1. Introduction

In this paper we will attempt to present an overview of service contracts and the general structure of many service contract programs. As with any such overview, it is necessarily limited to the current state of the industry, which is in a continual state of change. In addition there are numerous variations of many of these characteristics. Therefore, no overview can be complete, nor can it remain current for any extended period of time.

We begin with a description of service contracts, what they cover, and their general common characteristics. Our focus will be on characteristics of the contracts and service contract programs that affect overall costs and the timing of cash flows. Understanding these cash flows is critical to assessing the profitability of a service contract program overall and to assessing areas of relative strengths and weaknesses in that program.

Although we will attempt to be general in our discussion, we will touch on the major types of products often covered by service contracts. We will also touch on the more significant unique characteristics among various product groups, again with the objective of identifying characteristics that affect the estimation of liabilities, whether they be for unpaid claims or for unearned premiums or fees.

2. Contract and program structure

We begin our overview with a brief discussion of what service contracts cover. We then move to a discussion of the structural elements common in many service contract programs.

2.1. What service contracts cover

Generally, service contracts are agreements by one party, known as the obligor, with the owner of an item to either repair or replace or, in some instances, to reimburse the owner for the cost to repair or replace that item or specific components of that item should the item or components break or fail to function. As with any contract, the terms are usually specific and the details often differ from one service contract program to another.

2.2. Types of items covered

At one time, service contracts were limited to certain products such as major appliances, homes, and motor vehicles. Now service contracts are offered on a wide array of products. Many stores find the sale of service contracts a major profit source, particularly where sales margins have been squeezed by competition, and offer contracts on virtually all products sold. This is particularly true of electronics stores.

Major categories of products currently covered by service contracts include the following:

Motor Vehicles

-

Automobiles

-

Trucks

-

Motorcycles

-

Recreational Vehicles

-

All-Terrain Vehicles

Watercraft

Travel Trailers

New Homes

Home Systems

Major Appliances

Electronics

-

Televisions

-

Sound Systems

-

Video Cameras

-

Film and Digital Cameras

-

General Consumer Electronics

Computers and Peripherals

Other

2.3. Common contract provisions

There are a wide variety of contracts and contract provisions. Though we will try to describe provisions that often appear in service contracts, we caution that it is not likely that any specific contract will have all the characteristics we will describe. In this section, we are focusing on the contracts sold to the ultimate consumer and not variations in the structure of service contract programs. We will undertake such a discussion in a later section.

Many products come with some form of warranty, by either the manufacturer (original equipment manufacturer or OEM) or the product seller, or both. Service contracts are usually secondary to the OEM warranty and do not cover repairs or other benefits covered by the OEM warranty and other factory-provided repairs.

Almost all service contracts are limited by time. Contracts on used cars or cell phones may be as short as one month or less, while new home warranties typically have 10-year terms. Common contract terms for coverages on used cars are one to three years, while terms for new cars usually run from five to seven years from the original vehicle in-service date. Coverage for electronics is often for three or so years. Some contracts—for example, for home systems—are annual, as are some mechanical breakdown insurance products offered by some personal lines insurers in conjunction with traditional automobile coverage for physical damage. Most service contracts on motor vehicles also have mileage limitations, with the contract expiring at the earlier of when the contract time limit or the mileage limit is reached.

The agreement usually provides for repair of an item or component that fails. Sometimes it is less expensive to replace a failed item or component than repair it. Thus, most contracts include an option to replace the malfunctioning item or component. In addition, liability under the contract is usually limited to the value of the item covered at the time of the loss.

Nearly all contracts have some sort of deductible, though some programs offer the opportunity to purchase a $0 deductible at an increased cost.

Similar to customary insurance policies, there are usually exclusions for intentional acts and damage caused by external events that are often covered under traditional insurance policies. Acts of God, war, and other common policy exclusions are also found in many, if not most, service contracts.

We now look at some major categories of service contracts that have evolved their own characteristics.

2.3.1. Motor vehicles

One of the largest segments of the service contract industry relates to coverage for motor vehicles. In this section we will look at some features of these coverages that help set them apart from other service contracts.

New vs. used. Traditionally, service contracts on motor vehicles were divided between contracts designed to be sold on used cars and those designed to be sold on new cars. Since the service contract is in excess of OEM warranties, and car manufacturers generally agree to repair problems that occur early in the life of a vehicle, motor vehicle contracts designed for new cars traditionally were written to expire at the earlier of the time or mileage limitations as measured from when the vehicle was first put into service, that is, when the title to the vehicle is first issued. In contrast, service contracts on used vehicles generally have been written to run for the time or mileage from the time the contract is written.

Although a car is either new (not yet sold to the first purchaser) or used (already sold), not all used cars are the same. With OEM warranties now usually running 36 months or 36,000 miles, whichever comes first, or even longer, it is not uncommon to have used cars for sale that are still under the OEM warranty.

The argument had been advanced that since such cars are still under OEM warranty, they should be eligible for service contracts that were designed to be sold on new vehicles. Thus, in the early to mid-1990s, it became common for service contract sellers to sell contracts designed for new cars on these “near new” vehicles. Though there are many terms for such a provision, we will use the term “extended eligibility” to refer to the sale of a contract originally designed to be sold on new vehicles on vehicles that are actually used.

As with contracts written on truly new vehicles, the corresponding service contracts were still designed to run from the original vehicle in-service date. Thus the purchase of an 84 months/100,000 miles contract on a two-year-old car with 24,000 miles would afford the customer an additional 60 months or 76,000 miles of coverage from the date of purchase, whichever comes first.

Notice here that we have a dichotomy of contracts as summarized by Table 1.

More recently there has been a movement in the vehicle service contract market away from this traditional dichotomy to include other variations for “near new” cars that are usually still under OEM warranty. Many service contract programs now have what we call a “hybrid” type of new car contract (not to be confused with gasoline/electric vehicles). In these programs, the hybrid contract has replaced the traditional new car contract. For this hybrid contract, the contract expires on the time limit when measured from the contract sale date or the mileage limit when measured from the in-service date, whichever comes first.

Other programs have done away with the new/used dichotomy in contracts, offering only contracts that have terms that correspond to traditional used car contracts, whether on vehicles that are still under OEM warranty or not.

Since these contract characteristics affect the emergence of losses under the various contracts, it is critical that they be considered any time that liabilities under such contracts are to be estimated.

Covered parts. Although there is considerable variation from one service contract program to another, generally there are two main types of contracts available—either a “named part” type or an “all part” type that correspond to “named peril” and “all risk” coverages, respectively, under traditional insurance. The named part coverage provides for the repair or replacement of a specified list of parts, while the all part covers all mechanical parts with a list of excluded parts or assemblies. Many programs have different levels of coverage for named parts, ranging from the most restrictive, which commonly limits coverage to the power train, to levels providing coverage for a longer list of parts.

