1. Introduction

Against the background of substantial changes in competition, capital market conditions, and supervisory frameworks, holistic analysis of an insurance company’s assets and liabilities becomes particularly relevant. One important tool that can be used for such analysis is dynamic financial analysis (DFA). DFA is a systematic approach to financial modeling in which financial results are projected under a variety of possible scenarios by showing how outcomes are affected by changing internal and external conditions. DFA is employed for a variety of management-relevant purposes, including solvency monitoring, performance measurement of business segments, capital allocation, and analysis of major risks, such as inflation risk, interest rate risk, and reserving risk (Hodes, Feldblum, and Neghaiwi 1999). Other fields of application include strategic asset allocation, determination of optimal growth rate in the underwriting business, and analysis of alternative reinsurance decisions.

The discussion in Europe about new risk-based capital standards (Solvency II) and the development of International Financial Reporting Standards (IFRS), as well as expanding catastrophe claims, have made DFA an important tool for cash flow projection and decision making, especially in the nonlife and reinsurance businesses (for an overview, see Blum and Dacorogna 2004). However, several issues in the implementation of a DFA system have not been considered thoroughly in the DFA literature to date. One of these is the integration of management strategies in DFA, which is the aim of this paper. We see two reasons why modeling management is essential to DFA. First, management behavior reflects the company’s reaction to its environment and to its financial situation. Thus, suitable management rules are needed to make multiperiod DFA more meaningful. Second, management can use DFA to test different strategies and learn from the results in a theoretical environment, thereby possibly preventing costly real-world mistakes. Management responses include long-term strategies as well as management rules, which are rather short-term decisions and reactions to actual needs.

The literature contains several surveys and applications of DFA. The DFA Committee of the Casualty Actuarial Society started developing simulation models for use in a property/casualty context in the late 1990s; the committee’s results are reported in a DFA handbook (Casualty Actuarial Society, Dynamic Financial Analysis Committee 1999). In an overview, Blum and Dacorogna (2004) present the elements and the main value proposition of DFA. Lowe and Stanard (1997) and Kaufmann, Gadmer, and Klett (2001) both provide an introduction to this field by presenting a model framework, followed by an application of the model. Lowe and Stanard (1997) present a DFA model for a property-catastrophe reinsurer to handle the underwriting, investment, and capital management process. Furthermore, Kaufmann, Gadmer, and Klett (2001) provide a framework made up of the most common components of DFA models and integrate these components in an up-and-running model. Blum et al. (2001) use DFA for modeling the impact of foreign exchange risks on reinsurance decisions; D’Arcy and Gorvett (2004) apply DFA to determine an optimal growth rate in the property/casualty insurance business. Using data from a German nonlife insurance company, Schmeiser (2004) develops an internal risk management approach for property-liability insurers based on DFA, an approach that European Union—based insurance companies could use as an internal model to calculate their risk-based capital requirements under Solvency II.

It is generally agreed that implementing management strategies and rules is a necessary step to improve DFA (e.g., D’Arcy et al. 1997; Blum and Dacorogna 2004). But although DFA is regularly mentioned as a helpful tool to test management strategies and rules (e.g., D’Arcy et al. 1997; Wiesner and Emma 2000), very little literature directly addresses the implementation of such rules. Daykin, Pentikäinen, and Pesonen (1994) describe the implementation of a response function to changes in the insurance market. Thereby, the authors’ aim is to present possible management reactions to market changes, not to consider a holistic model of an insurer that demonstrates the effects of certain management strategies. The same holds true for Brinkmann, Gauss, and Heinke (2005), who present a discussion of management rules within a stochastic model for the life insurance industry.

The goal of this paper is to implement different management strategies in DFA and study their effects on the insurer’s risk and return position in a multiperiod context. Thereby, we compare the outcomes of our DFA model with and without the implementation of specific management strategies. This effort will yield results of interest to insurers in their long-term planning processes.

Our starting point is a DFA framework containing essential elements of a nonlife insurance company (Section 2), which is followed by developing typical management reactions to the company’s financial situation (Section 3). In Section 4, we define financial ratios, reflecting both risk and return of these strategies in a DFA context. A DFA simulation study to test the management strategies and examine their effects on risk and return is presented in Section 5. Finally, Section 6 concludes.

