{2\alpha}\right)\right)}\]

If this bid strategy profile is indeed a Bayesian Nash equilibrium, then the payoff must be maximized with respect to the first order condition for which is

\[\frac{0.5b_{i}+4.5\alpha-2\alpha b_{i}+0.5\alpha s_{i}-1.25}{\alpha^{2}}=0\]

Solving for gives

\[b_{i}=\frac{2.5-9\alpha-\alpha s_{i}}{1-4\alpha}\]

Substituting from our conjectured relationship, and solving the quadratic gives or Looking at the form of the payoff equation makes obvious that is the value that maximizes the payoff, and substituting this back in to the conjectured bid function gives us the following:

\[b_{i}\left(s_{i}\right)=2.5-\frac{1}{2}\left(1-s_{i}\right)\]

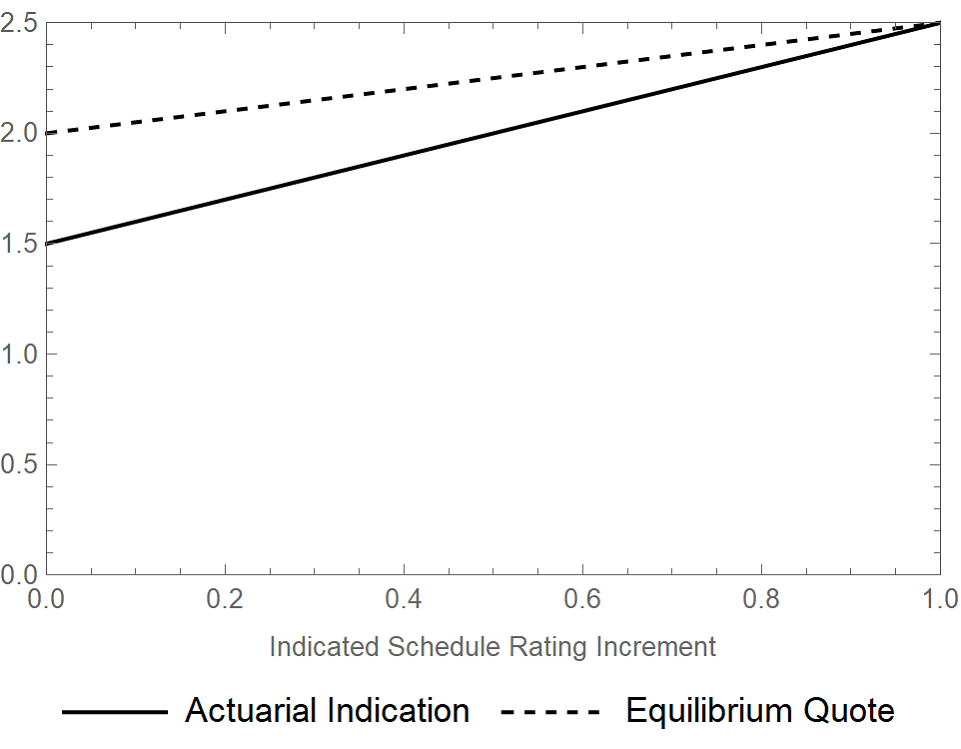

Thus, there is indeed a symmetric Bayesian Nash equilibrium of the auction game with a bid function of the conjectured form. Comparing to the direct actuarial indication, we see that the equilibrium bid amount is generally higher than the actuarially indicated quote (see Figure 1).

Substituting this bid amount and the value of back into the payoff function, I obtain each insurer’s expected payoff conditional on its own signal:

\[\pi_{i}=\frac{1}{4}\left(1-s_{i}\right)^{2}\]

Given I have and so each insurer’s unconditional expected payoff is

\[E\left[\pi_{i}\right]=\frac{1}{12}\]

The total expected payoff of the two insurers is thus Clearly, in expectation, the insurers in this equilibrium earn profit in an amount greater than zero, which is indicated by the actuaries.