Exclusions. As with traditional insurance coverages, service contracts on motor vehicles typically have a number of exclusions. Such exclusions include the use of the vehicle for racing or competition, commercial use, acts of God, acts of war or the government, failure to follow scheduled maintenance, and intentional damage. Service contracts typically also exclude causes of loss usually found in traditional insurance coverages such as theft, collision, vandalism, flood, and the like.

As mentioned above, service contracts are secondary to the OEM warranty. In addition, service contracts also typically exclude repairs covered by manufacturer recalls or by service notices. These service notices, sometimes called “secret warranties,” are arrangements made by the manufacturer to effect specific repairs, often to correct an inherent flaw in a specific vehicle model.

Nearly all service contracts exclude coverage for consumable components such as tires, batteries, brake shoes or pads, windshield wiper blades, and fluids. Often excluded are also “fit and finish” items such as paint, window glass, and body panels. In addition, some contracts also exclude coverage for failure caused by normal “wear and tear,” while others specifically include such coverage.

Since service contracts are focused on the repair of a mechanical breakdown, they usually exclude scheduled maintenance, though some programs have contracts that do provide such a benefit.

Additional coverages. Although coverage is secondary to the OEM warranty, it is possible for a service contract to incur losses even when the OEM warranty is in effect. This arises from the fact that some service contracts provide benefits that are not provided under the OEM warranty. Such additional provisions may include reimbursement for certain non-repair costs arising out of a breakdown, such as rental of a replacement vehicle, towing, and trip interruption.

Transferable. Some service contracts are transferable to subsequent purchasers of the covered product. Again, this feature is present in many motor vehicle service contracts. In the case of transfer, the contract holder usually must pay a nominal fee, often in the neighborhood of $25, and inform the issuer of the contract or the issuer’s designee or other involved party of the transfer. Transfers are generally not allowed when the vehicle is sold to an auto dealer.

Cancelable. Contracts usually cannot be canceled by the issuer of the contract. Since vehicle service contracts are often financed with the vehicle, there generally are limited cancellation provisions allowing the contract holder to cancel during the term of the contract with return of fees paid, usually on a pro rata basis. For motor vehicles, fees are generally returned on a pro rata basis as the lesser of the percentage of time remaining and the percentage of mileage remaining on the contract. We understand that most lenders require a pro rata refund of premium in order to allow the service contract to be included in the vehicle financing.

2.3.2. New homes

Regulations by the United States Department of Housing and Urban Development (HUD) require that new home builders offer certain limited warranties in order to qualify for HUD financing. Currently the minimum such warranty must include one year of coverage on workmanship, two years on major systems, and 10 years on the structure. Builders usually do not want the obligation for a project lasting for 10 years so they often satisfy this obligation by purchasing a policy or contract to provide the benefits. We note that technically this is an example of a warranty offered by the “manufacturer” (the home builder) and included in the price of a house as opposed to an “extended service contract” that is usually a separate purchase by a consumer. However, there are firms that market services to builders relating to new home warranties, so related programs do have many characteristics in common with other extended service contract programs.

2.3.3. Appliances and home systems

Technically, service contracts on most appliance and home systems are renewable annually. Appliance contracts cover a single major appliance—for example, a refrigerator, washer, or dryer. Home systems contracts, often offered as an inducement by the seller of an existing home, cover major systems in the home, including heating, ventilation, air conditioning, plumbing, drains, and the like. The new owners are then usually offered the opportunity to renew the service contract on its expiration. Many of these programs also offer options that cover major appliances such as refrigerators, washers, and dryers, even though such appliances are not part of the home systems.

2.3.4. Cellular phones

Service contracts on cellular phones are often provided on a month-to-month basis with the contract cost collected by the cellular provider. In contrast to many other service contracts, coverage for loss or theft of the phone is often included in such plans.

2.4. The transaction

A service contract is generally an agreement wherein one party, denoted the obligor, takes on the obligation to repair or replace a specific item if that item fails to operate under specific provisions of the contract. Thus, there are at least two parties to the contract, as in most contracts. However, service contract programs may have more entities involved.

For example, a service contract administrator markets and administers a service contract program. The administrator may also be the obligor, or there may be a separate entity taking on the responsibility of the obligor. These entities may also be separate from the product seller actually selling the contract. In turn, the obligor may purchase an insurance policy, technically a service contract reimbursement policy, from an insurer.

The number of parties taking part in the transaction requires care in identifying the insurance premium involved. Not only is this important for aggregate income determination for an insurer, but it is also important in the timing of future payments of losses and expenses under the insurance contract.

The number of parties in the transaction also affects the total cost and the amounts going to each of the involved parties. For example, the contract holder usually pays the product seller for the contract. As noted above, this transaction usually is not regulated as insurance; thus, the product seller is free to set the contract price and the contract holder is free to negotiate that price, though few know of this option.

The seller then remits an amount to the contract administrator, often including an administrative fee for the policy administration and potential claims handling services of the administrator. The administrator in turn remits an amount to the obligor in exchange for the obligor assuming the obligation to fulfill the service contract. Finally, the obligor may purchase an insurance policy covering all or part of the obligor’s obligation assumed under the contract. This final piece is subject to insurance regulation, premium taxes, and liability provisions on the insurer’s books.

There is at least one exception to this broad description. We understand that for motor vehicles, Florida allows only mechanical breakdown insurance wherein the transaction is an insurance policy between the purchaser of the vehicle and an insurer. This is only one of many variations among the states as to allowable structures and insurance protections for service contract programs. Later in this paper we will provide a brief summary of some of these issues. A more complete discussion of those differences is beyond the scope of this overview.

2.4.1. The seller

As mentioned earlier, the price charged to the final customer by the contract seller is usually not regulated. The seller knows the seller’s costs and is usually free to set the contract price. The seller remits the required contract costs to the administrator or obligor and keeps the remainder as income.

2.4.2. Loss-sensitive features

It is not unusual for service contract programs to have features that respond to the loss experience of a program. In motor vehicle programs, it is not uncommon for the selling dealer to share in the “profits” of his or her business. These profit-sharing arrangements are often one-way with no participation in losses.

Larger sellers of service contracts may also set up their own captive insurer or reinsurer that accepts a substantial portion, or all, of the underwriting risk from the obligor or insurer in a service contract program. These vehicles are sometimes referred to as producer-owned reinsurance companies or PORCs. To the extent that a PORC assumes risk from an obligor who is not an insurer, that PORC would technically be an insurer and not a reinsurer. A variation for some might be a “rent-a-captive” arrangement with existing insurers set up under the particular program. It is also possible that the seller could receive trust funds remaining once all claims have been paid.