2. Model framework

In this section we present the model framework and its assumptions. A summary of all variables used can be found in the Appendix. We denote as the equity capital of the insurance company at the end of time period and as the company’s earnings in For a time period the following basic relation for the development of the equity capital is obtained:

\[ E C_{t}=E C_{t-1}+E_{t} . \tag{2.1} \]

The earnings in period comprise the investment result, and the underwriting result, Taxes are paid contingent on positive earnings. The tax rate is denoted by :

\[ E_{t}=I_{t}+U_{t}-\max \left(t r \cdot\left(I_{t}+U_{t}\right), 0\right) . \tag{2.2} \]

As is often done in research of this type (e.g., Doherty and Garven 1986), we have greatly simplified the tax code for purposes of clarity in what follows. For instance, many national tax systems contain provisions allowing losses to be carried forward or backward in time, at least to a certain extent. Therefore, in “real” life, no doubt quite a few insurance practice management decisions are tax driven (for an overview, see Doherty 2000). However, due to the tax structure simplification as set out in Equation (2.2), our model cannot take such subtleties into consideration.

On the asset side, high-risk and low-risk investments can be taken into account. Highrisk investments typically consist of stocks, highyield bonds, or alternative investments such as hedge funds and private equity. Low-risk investments are mainly government bonds or money market instruments. The portion of high-risk investment in the time period is denoted by The rate of return of the high-risk investment in is given by and the return of the low-risk investment in is denoted by The rate of return of the company’s investment portfolio in is represented by:

\[ r_{p t}=\alpha_{t-1} \cdot r_{1 t}+\left(1-\alpha_{t-1}\right) \cdot r_{2 t} . \tag{2.3} \]

The company’s investment results can be calculated by multiplying the portfolio return with the funds available for investment :

\[ I_{t}=r_{p t} \cdot A_{t-1} . \tag{2.4} \]

The capital to be invested between and equals the equity capital for the prior period, plus the premium income less upfront expenses.

The other major portion of an insurer’s income is generated by the underwriting business. We denote as the company’s share of the associated relevant market volume in Thereby we assume to represent the whole underwriting market accessible to the insurance company. The volume of this underwriting market is denoted by The achievable premium level differs, depending on the prevailing market phase. We assume that the underwriting cycle follows a Markov process. Therefore, we account for so-called transition probabilities, indicating the probability of the underwriting cycle to switch from one state to another (Kaufmann, Gadmer, and Klett 2001; D’Arcy et al. 1998). We use a business cycle comprising three possible states. State 1 is a very sound market phase, which leads to a high premium income. For State 2, we set a medium premium level. State 3 is a soft market phase combined with a low premium level. The variables denote the probabilities of switching from one state to another, leading to the following transition matrix:

\[ p_{s j}=\left(\begin{array}{lll} p_{11} & p_{12} & p_{13} \\ p_{21} & p_{22} & p_{23} \\ p_{31} & p_{32} & p_{33} \end{array}\right) .\tag{2.5} \]

For instance, being in State 1, p11 denotes the probability of staying in State 1, and p12 (p13) stands for the probability of moving to State 2 (3). The premium income thus depends on underwriting cycle factor for the three states s = 1, 2, 3. Besides the underwriting cycle, the premium income is linked to a consumer response function. Empirical evidence shows that a rise in default risk leads to a rapid decline of the achievable premium level (Wakker, Thaler, and Tversky 1997). Thus, the consumer response function represents a link between the premium written and the company’s safety level. Therefore, the consumers in our model will buy insurance only if the premium is reduced accordingly. The safety level is determined by the equity capital at the end of the previous period and the consumer response function is described by the parameter cr. Including both underwriting cycle and consumer response in our model leads to the premium income:

\[ P_{t-1}=c r_{t-1}^{E C_{t-1}} \cdot \pi_{t-1}^{s} \cdot \beta_{t-1} \cdot M V. \tag{2.6} \]

Claims are denoted by and expenses by Expenses consist of upfront costs and claim settlement costs Using the variable one fraction of the upfront expenses depends linearly on the market volume written. Increasing or decreasing the underwriting business entails additional costs (modeled with the factor ), e.g., for advertising and promotion efforts. This part of the upfront costs is calculated using a quadratic cost function. The upfront costs can then be obtained from the relation Claim settlement costs are a percentage of the claims incurred Thus, we obtain the underwriting result by the relation:

\[ U_{t}=P_{t-1}-C_{t}-E x_{t-1}^{P}-E x_{t}^{C} . \tag{2.7} \]

At the beginning of each period t, management has the option of altering two variables of the model: α denotes the portion of the risky investment and β stands for the market share in the underwriting business.

3. Management strategies

To make DFA projections more realistic and thus more useful, it is crucial to incorporate management strategies into the model. Especially regarding long-term planning, the inclusion of management strategies provides a more reliable basis for decision making.

However, most DFA models contain very few of these management responses and therefore it is our aim to present a framework allowing implementation of management rules and strategies. The rules presented in this paper are response mechanisms to the actual financial situation of the insurance company. Thus, the portion of the risky investment α and the market participation rate β are dynamically adjusted. In this context, we address three basic questions.