I have shown that a symmetric equilibrium exists in which the insurers earn positive expected profit in expectation. Could there exist another equilibrium in which this is not the case? A key result in auction theory, called the Revenue Equivalence Theorem, describes the surprisingly large extent to which certain variations in the form of the auction game do not affect key outcomes of an auction, including the expected price paid or received by each player.[13] This can be used to show, for example, that in my example auction there are no symmetric equilibria in which the insurers each receive any other unconditional expected payoff than In fact, it can be used to show that any symmetric equilibria of many other forms of auction would produce the same result, given the assumptions I have made about the insurers, their costs, and in particular their signals’ being independent.[14]

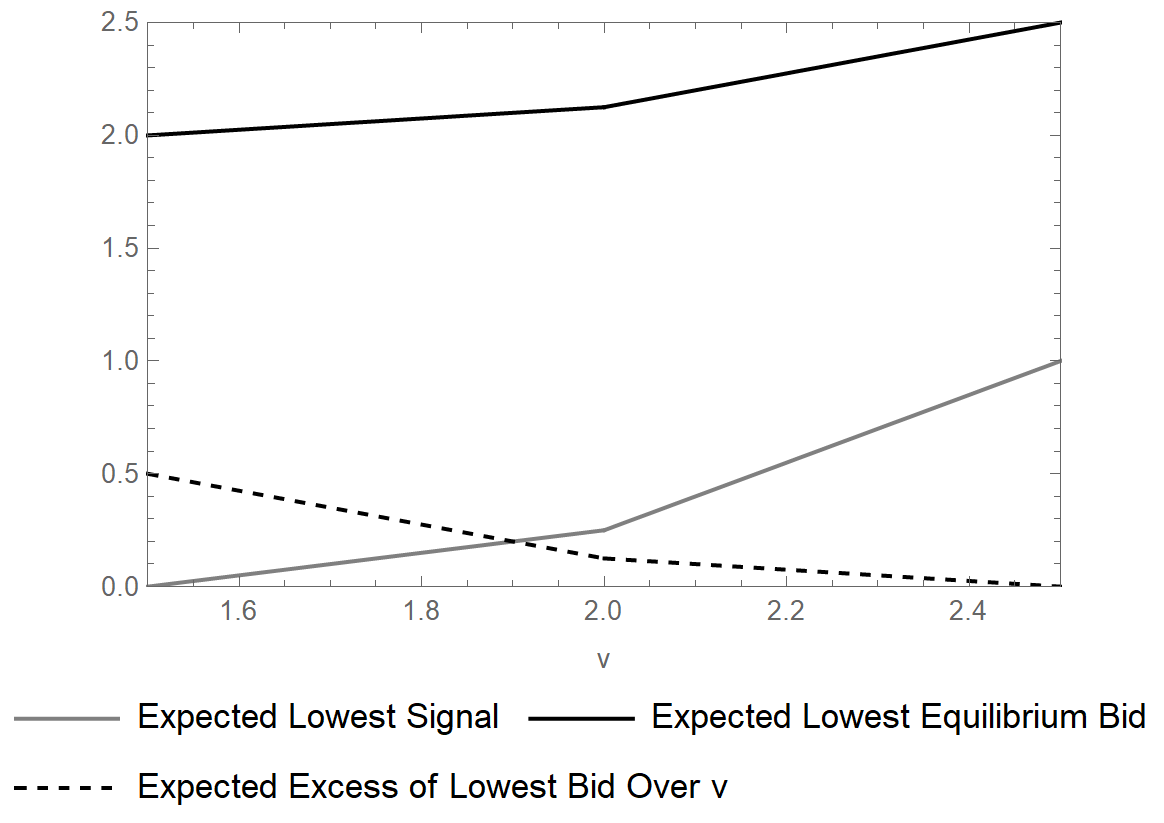

In equilibrium, the customer pays the lowest bid, which is where is the minimum of the signals. Conditional on a value for the customer, the distribution of the minimum of the signals, received by the two insurers is uniform, on the interval: if or if We thus have:

\[E\left[s_{m}\mid v\right]=\begin{cases} \frac{v-1.5}{2} & 1.5\leqslant v\leqslant2\\ \frac{3v-5.5}{2} & 2\leqslant v\leqslant2.5 \end{cases}\]

The expected price paid by the customer as a function of the true value is:

\[E\left[b_{i}\left(s_{m}\right)\mid v\right]=\begin{cases} \frac{2v+13}{8} & 1.5\leqslant v\leqslant2\\ \frac{6v+5}{8} & 2\leqslant v\leqslant2.5 \end{cases}\]

The expected excess paid by the customer over the true value is:

\[E\left[b_{i}\left(s_{m}\right)\mid v\right]-v=\begin{cases} \frac{13-6v}{8} & 1.5\leqslant v\leqslant2\\ \frac{5-2v}{8} & 2\leqslant v\leqslant2.5 \end{cases}\]

These are piecewise-linear functions, shown in Figure 2. Note that the unconditional distribution of is triangular across its whole range with a mode at 2, and it follows straightforwardly that the unconditional expected excess paid in equilibrium by a randomly selected customer is which of course is equal to the total expected excess profit earned by the insurers.