Very often the level of loss-sensitive compensation to a contract seller is determined using a loss ratio that is calculated as losses paid divided by earned “reserves.” Here “reserves” refers to the portion of contract fees intended to pay for service contract losses and potentially related loss adjustment expenses. This is common terminology in service contract programs, though quite confusing to professionals with an insurance background. Payment timing is not usually a significant issue since claims are usually paid quite soon after the loss (a breakdown) occurs; however, the timing of income recognition is a much less certain exercise.

2.4.3. The obligor

As noted above, the obligor plays a pivotal role in a service contract program. The obligor takes on the responsibility to fulfill the service contract. One of many of the parties in the above-described transaction can be the obligor: the product seller, the administrator, a separate obligor company, the product manufacturer, or even the insurer. State laws sometimes dictate which, with some allowing the seller to be the obligor, others requiring a separate entity.

The obligor may retain some or all of the risks of fulfilling the service contract obligations. In some programs, all the risk assumed by the obligor is transferred to an insurer via a service contract reimbursement policy. If there is a single obligor for a large, multistate or nationwide program, then there may only be a single insurance policy involved.

2.4.4. The administrator

Very often a service contract program is packaged by an administrator. For a fee, usually per service contract, the administrator will take “cradle to grave” responsibility for the program, usually without taking associated underwriting risk. The administrator usually handles the marketing materials, the placement of the program with various sellers, contract design and contract forms, contract administration, rating plan design and pricing, and claims handling and administration. The administrator may also act as the obligor in a program or some other entity may take on that role.

2.4.5. Trusts

Some programs leave a significant portion of the risk with the obligor in the form of what is often called a trust account. In such an arrangement, the obligor deposits a specific portion of the service contract fee, usually referred to as the “reserve,” into an account. The obligor then pays losses and certain defined expenses (usually related to loss adjustment) from this account and interest accrues to the account. The obligor might then purchase a surety bond, or guarantee coverage from an insurer in the event the trust account becomes exhausted. Often the premiums for such stop-loss coverage are nominal, in the range of $25 or so per contract issued.

It is important enough to repeat: The term “reserve” in a service contract program refers to the loss (including potential loss adjustment and other specified expense) portion of the cost of a service contract. This unfortunate use of a term often used in insurance can lead the unwary to significant misunderstandings.

Often the obligor will purchase an insurance policy that assumes the liability of the obligor should the trust become exhausted. As with any insurance policy, the specific terms of the contract are important in understanding its liabilities and cash flows. A trust guarantee policy could be written to insure the trust for service contracts written during a year and be unaffected by profits or losses on service contracts written in other years. A trust guarantee policy could also be written to pay all remaining losses should the trust on an inception-to-date basis become exhausted in a year. Still another variation could have the guarantee policy effective until the last contract in a trust expires.

The premium for a guarantee policy is based on the number of service contracts written in the program. As mentioned earlier, the charges tend to be nominal, often in the neighborhood of $25 per contract.

2.4.6. Some examples of program structure

Schematically the following four sections briefly describe various program structures we have discussed here. The amounts shown are purely hypothetical and are selected so that the same amounts end up flowing to fund losses and to pay expenses, though relative magnitudes would not be too unusual in various vehicle service contract programs.

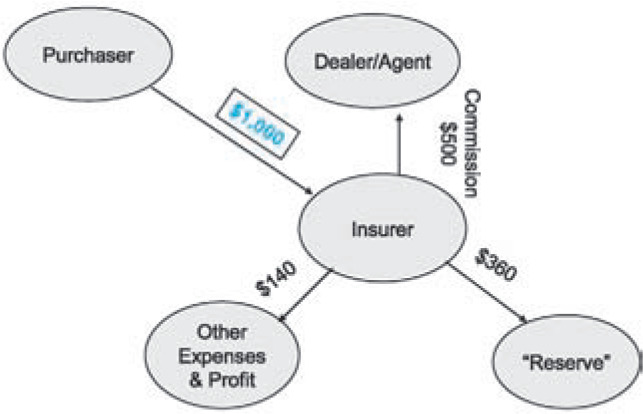

Direct insurance. Probably the simplest of programs is the direct insurance program, which is the only structure allowable in Florida for motor vehicles. In this case the dealer or other seller acts as an agent, selling the mechanical breakdown insurance policy directly to the car purchaser. In our simplified example, the insurance premium (in a box and in blue type) is arbitrarily set at $1,000, with total commissions of $500, total expenses of $140, and pure premium (often called “reserves” in the service contract arena) of $360. Figure 1 summarizes this transaction.

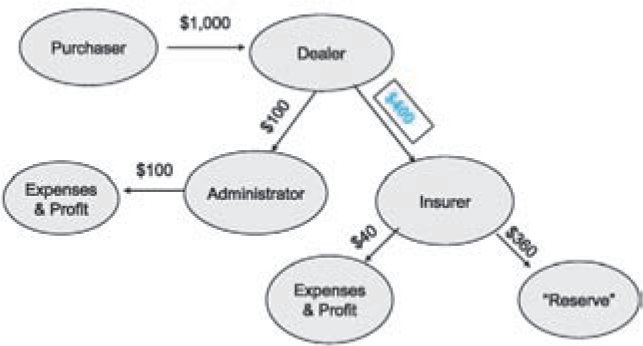

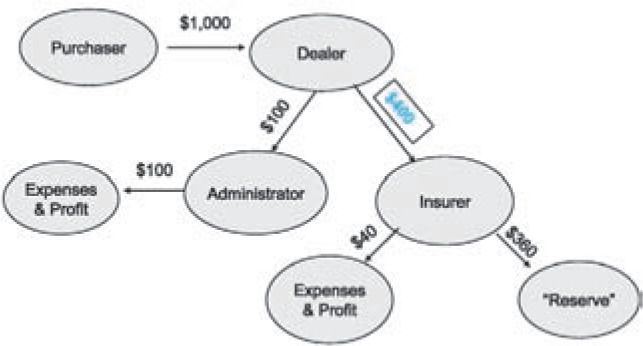

Dealer obligor. Many states allow the dealer to be the obligor on a contract. Thus, the service contract is a contract between the purchaser and the dealer, which is usually not regulated. In the meantime, the dealer usually purchases a service contract reimbursement policy, to cover obligations assumed under the service contract. An administrator is often involved in this sort of program and charges the dealer a separate fee for its services. As with the other programs described in this section, the dealer is usually free to set the price charged to the consumer; thus, in many programs the amount the dealer retains can vary from transaction to transaction. This type of program design is shown in Figure 2.