3.1. What is management’s goal (the target)?

Management has a complex set of different business objectives (e.g., maximization of profits, satisfaction of stakeholder demands, or maximization of its own utility). On the one hand, the strategy might require fast intervention—for example, in the case of a dangerous financial situation. On the other hand, the strategy can be long-term-oriented, e.g., when deciding on a long-term growth target. The design of current management strategy can thus be manifold, depending on the actual situation of the enterprise and management’s goals. In distressed situations, management may act to reduce risk in order to avoid insolvency; however, it is also possible that it might act in exactly the opposite direction—to increase the risk. Keeping the limited liability of insurance companies in mind, this behavior could look quite rational from the shareholders’ point of view, since their return profile corresponds to a call option (Gollier, Koehl, and Rochet 1997; Doherty 2000). Even when the company’s financial position is good, management strategies can go in both directions, either to increase the risk (e.g., for enhancing income from option programs) or to reduce the risk (e.g., to fix a certain level of profits).

Moreover, a combination of both strategies (increase and decrease the risk) might be rational in certain situations, possibly motivated by a growth target. Management might follow a risk-reduction strategy when the equity capital is under a certain level, but if the equity capital is above a certain level, an increase in risk could be induced.

3.2. When does management react (the trigger)?

There are different triggers that can induce management reaction. The trigger used in this paper is the level of equity capital at the end of each period. Especially in the context of the European capital standards (“Solvency I”), the minimum capital required (MCR) is a highly critical equity capital level; if the firm’s capital drops below this level, the regulatory authority will intervene. However, we do not expect that management would wait until the equity capital falls below the MCR, but would have some sort of early warning signal. For example, the trigger could be set to the MCR plus 50%.

Financial ratios could also be used as a trigger for management reaction. The return on investment (ROI), a common ratio in business management, indicates the compounded return based on the equity capital invested and can be compared with the ROIs of other investment opportunities with the same risk level. A possible trigger from the field of solvency analysis is the expected policyholder deficit (EPD), analyzing the expected costs of ruin (Butsic 1994).

Finally, as management reactions depend on the development of asset and insurance markets, instead of looking at how the total equity capital develops, management might focus on the company’s investment and its underwriting business. Because responsibility for asset and liability management are still separated in some insurance companies, the company’s investment and underwriting results could become a third possible trigger for management responses.

3.3. How does management react (the rule)?

How would management react to a specific event when following a certain management strategy? For example, would management engage in risk reduction whenever the equity capital comes close to falling below the requirements of Solvency I MCR by reducing asset volatility? Or would it take some other course of action?

With respect to our model framework, management can control two basic parameters. Parameter α regulates the asset side by adjusting the share of risky investments; parameter β controls the underwriting market participation. A combined approach would involve simultaneously changing assets (α) and liabilities (β).

From a wide range of applicable rules, we choose a set of easy logic rules such as “if-then” for the simplest case, where the trigger is denoted by “if” and the operating action would be activated by “then.” But other rules such as “if-then-else” are also possible. Table 1 summarizes the different management strategies analyzed in this paper.

3.4. Management strategy 1: “solvency”

The solvency strategy is a risk-reducing strategy. For each point in time (t = 1, . . . , T − 1), α and β is decreased by 0.05 each as soon as the equity capital falls below the critical value defined by the MCR plus a safety loading of 50%.

3.5. Management strategy 2: “high-risk”

The risk reduction strategy seems favorable especially for the policyholders, because it increases the safety level. However, as mentioned before, it might be rational for the shareholders to choose a risk-taking strategy in case of financial distress because of their limited liability. Therefore, the high-risk strategy is the exact opposite of the solvency strategy: should the equity capital fall below the MCR, including a safety loading of 50%, α and β are increased by 0.05.

3.6. Management strategy 3: “growth”

The growth strategy combines the solvency strategy with a growth target for the underwriting business. Should the equity capital drop below the MCR plus the safety loading of 50%, the same rules apply as in the solvency strategy. If the equity capital is above the trigger, we assume a growth of 0.05 in β.

4. Measurement of risk, return, and performance

What measures appropriately reflect risk, return, and performance of the management strategies outlined in the previous section? In Table 2, we propose eight financial ratios.