It’s important to remember that the range of possible customers I have considered shares the same class and experience modification. What I have shown, in effect, is that if the remaining differences between these clients are subject to differences of opinion among underwriters, then in equilibrium, insurers will be cautious in giving credit for a good opinion. Customers who appear to be the lowest risk also carry the greatest risk from possible underwriting error, so they will suffer the greatest increase in rate above their true value. As a result, they will also generate most of the insurers’ profit.

Note that although the actuarial indication is intended to represent a rate at which the insurer makes zero expected profit in excess of the included “normal” profit loading, this is not what will actually happen if the insurer simply issues quotes equal to the indication. Consider, for example, a symmetric outcome (this is not an equilibrium) in which each insurer issues quotes equal to the indicated values it produces, The lowest quote will win and will be from the insurer with the lowest signal. Using the function for the expected lowest signal from above, and substituting into the bid function, we have:

\[E\left[b_{A,i}\left(s_{m}\right)\mid v\right]=\begin{cases} \frac{1.5+v}{2} & 1.5\leqslant v\leqslant2\\ \frac{3v-2.5}{2} & 2\leqslant v\leqslant2.5 \end{cases}\]

This function is almost everywhere lower than so it is immediately apparent that the insurers will make an expected loss. It is easy to show that the unconditional expected value is in fact This is less than the value of or 8.3% of itself. Each insurer would win the auction with probability 0.5 and thus would make an expected loss of

Note that all my key results rest on there being more than one insurer. If there were only one insurer, then it might choose to exploit its monopoly power by setting even higher rates, but if it chose not to do that, then it could safely issue quotes at the actuarial indication, for all customers, without fear of making an expected loss overall. This might describe, for example, the strategy of a monopoly state fund. Intuitively, competing insurers know that they are more likely to win when their mistakes are to the customer’s advantage, so they need to bias their bids upward to compensate. A monopolist always wins the auction, so its negative and positive estimation errors can balance. This contrast between competition and monopoly does of course depend on the signals obtained by competing insurers’ being at least somewhat independent. To see this, assume that the insurers’ signals are not independent and are in fact perfectly correlated. Assume also that this fact is common knowledge among all market participants. This is an extreme and rather unrealistic assumption, but it serves as a useful demonstration. Each insurer believes that the true expected value is 1.50 plus its own signal. As in the example with independent signals, each insurer sees only its own signal before issuing a quote. The difference is that now it knows that the other insurer’s signal equals its own. The strategy choice of each insurer is a bid function that gives the amount of its quote as a function of its signal. I will again look for a symmetric Bayesian Nash equilibrium of the auction game. Since the two bids in a symmetric equilibrium will be equal. Assume that in such a case each insurer wins with probability The expected payoff of each insurer in equilibrium is thus the following:

\[\pi_{i}=\frac{1}{2}\left(b_{i}-E\left[v\mid s_{i}\right]\right)=\frac{1}{2}\left(b_{i}-1.5-s_{i}\right)\]

The expected payoff in equilibrium cannot be more than zero; otherwise either of the insurers could raise its payoff by reducing its bid by some small amount and winning the auction for sure. Setting the expected payoff to zero yields:

\[b_{i}=1.5+s_{i}\]

which can be rearranged to:

\[b_{i}=2.5-1\left(1-s_{i}\right)\]

So again, I can express a symmetric equilibrium strategy in the form except that now, with perfectly correlated signals, I find and expected insurer profit, individually and collectively, is zero. The extra information that the insurers have about each other results in the elimination of their profit. Or looking at this another way, I might say that the insurers’ lack of private information results in their profits being eliminated. The end result is also one in which the correct bidding strategy is to use the actuarial indication directly as the quote amount.

4. Discussion

The most important general inference I can draw from this work is that if underwriters for competing insurers make private mistakes (at least until later, after the business has been written), then a profit-maximizing insurer should generally compensate for the risk of such mistakes by quoting higher than the standard actuarial indication. Otherwise they will make underwriting losses. In my basic example, which is a fairly realistic depiction of a workers compensation policy sale, the expected underwriting loss ratio from quoting unmodified standard indications could be as high as 8.3%. The appropriate form of a compensatory rate increase is not to add (as actuaries and underwriters have been known to do) an unexplained “margin for conservatism” to the indicated quote. How much margin is appropriate? How much is too much? How should it vary with the individual risk characteristics? We have already seen that it may so vary. Does it also depend on the number of competing insurers, or the maximum extent of individual risk rating, or the extent of risk sharing by the client, or the relative skill of underwriters for different insurers? To what extent do similar considerations apply in markets where individual risk rating is not discretionary but the underlying rating plans are to some extent discretionary? These are important questions that should be asked if actuaries are to implement their stated precepts of pricing correctly, and which I think can be answered only by furthering the auction theoretic analysis of the rating process.