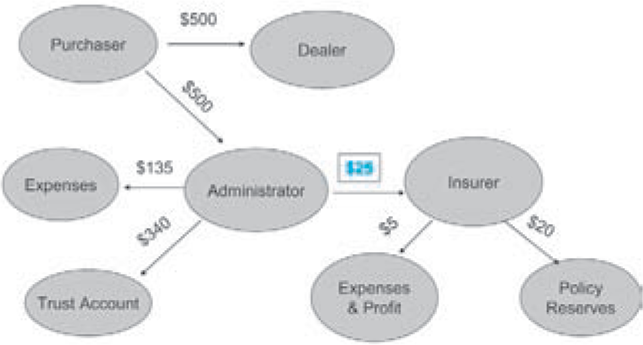

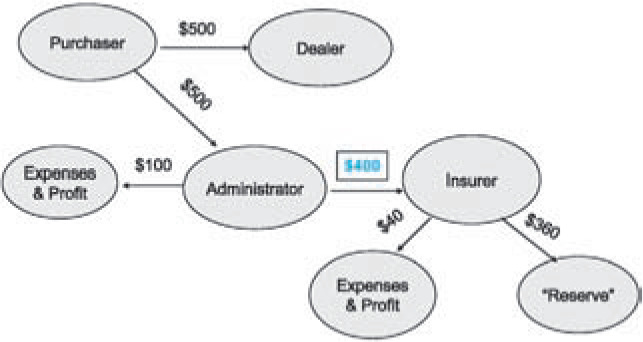

Administrator obligor. Very similar to the dealer obligor program, this variation has the administrator assuming the obligation to provide service (though a separate administrator and obligor could be created). Here, the obligor and not the dealer or purchaser pays the insurance premium. Most states allow this variation, with some having minimum requirements for the insurer (such as a minimum rating from A.M. Best). Figure 3 shows two separate payments by the customer, one to the dealer and one to the obligor. As with the trust program described in the next section, in reality there is usually only one check issued to the dealer, from which the dealer remits an amount to the obligor and retains the rest. We are showing two amounts in Figures 3 and 4 to emphasize that the dealer compensation in the form of the difference between the dealer’s charge and actual contract cost is outside of the obligor system.

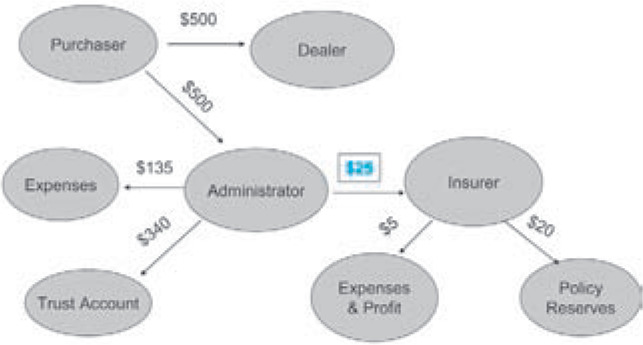

Trust program. The trust program leaves much of the funds to provide for repairs with the obligor, with only a small amount of premium actually paid to an insurer. It would appear that the presence of an insurer, at least technically, may satisfy requirements for the fund to be insured. Figure 4 gives a view of this type of program. Again, as with the obligor model, there is usually only one check written by the actual contract purchaser.

Here, the actual insurance premium is quite small ($25) relative to the cash flows in the program. Though an example, the magnitude of $25 per contract is not unusual in the trust contracts we have seen. We also note here that “Policy Reserves” refers to loss and loss adjustment expense reserves as well as unearned premium reserves carried by the insurer.

Even if the insurer has the appropriate financial strength rating, the nature of the trust guarantee policy might result in little or no actual protection to the trust. As mentioned above, it is not uncommon for trust guarantee policies to be written on an annual claims-made basis, with no claim occurring during a year unless the trust is actually exhausted during the year.

As with a Ponzi scheme, as long as the business is growing rapidly, the chance of a cash flow shortfall in any year is often quite small, even if the underlying contracts are severely underpriced. Theoretically, at least, the insurer in this case has no losses; thus, profits are nearly equal to total premium for each year that the fund is not exhausted. There are no requirements for the insurer to retain these “profits” as surplus; therefore, the insurer could release them to its shareholders as long as the trust account is solvent.

Using realistic assumptions regarding loss emergence and payment, we can construct an example of a program growing at 10% per year and priced such that each $1 in revenue, including investment income, will generate $2 in losses that does not exhaust the trust until the seventh year! The appendix to this paper gives an example of how this can happen. This occurs even though the product is obviously seriously underpriced. In addition, like Ponzi schemes, the faster the growth in business, and the longer the lag from policy issue to claims occurrence, the longer the delay before an underpriced trust exhausts its resources.

It could also be argued that since the policy is a one-year claims-made contract, there is no obligation in subsequent years. Thus, there is no need to maintain surplus at anything near the levels of potential liabilities of the trust. If it appears that the trust is nearly running out, then the insurer could simply refuse to write the coverage the next year, effectively eliminating any “protection” offered by the requirement to have the obligation insured. Even if the guarantee was priced appropriately, if the insurer distributes profits, then it would not have sufficient assets to cover obligor liabilities even if it wrote coverage in the fateful year the trust is exhausted. Of course, business relationships between the obligor and insurer may hinder the insurer’s ability to stop offering the coverage.

This problem does not arise if a trust guarantee is written to cover the segregated trust for contracts written in a particular year. In this case, the trust policy is similar to any other multiple-year policy and closely tracks characteristics of the underlying service contracts. Here, the issues of loss reserves and premium reserves track those already dealt with in mechanical breakdown insurance and other multiple-year contracts.

It is also possible that guarantee policies could last for the duration of the trust. Though we have not seen this variation in practice, such a policy would be open-ended and effectively could be seen to bar the release of “profits” by the insurer until the underlying trust is completely run off.

2.5. Reserving considerations

Although there are a number of contracts with terms of one year or less—for example, on cellular phones, home systems, some used vehicles, and so forth—most service contracts are multi-year commitments funded by a single payment by the contract holder at the beginning of the contract. Because of this, service contracts have characteristics that are different from traditional property and casualty insurance products.

2.5.1. Total contract liabilities

For most property and casualty insurance products, one generally expects losses to arise uniformly, or nearly uniformly, over the life of a contract. Most property and casualty insurance products that have terms of less than one year, and even multiple-year policies such as three-year fire policies will generally expect uniform emergence of claims over the life of a contract.

On the other hand, claim liabilities (loss and loss adjustment expense reserves) for traditional insurance products are often difficult to estimate because final settlement of claims that have occurred may take many years to achieve. Conversely, due to predictable loss emergence, the mechanism to control recognition of income (the unearned premium reserve) is usually quite easy to specify.

Multiple-year service contracts turn this paradigm on its head. As we will discuss in greater detail later in this paper, liabilities for existing breakdowns tend to be relatively small and can often be forecast with relatively high precision. On the other hand, the expected emergence of losses and expenses during the life of a service contract, or related reimbursement policy, can be quite complex and subject to not only contract provisions but also the associated product manufacturers.

Based on these characteristics of service contracts, we prefer to consider contract liabilities holistically, without the distinction between loss and loss adjustment expense liabilities and unearned fee reserves. Although the tail can be quite long, if care is exercised, customary actuarial forecasting methods applied to suitably constructed data triangles, often by contract quarter, can lead to reasonably accurate estimates of expected future losses on contracts in force on a valuation date.