With the expected gain from time 0 to is denoted. The expected gain per annum can then be written as:

\[ E(G)=\frac{E\left(E C_{T}\right)-E C_{0}}{T} . \tag{4.1} \]

While E(G) represents an absolute measure of return, the return on invested capital measures a relative return. Let ROI denote the expected return on the company’s invested equity capital per annum. Based on the relation

\[ E C_{0} \cdot(1+\mathrm{ROI})^{T}=E\left(E C_{T}\right), \tag{4.2} \]

we obtain for the ROI:

\[ \mathrm{ROI}=\left(\frac{E\left(E C_{T}\right)}{E C_{0}}\right)^{1 / T}-1. \tag{4.3} \]

Risk can be any measure of adverse outcome considered relevant (Lowe and Stanard 1997). We distinguish between measures for total and downside risk. Because it takes both positive and negative deviations from the expected value into account, the standard deviation represents a measure of total risk. The standard deviation of the gain σ(G) per annum can be obtained as follows:

\[ \sigma(G)=\frac{1}{T} \cdot \sigma\left(E C_{T}\right). \tag{4.4} \]

In addition to the standard deviation, risk in the insurance context is often measured using downside risk measures like the ruin probability (RP) or the EPD (Butsic 1994; Barth 2000). Downside risk measures differ from total risk measures in that only negative deviations from a certain threshold are taken into account. In this context, the ruin probability is defined by

\[ \mathrm{RP}=\operatorname{Pr}(\tau \leq T), \tag{4.5} \]

where with describes the first occurrence of ruin (i.e., a negative equity capital). However, the ruin probability does not provide any information regarding the severity of insolvency (e.g., Butsic 1994; Powers 1995). To take this into account, the EPD can be applied

\[ \mathrm{EPD}=\sum_{t=1}^{T} E\left[\max \left(-E C_{t}, 0\right)\right] \cdot\left(1+r_{f}(0, t)\right)^{-t}, \tag{4.6} \]

where stands for the risk-free rate of return between 0 and

Moreover, performance measures that take risk and return into account can be applied. The most widely known performance measure is the Sharpe ratio, which considers the relationship between the risk premium (mean excess return above the risk-free interest rate) and the standard deviation of returns (Sharpe 1966). Applying this ratio to our DFA framework, we obtain:

\[ \mathrm{SR}_{\sigma}=\frac{E\left(E C_{T}\right)-E C_{0} \cdot\left(1+r_{f}\right)^{T}}{\sigma\left(E C_{T}\right)} . \tag{4.7} \]

In the numerator, the risk-free return is subtracted from the expected value of the equity capital in T. Using the standard deviation as a measure of risk, for the Sharpe ratio also, positive deviations from the expected value are an indication of performance reductions. However, since risk can be understood as downside potential, the probability of ruin or the EPD in the denominator of the Sharpe ratio can be used in the following sense:

\[ \mathrm{SR}_{\mathrm{RP}}=\frac{E\left(E C_{T}\right)-E C_{0} \cdot\left(1+r_{f}\right)^{T}}{\mathrm{RP}}, \tag{4.8} \]

\[ \mathrm{SR}_{\mathrm{EPD}}=\frac{E\left(E C_{T}\right)-E C_{0} \cdot\left(1+r_{f}\right)^{T}}{\mathrm{EPD}}. \tag{4.9} \]

5. Simulation study

5.1. Model specifications

In the simulation study, we consider a typical German nonlife insurance company, using corresponding data and German solvency rules. Given a time period of T = 5 years, decisions concerning parameters α and β can be made at the beginning of each year. Parameters α and β can be changed in discrete steps of 0.05 within the range of 0 to 1. The market volume MV (i.e., β = 1) of the underwriting market accessible to the insurance company is set to €200 million. In t = 0, the insurer has a share of β0 = 0.2 in the insurance market, so that the premium income for the insurer in State 2 (π2 = 1) is €40 million. In a favorable market environment (State 1), a higher premium income can be realized for the given market volume. Thus, the premium is adjusted by the factor π1 = 1.05. In the disadvantageous State 3, the factor π3 = 0.95 is used. The transition probabilities from one state to another follow the matrix:

\[ p_{s j}=\left(\begin{array}{lll} 0.1 & 0.5 & 0.4 \\ 0.2 & 0.6 & 0.2 \\ 0.3 & 0.5 & 0.2 \end{array}\right) . \tag{5.1} \]

The expenses incurred for the premium written are given by the relation Taxes are paid at the end of each period, given a constant tax rate of The consumer response parameter is 1 (0.95) if the equity capital at the end of the last period is above (below) the MCR.

We assume normally distributed asset returns. Thus, the continuous rate of return has a mean of 10% (5%) and a standard deviation of 20% (5%) in case of a high- (low-) risk investment. Equation (2.3), the return rate of the company’s investment portfolio, can be written as:

\[ \begin{aligned} r_{p t}= & \alpha_{t-1} \cdot(\exp (N(0.10,0.20))-1)+\left(1-\alpha_{t-1}\right) \\ & \cdot(\exp (N(0.05,0.05))-1) \end{aligned}. \tag{5.2} \]

Data from the German regulatory authority (BaFin) served for calculating the asset allocation. German nonlife insurance companies typically invest approximately 40% of their wealth in high-risk investments such as stocks, high-yield bonds, and private equity, while the remaining 60% is invested in low-risk investments such as government bonds or money market investments (BaFin 2005, Table 510). Thus, we set α0 = 0.40 as the starting point for the asset allocation. The risk-free rate of return rf is 3%.