Some of the history of actuarial profit provisions can be found in Robbin (1992). Statements of the standard view can be found, for example, in the “Statement of Principles Regarding Property and Casualty Insurance Ratemaking” (Casualty Actuarial Society 1988)—“The underwriting profit and contingency provisions are the amounts that, when considered with net investment and other income, provide an appropriate total after-tax return”—and in the opening paragraph of (Werner and Modlin 2016)—“the price [of insurance] should reflect the costs associated with the product as well as incorporate an acceptable margin for profit.”

For a standard exposition of economic concepts of profit, see Varian (2010).

The use of profit maximization is somewhat muddied by the precept of rate regulation that a rate should be reasonable and not excessive, inadequate, or unfairly discriminatory. If companies aim to maximize profits then could the resulting profit loads be excessive or unfairly discriminatory? I would venture that the answer to both questions is generally no. I will show in this article that profit maximization may lead to profit provisions that are discriminatory, but not, I believe, unfairly so. In fact, I would conjecture that one of the benefits of the methods outlined in this article could be to give us a more enlightened view as to what constitutes a discriminatory rate. However, these conjectures should be examined further, beyond the scope of the current article.

Robinson (1933) developed a model of “monopsony,” or a market with many sellers and a single buyer, but this too is of little use in insurance because it assumes that the production costs of the good desired by the buyer are known, whereas another key characteristic of insurance products is that not only are these costs generally unknown but (more important) different sellers are likely to have different opinions about their expected value.

Klemperer (2004), Krishna (2010), or Milgrom (2001) can serve as a good introduction to auction theory.

See, for example, McClenahan (2001) for an introduction to this method of ratemaking.

In the literature of economics and management science, almost all study of strategy is couched in terms of game theory. Fudenberg and Tirole (1995), Gibbons (1992), Myerson (1991), Osborne (2004), and Osborne and Rubinstein (1994) are all good, broad introductions to game theory that commonly serve as standard texts for undergraduate- and graduate-level courses. Only one paper in the current FCAS syllabus, Mango (1998), mentions game theory at all.

Nature makes only one move, which must follow its specified random path, so we don’t need to think about its payoff. It is usual not to include Nature in the count of players.

Cooperative games were central in the early development of game theory, but the vast majority of work since the 1950s has been on noncooperative games. To illustrate, less than 10% of the pages in Fudenberg and Tirole (1995), Gibbons (1992), Myerson (1991), Osborne (2004), and Osborne and Rubinstein (1994) cover cooperative game theory. Cooperative game theory can be an interesting tool, but almost all development and applications of game theory today use noncooperative game theory. Mango (1998) touches briefly on cooperative game theory but does not refer to noncooperative game theory at all. It’s an excellent contribution to the study of risk loads but is not useful as an introduction to game theory.

A statement is common knowledge only if each participant knows it to be true, and each participant knows that each other participant knows it to be true, and each participant knows that each other participant knows that each person knows it to be true, and so forth. This rather demanding sounding condition can be summed up, closely enough in the current context, as saying that the statement is obviously true.

A procurement auction is one.

Investment bankers sometimes refer to this as a Dutch auction.

Rather like for the Central Limit Theorem, no one canonical statement is uniquely identified in the literature of auction theory as the Revenue Equivalence Theorem; rather it comprises a collection of closely related results.

The straightforwardness of a first-price sealed bid auction is sometimes challenged by the customer or by a broker or agent acting for the customer, extending the auction by giving some bidders a chance to improve their bids, or leaking information about bids to other bidders, or changing other terms of the auction on the fly. We can obviously complicate the game descriptions to include such moves and analyze equilibria of the revised games. The Revenue Equivalence Theorem describes a surprisingly large extent to which such variations in the form of the auction game may not affect key outcomes of an auction, including the expected price paid or received by each player. A useful next step in analysis would be to consider more complex move sequences by introducing the Revenue Equivalence Theorem and considering how far its application extends across the possible variations of insurance auctions.