However, the annual orientation of accounting practices seems to require annual assessment of the profitability of an insurer’s book. Thus, there is a reporting need to separate loss and loss adjustment expense reserves and unearned premium reserves for service contract-related policies, such as reimbursement insurance policies.

2.5.2. Loss and loss adjustment expense reserves

Typically, service contracts involve an agreement to repair or replace a covered part in the event of breakdown. Thus, no obligation generally exists on the part of the obligor until a breakdown occurs. Once a breakdown occurs, a claim exists and liability for the costs related to that claim should probably be recognized by the obligor and by the entity insuring the obligor. Typically, service contract claims are very well defined. Repairs are made relatively quickly and costs, in general, are completely determined within a relatively short amount of time, usually days or a few weeks after the breakdown for most claims. In fact, it is not unusual to see more than 75% of the dollars for breakdowns occurring in a quarter being paid by the end of that quarter, and well over 90% by three months after that. In addition, since coverage is for mechanical breakdown, there is usually not much salvage or subrogation involved. All these factors make loss and loss adjustment reserves a relatively small part of liabilities for obligors or insurers of typical service contract programs.

Service contract claims tend to have relatively low severity and could have relatively high frequency. For example, the average cost for automobile service contract claims could be in the range of $300 to $500, with frequencies on some longer-term contracts on new cars of two or more claims per contract. For this reason, along with the relatively short payment tail, ultimate losses on existing claims are usually subject to rather accurate estimation.

One way to analyze the need for loss and loss adjustment expense reserves for a non-trust service contract program, in contrast to a trust program, is to review historical triangles of payments and claim counts sorted by breakdown month, or quarter, and valuation month, or quarter, using standard actuarial forecasting methods. It is not uncommon for insurers not to set separate case reserves on warranty claims. This is due to the relatively small average claim size, large number of claims, and the relatively short time a claim remains open. Thus, case reserves are often zero and analysis is usually confined to claim count and paid loss data.

In this discussion, we have assumed that the insurance policy and the obligation of the obligor are triggered by a covered breakdown. The situation for trusts is likely to be different. Depending on contract wording, it is likely that in policies guaranteeing trusts, the insured event is the trust exhausting its funds. Consequently, unless the trust is likely to exhaust its funds due to claims occurring at the valuation date or before, there is no need for the insurer who guarantees the trust to post loss and loss adjustment expense reserves.

If one argues that the claim occurs once payments exceed fund balance, then one can argue that there is only one claim whose size will be determined once all policies to be covered by the trust expire. Under this interpretation, once a claim has occurred, the loss reserve would be the entire obligation of the trust until all underlying contracts expire, with an unearned premium reserve no longer appropriate or required for that policy.

2.5.3. Unearned premium or fee reserves

With multiple year contracts and financial reporting done much more frequently, the rate at which premium is recognized as income can be critical in monitoring the profitability of a book of service contract business. For this reason unearned premium or fee reserves is a critical component of the financial statement for a company involved in service contract business.

Service contract reimbursement insurance. We first consider the service contract reimbursement insurance policies that directly compensate the obligor for the entire obligation assumed under a service contract. In the next section, we will discuss issues related to trust guarantee policies.

One way to view unearned premium reserve (UEPR), a term we will also use in talking about unearned fee reserve where an insurance policy is not involved, for service contract-related business is the difference between total future losses under existing policies or contracts (holistic forecast) less the future payments on existing claims—the loss and loss adjustment expense reserves. In short, under this view of the UEPR, it is to provide for the losses that are expected to arise on claims occurring after the valuation date on existing contracts. This approach, though an accurate reflection of expected future liabilities, would in effect allow a company to take all profits from its service contract business into income immediately, and not over the life of the various contracts. We note that even if an obligor ceases coverage with a particular insurer, the insurer may still be obliged to return premiums in the event of future cancellations by service contract holders, so it may not be prudent to recognize all apparent profits immediately.

A way to control release into income appears to exist in procedures that we understand apply to generally accepted accounting practices (GAAP) in the United States. In this case, the UEPR is set as the written contract fees or premiums for the contract multiplied by the ratio of expected future losses and expenses divided by expected total losses and expenses for that contract.[1] In practice, it is usually acceptable to do this on an aggregate basis, such as by policy month, but this is often determined prior to the writing of that policy. This amount then becomes the “base line” or minimum unearned premium or fee during the life of the policy. It may be that the holistic approach, in combination with a broad-based (multiple line) test of premium deficiency, may give rise to the need for additional reserves to be posted. Given that premium deficiency calculations may be on a level less fine than either an account or line of business level, and given that discounting may be allowed even to the date of payment, it is unclear how much influence the holistic approach will have on total premium deficiency.

Statutory accounting practices in the United States for long-duration contracts differ from this approach and incorporate a three-way test for the minimum allowable UEPR, which incorporates the two GAAP provisions described above, but allows discounting only to the date of loss occurrence in what would correspond to the GAAP premium deficiency reserve calculation. Statutory accounting in the United States adds a third test, not allowing the UEPR to be less than the amount the insurer would have to refund if all policies were canceled. As indicated previously, this provision is usually pro rata based on time and mileage for vehicle service contracts.

These issues are further complicated by the fact that losses and expenses on service contracts generally do not arise uniformly over the life of a service contract. The expected loss emergence patterns usually vary by product covered (televisions vs. automobiles) and even by particular characteristics of the product (new vs. used for vehicles).

Often, as products age, the chances for failure increase. Thus, one might expect service contract losses to be “back-ended,” that is, more heavily weighted toward the end of a contract than toward the beginning. This general tendency might be offset, however, by other factors such as the contract holder forgetting the contract exists after a period of time or even discarding the covered item before the contract expires.

In the case of vehicles, by and large, losses for service contracts on used vehicles tend to be “front-loaded,” that is, losses tend to occur more toward the beginning of the contract than toward the end. A factor contributing to this is the mileage limitation included in vehicle service contracts, causing the contracts to expire because of mileage before the time expires.

Conversely, service contracts sold on truly new cars (at the time they are first put into service) tend to be rather heavily back-ended. This is largely due to the presence of the OEM warranty, now usually in effect for the first 36 months or 36,000 miles of the vehicle’s life. As pointed out previously, this eliminates most, but not all, service contract losses in the early stages of a new car contract.

Matters become less clear for contracts sold on cars that are still under OEM warranty but removed from the original in-service date, extended eligibility contracts. Here, the bias in loss emergence is not as clear-cut as for used and truly new vehicles. Emergence of losses will depend on how close the service contract effective date is to the expiration of the OEM warranty. The closer the two dates are together, the more we could expect the contract to behave like a used car contract.