Using random numbers generated from a lognormal distribution with a mean of and a standard deviation of claims are modeled (see BaFin 2005, Table 541). The expenses of the claim settlement are determined by a 5% share of the random claim amount (BaFin 2005, Table 541).

For calculating the minimum capital required, Solvency I rules as adopted in the European Union are utilized. The minimum capital thresholds based on premiums are 18% of the first €50 million and 16% above that amount. The margin based on claims, which is 26% on the first €35 million, and 23% above that amount, is used if the calculated amount exceeds the minimum equity capital requirements determined by the premium-based calculation (see EU Directive 2002/13/EC). Applying these rules, we assign a minimum capital requirement of E8.84 million for t = 0 as a result of calculating the maximum of 18% · €40 million and 26% · €34 million. In compliance with Solvency I rules, the insurance company is capitalized with €15 million in t = 0, which corresponds to an equity to premium ratio of 37.5%, a typical figure for German nonlife insurance companies (BaFin 2005, Table 520).

All model parameters and their initial values are summarized in the Appendix. Because the simulation study considers a typical German insurance company, applying the model to other business and regulatory structures will require some adjustments to asset allocation, claims ratio, expense ratio, regulatory rules, and so forth. For example, compared to the situation in Germany, the claims ratio is usually higher in the United States and lower in Japan, whereas the expense ratio is usually lower in the United States and higher in Japan compared to Germany (Swiss Re 2006). Also, different regulatory rules need to be taken into consideration: for example, risk-based capital standards within the U.S. regulatory framework or solvency margin standards within the Japanese environment (e.g., Eling, Schmeiser, and Schmit 2007).

5.2. Results

In Table 3 we present simulation results calculated on the basis of a Latin-Hypercube simulation with 100,000 iterations (for details on Latin-Hypercube simulation, see, e.g., McKay, Conover, and Beckman 1979).

In the case where no management strategy is applied, we find an expected gain of €5.57 million per annum with a standard deviation of €2.88 million. The expected return on the invested equity capital is 23.35%. The ruin probability amounts to 0.22%, which is far below the requirements of many regulatory authorities (e.g., given the Solvency II process in the EU, a ruin probability lower than 0.50% is required; see CEIOPS 2007, 58).

Risk is reduced much more applying the solvency strategy. While the return remains almost unchanged (the expected gain decreases by 2% from €5.57 million to €5.46 million per annum), we find much lower values for the downside risk measures. The ruin probability is 0.06% and the EPD €0.0006 million. This figure is less than 15% of the value where no management strategy is applied. Thus, the solvency strategy avoids most insolvencies without affecting return much. As a result, this strategy leads to higher performance measures based on ruin probability and EPD. For example, the SRRP is 44.53 instead of 11.36. We can thus conclude that the solvency strategy effectively reduces downside risk and provides valuable insolvency protection. Interestingly, risk is not reduced when both positive and negative deviations from the expected value are taken into account, because the standard deviation is 3% higher compared to the “no strategy” case (€2.95 million versus 2.88 million per annum). This outcome is because reducing the participation in insurance business and amount of the risky investment changes the level of earnings within different time periods, resulting in an increased standard deviation. Because of the higher standard deviation and the lower return, the Sharpe ratio for this strategy is slightly decreased compared to the “no strategy” case.

The high-risk strategy, which is the opposite of the solvency strategy, will obviously result in a risk and return profile that is in direct contrast to that of the solvency strategy. Compared to the model without a strategy, the expected gain per annum rises by 2%, from €5.57 million to €5.70 million. However, we also find a strong increase in downside risk: both ruin probability (0.63%) and EPD (€0.0225 million) are much higher than in the case where no strategy is applied. As the increase in risk is much higher than the increase in return, the performance measures based on downside risk are very low compared to the other strategies. The standard deviation of €2.89 million per annum is comparable to the standard deviation found with the solvency strategy, and confirms our hypothesis that the standard deviation is mainly driven by changes in the level of earnings.

The growth strategy is much more flexible than the previous strategies. Here, parameter β must be changed at the end of each period, while with the other strategies, β is changed only when the equity capital falls below the given trigger. Therefore, we obtain a completely different risk return profile, where a higher return is accompanied by higher risk. The expected gain per annum now amounts to €7.30 million, 31% above the €5.57 million obtained when no specific management strategy is applied. The percentage increase in standard deviation is comparable with the increase in return, as the standard deviation (€4.19 million per annum) is 45% higher. However, the ruin probability (0.20%) is 10% lower and the EPD (€0.035 million) is 22% lower compared to the situation without a strategy. The performance values for SRRP and SREPD are thus higher compared with the “no strategy” case. Therefore, the growth strategy seems to work quite well. In comparison to the solvency strategy, the growth strategy is suitable for those managers pursuing a higher return level and who are also willing to take a higher risk.

In “real life” insurance practice, there are often important (and difficult) differences between, on the one hand, the organization and team interaction of the risk management group and the actuaries who are responsible for developing and calibrating DFA models like the one discussed in this paper, and, on the other hand, top management. Because of implied model risk and the many assumptions necessary to run a cash flow simulation model, the results under different scenarios cannot, and indeed should not, be used as the sole basis for a management decision. Instead, model results are better employed as support, either for or against different strategies. How the statistical outputs of a DFA model are communicated to top management is crucial. Not everybody enjoys reading statistics like those presented in Table 3, and it is essential, from every point of view, that management not be made to feel uncomfortable when confronted with model results that could, if presented well, be very useful to decision making. However, we also believe that management needs to become a little more flexible in its decision-making process, looking at things more in terms of “probable” than “certain,” for example. Effective communication of results and effective use of results can be hugely important to a firm’s success and to this end, we recommend the use of more intuitive forms of communication—graphs and diagrams, for example, instead of long lists of numbers, complicated tables and equations.

5.3. Robustness of results

In this section, we check the robustness of our findings. It is crucial to verify whether our main findings hold true whenever main input parameters are changed, particularly as the results presented in Section 5.2 are based on specific input parameters (e.g., the level of equity capital, the time horizon, or the starting values for α and β).

In what follows, we consider the results presented in the last section to be robust, given that the basic relations between the analyzed management strategies remain unchanged. For example, we expect the solvency strategy to have a lower return but also a decreased risk compared to the other strategies, independent, e.g., of the equity capital level in t = 0. As before, all tests have been calculated on the basis of a Latin-Hypercube simulation with 100,000 iterations.