This discussion only hints at some of the complexity involved in completely estimating the UEPR for service contracts. Companies writing service contracts need a way to continuously monitor experience without constantly reevaluating the ultimate losses for a wide array of different contracts. To accomplish this, they often use “earning curves” to approximate the expected emergence of losses for a contract.

Practically, such a company will calculate the “earned premium” or more often “earned reserves” (again “reserves” in the service contract context) for each contract at a valuation date based on the policy age and a table of percentages that may vary by contract type (such as new, used, and hybrid), contract term (time and mileage limitations), and possibly certain contract features (such as all-parts, named parts, power train). The level of analysis and discrimination that goes into this table varies from company to company. Some companies will analyze their experience under various major contract groups at various time (and for vehicles, mileage) limitations and select their earning curves to match that experience. Other companies may take a rougher approach and use much broader estimates, such as pro rata for used car contracts and the “reverse rule of 78s” for new car contracts. The reverse rule of 78s earns one unit the first month, two units the second month, and so forth, through the life of the contract. The 78 comes from the sum of 1 + 2 + . . . + 12 (for a 12-month policy) and is called “reverse” since the original “rule of 78s” was developed to calculate interest accrual on simple interest loans where a large part of the interest (12/78) is included in the first month’s payment, 11/78 in the second month’s, and so forth.

A side effect of statutory accounting in the United States for long-duration contracts is that under certain conditions, pro rata earning for used car contracts and the reverse rule of 78s for new car contracts give UEPR calculations that exceed the statutory minimum requirements. This is not too difficult to see for used cars, as the following paragraph explains. Though not as obvious, it occurs for new cars, as we will discuss later.

Under the assumption that the service contract is adequately priced, then the statutory UEPR is the larger of the portion of losses and expenses expected in the future multiplied by written premium, or the amount to be refunded on cancellation. Since used car contracts have losses that are “front-ended,” the proportion of future losses and expenses is generally less than the proportion of time yet to elapse; therefore, it is less than the amount unearned on a pro rata basis. Similarly, since cancellations for vehicle contracts usually refund the lesser of the proportion remaining based on time and the proportion remaining based on mileage, the refund amount too is no larger than the pro rata amount to emerge. Hence, setting UEPR for used car contracts on a pro rata basis will be at least as large as the minimum under statutory accounting.

Although not as clear, it is also often the case that for an adequately priced new car contract with substantial commission expenses, the Statutory UEPR is smaller than the amount calculated by the reverse rule of 78s. Again the pricing assumption removes the third calculation in the statutory minimum formula from consideration, and again the statutory minimum is the larger of the cancellation provision and the proportion of losses and expenses yet to emerge. One would expect that because new car losses tend to be back-loaded, the proportion of loss and expense calculation would dominate. This expectation, however, ignores the “and expenses” provision. If there are noticeable up-front expenses (premium taxes, commissions, other acquisition expenses), then the proportion of expected future losses and expenses can start well below the pro rata level. So once more, there is a strong chance that the “refund on cancellation” calculation will again dominate, and that amount is clearly less than what is remaining under the reverse rule of 78s.

We note in the above discussions that the assumption of adequate pricing is actually stronger than necessary. Note that we used that assumption to limit consideration to only the first two of the three statutory calculations. Since the third statutory calculation allows for discounting, it is possible for a contract to be underpriced and yet still have the third calculation smaller than one of the other two.

This discussion is not meant to argue that a simple formula such as the reverse rule of 78s is appropriate, but rather it is intended as an example of some of the possibly unexpected consequences of the National Association of Insurance Commissioners (NAIC’s) minimum unearned premium formula.

Premium earning on vehicle service contracts can have some interesting consequences. Suppose, for sake of argument, a company’s earning pattern for new car contracts mirrors the emergence of losses under those contracts. All things being equal, we would expect the loss ratio—calculated as policy inception-to-date incurred losses divided by inception-to-date earned fees—to be reasonably stable over time. Cancellations, however, can have some unexpected consequences. As indicated previously, cancellation provisions on vehicle contracts are usually pro rata based on the lesser of the proportion of time or mileage remaining in the contract. Since few losses emerge during the early stages of a new car contract, if a company earns premium based on the pattern of loss emergence, then little premium or fee is earned in the early policy ages. Therefore, the amount refunded tends to be substantially less than the exposure remaining on the contract, even if the pricing is exactly correct. As such, cancellations tend to show profit in the early ages of a new car contract, even if the underlying pricing is not set to show that level of profit.

This same logic also shows that cancellations early in the life of a used car contract would generally result in unexpected losses if premium or fee earning is set to track loss emergence. This happens because losses in used car contracts tend to occur more in earlier ages than later and premium or contract fee is usually refunded on a pro rata basis.

Service contract trust guarantees. Policies that cover trusts have different characteristics and present some interesting questions. First, let us assume that, as the previous arguments would imply, a loss under a trust guarantee policy does not occur until there is a payment that exceeds the accumulated trust.

If a policy guarantees the fund established for contracts written during a period of time, such as a contract year, then the loss emergence “curve,” the percentage of losses that emerge under a contract as a function of time, stays zero until the fund is exhausted. If there is only one claim—the exhaustion of the fund, as argued previously—then all liabilities immediately transfer to loss reserves with no unearned premium reserve. This is an interesting situation with the “earning” pattern being zero until a claim occurs (or the policy expires) and then moving immediately to 100%.

This is one point of view. If an insurer issued trust policies on several different accounts or trusts, another argument is that a pattern of expected claim emergence for a portfolio of these contracts would be used to determine an earnings pattern. This pattern would probably be very back-ended, with no adjustment for those policies that are triggered. We note that the two approaches get the same answer if the portfolio of policies has loss experience as expected.

Another variation is a guarantee policy that covers payments that exceed the inception-to-date fund balance. The principal, though subtle, difference between this variation and the prior description is the open-ended nature of this variation. The prior description segregates funds by contract year. This variation combines funds from multiple policy periods. Since the trust is now considered as a single account, with new contracts written adding all their written premium to the fund, if the program is growing sufficiently rapidly with significant back-loaded contracts, similar to a Ponzi scheme, “reserves” from new contracts could be used to pay claims from older policies, thereby extending the life of the fund even if the contracts are severely underpriced. The example in the Appendix of this overview shows how this can happen.

As with the contract year variation, it could be argued that a claim does not occur until there is a payment made in excess of the aggregate fund balance. If the guarantee policy only guarantees payments if the fund is exhausted in a particular time frame, say a year, then, although the underlying contracts are for multiple years, the guarantee is only a single-year policy with the chance for a loss potentially increasing over the year, depending on the volume and loss characteristics of new business written during the year.