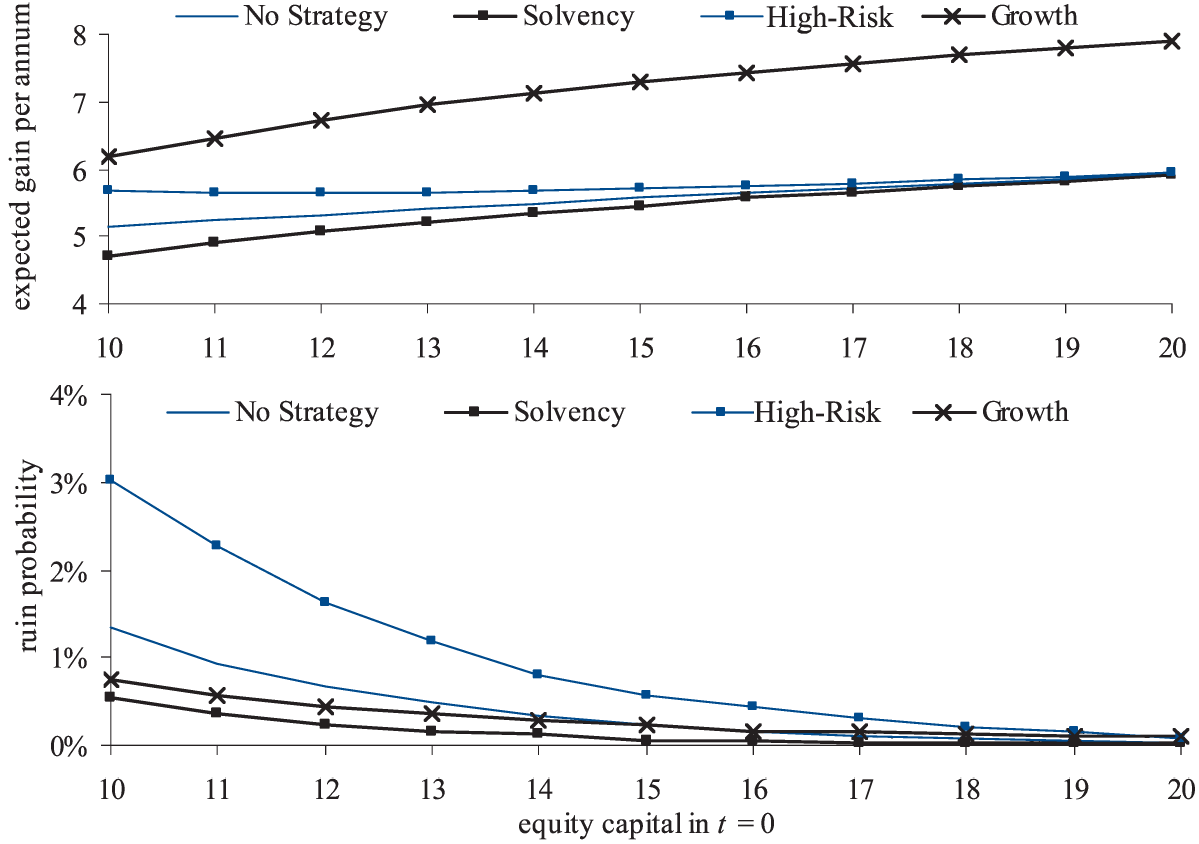

5.3.1. Variation of equity capital

The level of equity capital in t = 0 determines the company’s safety level. The results in Section 5.2 may change for different levels of safety. In Section 5.2 the level of equity capital has been set at €15 million. To test the implications of different equity capital levels, we vary the equity capital in t = 0 from €10 to €20 million in €1 million intervals. The results are shown in Figure 1, where the expected gain per annum is displayed in the upper part of the figure and the ruin probability for different levels of equity capital in the lower part.

With an increasing level of equity capital, the expected gain per annum converges toward €5.9 million when applying the “no strategy” case, the solvency strategy, and the high-risk strategy. This is because an increasing level of equity capital results in fewer shifts of the parameters α and β. For example, given an equity capital of €20 million in t = 0, only very few cases where the equity capital is below the trigger level can be found; hence almost no difference between these three strategies can be identified. In contrast, the expected gain per annum increases with the growth strategy. Given an increasing level of equity capital, we find more shifting toward a higher participation in the insurance market with the growth strategy, which increases the expected gains. However, the basic relations remain unchanged for all strategies. Hence, the results of the last section are robust with respect to the expected gain per annum. The same holds true for the ruin probability, except in the case of the growth strategy, where risk does not decrease as fast as with the other strategies. The reason for this is that “growth” is the only strategy where the risk is increased with higher equity capital.