Premiums for guarantee policies are often simple dollar charges per contract written, remitted at the time that the original service contract is written. Since fund trusts are written on a cash flow basis, the chance for a loss early in a program’s life is usually quite small. If premiums are earned in this case over a year, then there is an obvious mismatch between premium charged and potential for loss. If an insurer writes such annual policies and earns its premiums over a year and releases apparent profits, then it is likely that even if the premium were sufficient, assets might not be available to respond to losses when they occur.

The guarantee policy could cover payments on all contracts should the trust become exhausted, without limit to time. Here questions become even more interesting. The policy that we are discussing guarantees the entire fund, though losses on underpriced contracts could be offset by premiums of those more adequately priced. Since the premium is generally paid when original service contracts are written, and since the policy guarantees the aggregate fund, it is unclear when any premium is fully “earned.” Again, a program could experience a number of years of apparently profitable results, with profits extracted from the company, only to find that even though premiums were adequate, there are not sufficient funds remaining to cover liabilities assumed.

2.6. Some regulatory, economic, and legal considerations

The caveats at the beginning of this paper about an ever-changing environment are particularly applicable to any discussion of legal, regulatory, or underwriting issues related to service contracts. Not only is the landscape constantly changing, but many of the regulations themselves are considered (at least by some) as often somewhat vague and subject to different interpretations. As mentioned previously, a complete discussion of the regulatory, legal, and accounting environment is well beyond the scope of this paper and the author’s ability. However we will attempt to at least give a broad view of that environment.

2.6.1. Legal and regulatory environment

We preface all comments here that none of what is presented in this paper should be taken as legal opinion, but rather as the author’s understanding of the legal environment in which service contracts operate, based on his experience in the area. Generally we understand that warranties are explicitly excluded from the definition of insurance in most, if not all, states. As such, manufacturers and, in many cases, sellers can agree to provide service on a product and that contract is not considered to be insurance, nor does it fall under insurance regulation.

As with the regulation of insurance, there are many different regulatory approaches to service contracts in the United States. To some extent, the underlying regulation in a state has a major influence on the structure of a service contract program in that state.

In some states only parties involved in a vehicle sale—for example, manufacturers or sellers—can assume the obligation to repair under a vehicle service contract. Other states allow for a third party to assume the obligation.

We understand that Florida only allows “vehicle service agreement companies,” which are regulated by the Florida insurance department, or licensed insurers to sell vehicle service contracts. Thus, Florida does not allow programs wherein a dealer or some third-party administrator other than an insurer or vehicle service agreement company takes on the obligation to repair a vehicle.

Some states require that service contract programs be covered by a policy issued by an insurer, sometimes of a certain financial rating. Sometimes this coverage is provided by a contractual liability policy, often termed a service contract reimbursement policy. However, these regulations frequently do not specify the type of coverage required, giving rise to the use of trusts guarantee policies as an alternative to a service contract reimbursement policy.

Unfortunately we are not too familiar with the regulatory and legal environment for these contracts outside of the United States and thus cannot comment on the treatment of these contracts in the rest of the world.

As mentioned above, insurers writing certain contracts, including service contract reimbursement policies with a duration of 13 months or longer, are subject to special statutory minimums for unearned premium reserves. Service contract companies not subject to these statutory requirements may be subject to GAAP reporting requirements. We understand that GAAP requirements essentially mirror the second and third calculations of the NAIC statutory test. That is, we understand GAAP requires that a company should hold in reserve the portion of fee income that relates to the part of exposure yet to occur, but in no event less than the present value of the losses and expenses expected to arise in the future. Thus, it is likely that the GAAP unearned fee provision (including any provision for fee deficiency) would be less than or equal to the Statutory provision.

In some jurisdictions outside of the United States, we understand the financial regulator looks to total technical reserves, without the dichotomy between loss reserves and unearned premium (fee) reserves. Here the regulatory issues appear to be a bit more transparent, but surplus regulation may still provide an incentive to use separate administrators or service contract companies.

2.6.2. Observations on economics

One might wonder why the structure of many service contract programs is so complex and so varied. A key to understanding this variety lies in understanding the effect of the interaction between the legal and economic environments. Put briefly, insurers are regulated with statutory accounting rules and regulations that require material amounts of surplus and, in the case of service contract insurers, conservative unearned premium reserves. Service contract administrators generally are not subject to those same requirements.

When a service contract administrator is allowed to operate with less surplus than a similar insurer, one can increase return on total capital (combined surplus) by making use of the service contract administrator as much as possible and minimizing the use of the insurer. In addition, fees charged by the service contract administrator are generally not considered “premiums” when state premium taxes are calculated, giving an additional, though quite minor, incentive to move costs from the insurer.

There appears to be a general bias toward using a third-party administrator when possible, even in states that allow for both a dealer and a third party to be the obligor of the contract. There may be some economic incentive for this approach since it moves more of the transaction costs away from the regulated insurer to the unregulated third-party administrator.

The trusts established by service contract administrators may also not be directly subject to any regulation. If a trust guarantee policy is considered to be insurance to satisfy state law, then a rather sizable volume of business could be guaranteed by the relatively small level of surplus in an insurer established to provide such trust protection. Limiting total capital in this manner increases return on equity but can leave the program quite vulnerable.

As with many risk financing alternatives that exist in traditional insurance, tax considerations also influence the structure of service contract programs. Other than this mention, we will not consider taxes further here.

3. Analysis of experience

As mentioned previously, under a policy that covers the obligation of the obligor in a service contract program, loss and loss adjustment expense reserves are usually small relative to unearned premium reserves, and usual loss period development can be used to estimate them. For a guarantee policy, if the argument above is accepted, then the loss reserve corresponds to the total unpaid liability of the trust fund at the valuation date, for those trust funds that have been exhausted, including claims yet to emerge. Obviously, when considering liabilities for trust guarantee policies, it is critical to assess the viability of the underlying fund at the valuation date.

An obvious approach would be to analyze experience on a contract quarter by valuation quarter development—the traditional contract quarter development approach. If one groups contracts of similar length, then one could expect development on these triangles for a bit longer than the contract term, allowing for development from breakdown to claim payment.

Because of the dichotomy between loss and unearned premium or fee reserves, the liabilities on claims that have occurred need to be evaluated separately from those on future claims. This suggests a rather powerful way of analyzing service contract experience.

As noted previously, analysis of claims by accident quarter and development quarter might be a way to address the loss reserve component of this dichotomy. For the other portion, i.e., the unearned premium reserve, arraying data by contract quarter and then by accident (incident) quarter allows us to focus on the emergence of losses over the life of a contract.

Although the data arrayed in this fashion looks similar to an incremental development triangle, it has a significant difference. Unlike a traditional development triangle arrayed by contract quarter and valuation quarter, we can expect some values in the triangle to continue to develop from one valuation to the next. This is because the component accident quarters are themselves at different ages and, hence, likely to develop differently.

We note, however, that the loss reserve analysis provides insight into the potential for additional development in the contract quarter by accident lag array. The emergence of losses from contract issue to claim occurrence is often beyond the control of a service contract program. However, the administrator and program can have considerable influence on the emergence from the time a claim (breakdown) occurs to the time the final payment is made. In addition, the claim-to-payment lag will likely be quite similar across a variety of contracts in a particular program. Hence, a single accident quarter analysis based on data from many or all contracts in a program will add to the stability of the forecast methods.

With this observation, we can calculate age-to-ultimate factors implied by our accident quarter analysis to develop accident quarter data to ultimate in the various cells of the contract quarter by array of repair lag data. The resulting array would then be the estimated ultimate losses by contract quarter and repair quarter for claims that have occurred. Movement in that data array would then give insight to the emergence of losses over the life of a contract.

Once we have estimated ultimate losses by contract quarter and repair quarter, we can derive ultimate loss estimates by contract quarter as well as estimates of the timing of those losses. We could use usual actuarial methods to derive such estimates. This includes normal development methods and incremental frequency forecasts as well as incremental severity and pure premium forecast methods. As with certain other lines, separate frequency and severity forecasts can lead to better understanding of the underlying characteristics of the contracts involved. This approach presents a benefit if it is used to analyze contracts of the same length. As a result, development will stop at a fixed point in time, known at the start of the analysis; thus, the issue of “tail” is much clearer than in the grouping of contract quarter by valuation quarter data.

When analyzing service contract experience in this manner, we suggest that policies of different length and general characteristics be reviewed separately. Otherwise, changes in contract mix might be misread as changes in underlying emergence patterns. In addition, when analyzing experience under vehicle service contracts, we suggest additional segregation by mileage limitation.

Contract quarter may not be the best way to analyze certain vehicle service contracts, particularly traditional contracts on new vehicles. The presence of “extended eligibility”—that is, “new car” contracts written on cars after the original vehicle in-service date—fundamentally changes contract term and loss emergence during the contract life. For example, an 84 months/100,000 miles traditional new car contract written on a two-year-old car with 24,000 miles will provide the contract holder with five years of coverage for 76,000 miles from the date of contract issue. In addition, since the manufacturer warranty would likely only run for another 12 months or 12,000 miles, we would expect to see losses emerge sooner from the contract date than if the same contract were written on the same car at the time it was first put into service.

As such, we would suggest that analysis of traditional new car experience be conducted on an in-service quarter by repair quarter basis, as opposed to contract quarter, and, in addition, that contracts be further subdivided based on the length of time from the in-service quarter and the policy quarter. This approach preserves the uniform expiration date of the contracts being analyzed, and it at least partially overcomes the different timing of the expiration of the OEM warranty within a group of policies being analyzed. The in-service quarter forecasts can then be allocated to contract quarter making use of experience sorted by policy quarter and in-service quarter.

Hybrid contracts also present challenges for analysis. Here, we would suggest contract quarter organization but with contracts subdivided by vehicle mileage at contract issue.

The foregoing discussion made the implicit assumption that there is sufficient history available for a particular contract term to be able to assess loss emergence over the life of the contract. It is often the case that a particular contract term or variation is new, without a complete history available. In these cases, one could look to similar terms that have actual experience and adjust the resulting emergence patterns for recognized differences. Another tool would be simulation models built to estimate emergence over a broad range of contracts and calibrated to reasonably track actual observed experience under those contracts for which experience is available. The paper by Hayne [1] contains a considerable discussion of this and other methods that can be used to analyze service contract experience.

Analysis for trust policies would seem to require, at the minimum, a thorough analysis of the underlying program using methods similar to those outlined here. This analysis could then be used to review cash flows, including expected interest income on fund assets to determine the likelihood of the trust being exhausted. In the case of a trust guarantee that covers inception-to-date business, unless the fund has been exhausted at the valuation date, its future viability depends not only on the profitability of the business already on the books, but also on future income, including investment income and “reserves” on new contracts. It is not clear to what extent this level of analysis is currently being done on guarantee contracts in the industry.

3.1. Common rating variables

As with other aspects of service contract programs, there are a variety of rating plans used to reach the “wholesale” price that sellers pay to the issuer of the contracts or the premiums that insurers charge for reimbursement or other policies involved in such a program. Almost universally, the length of term of a service contract is a major factor in the amount charged. Other factors such as item value, deductible, coverage options, and the reliability of particular brands or models are also usually considered. In addition, for vehicle service contracts, contract mileage and the difference between policy date and vehicle in-service date are also usually considered in rating. In some vehicle contract programs, there might be scheduled credits and debits that affect the final dealer’s cost for a program.

3.2. Some methods to track performance

Probably the best way to assess the profitability of a particular service contract term is to analyze the development history in detail as described in earlier sections. However, analysis in this level of detail is time-consuming and not efficient for situations where data might be sparse—for example, in assessing the efficiency of product classification relativities, and so forth.

In such situations, those administering service contract programs often rely on loss ratios of incurred losses divided by premiums, fees, or, more commonly, “reserves” earned using “earning curves” that are intended to track the emergence of losses over the life of a contract. Before relying on earning curves, one should test how well they do at tracking loss emergence. A very simple test would be to assemble a triangle of loss ratios by contract period (month, quarter, year, etc.), and valuation period. If the loss ratios for a contract period move randomly over time, then one might get some assurance that premium earnings that are tracking loss emergence and loss ratios might prove useful in monitoring experience. If, however, the ratios tend to move upward or downward over time, then loss ratios should only be relied upon with extreme caution, if at all.

Reliance on calendar year loss ratios can be particularly perilous. If premiums are brought into income more rapidly than losses emerge, then calendar year loss ratios will tend to understate true experience, leading to erroneous conclusions regarding business expansion and rate change needs. If such is the case, then the contract year loss ratios discussed in the prior paragraph will tend to increase over time for a fixed contract year, reinforcing the need to assess the appropriateness of the factors used to earn premium.

The appropriateness of earning patterns can also be affected by changes, among other factors, in the following:

-

Contract provisions

-

OEM warranties

-

Product quality

-

Consumer behavior

Because of this, it is very helpful and sometimes necessary to check the appropriateness of earning patterns frequently and to definitely do so before major decisions regarding a service contract program are undertaken.

We note that these cautions assume that the rate at which premiums or fees are earned matches the emergence of losses. If the earning pattern that a company uses is calibrated to match the minimum allowed unearned premium under U.S. statutory accounting, then it will likely not match the emergence of losses and will probably be slower. In this case, loss ratios for a fixed contract period would likely decrease over time, possibly leading to overly pessimistic views of profitability and rating needs.

Acknowledgments

The author would like to acknowledge the substantial contributions made by several individuals in the preparation of this paper. First, thanks to Ralph Blanchard and John Purple who first suggested I put this work together and offered guidance and suggestions on earlier drafts. Thanks also go to the anonymous reviewers whose comments and suggestions have improved this paper. As always, responsibility for errors remains with the author.