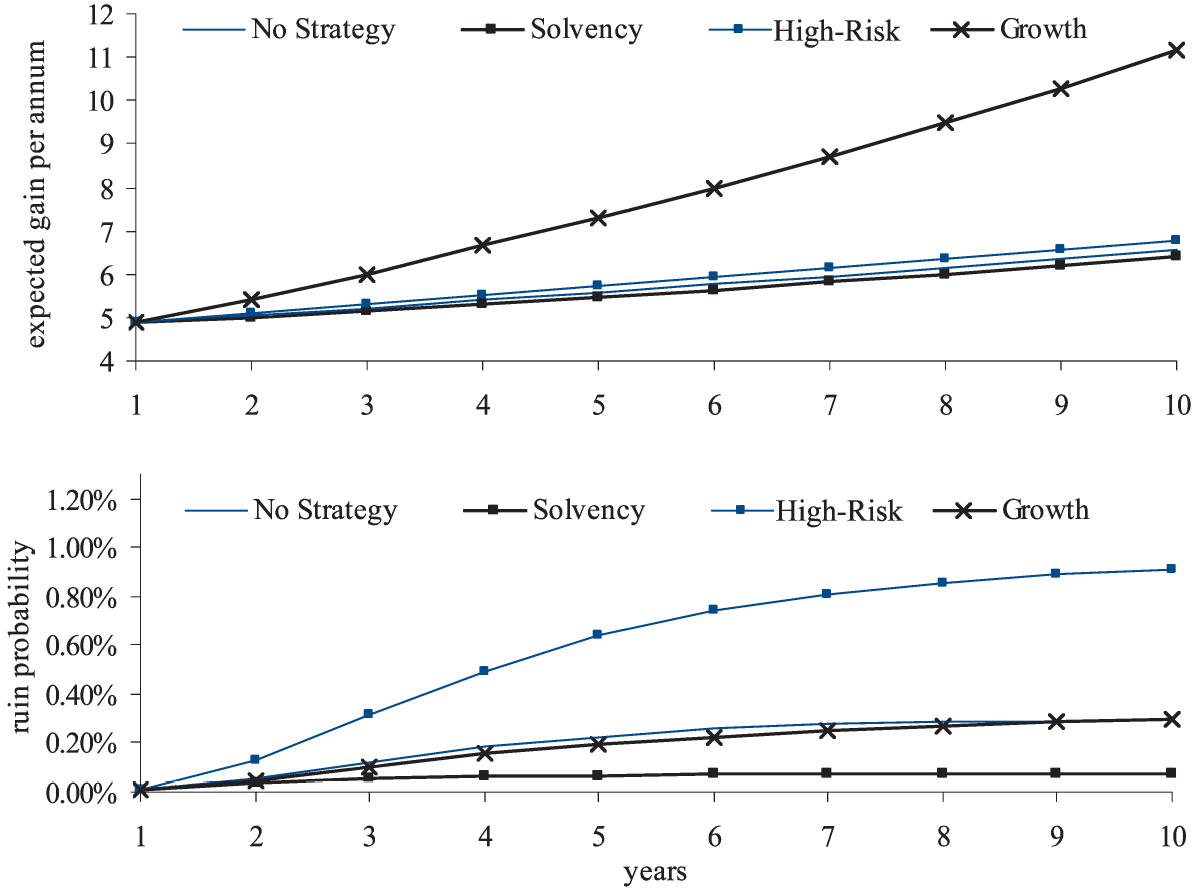

5.3.2. Variation of time horizon

In general, the time horizon observed is very important in interpreting DFA results. If the observed time period is short, the DFA results may not be relevant for strategic decision making. However, with longer time periods, issues like data uncertainty or the variability of outputs gain significance. The longer the time period, the more uncertain is the input data, producing greater variability of the results. In Section 5.2, we chose a time horizon of 5 years. To check the implications of different time horizons on our results, we varied the time horizon from 1 to 10 years in yearly intervals. The results are presented in Figure 2.

For all strategies the expected gain and the ruin probability increases whenever the time horizon is expanded. All the basic relations set out in Section 5.2 between the different strategies remain unchanged; thus, the results are robust regarding a variation of the time horizon.

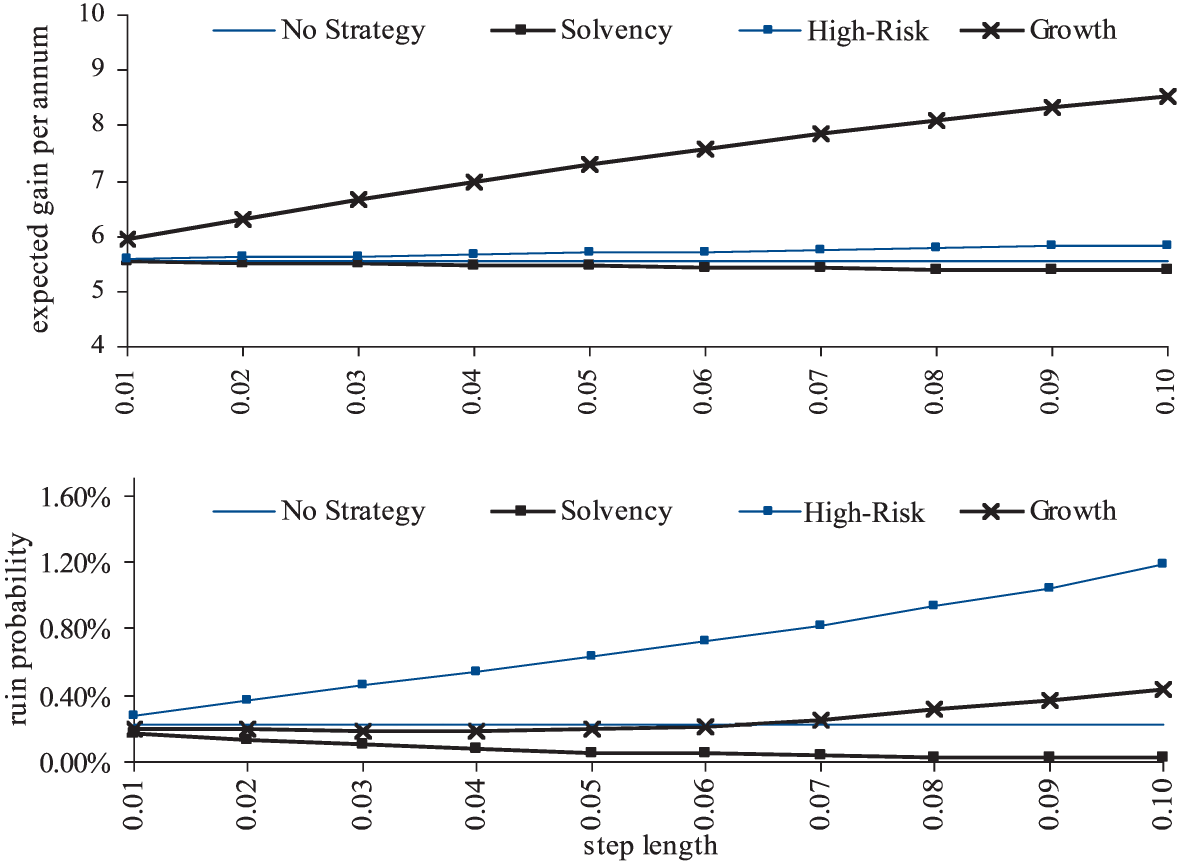

5.3.3. Variation of the parameters α and β

The changes in α and β determine the intensity of management reactions in our DFA study. For the results presented in Section 5.2, management was confined to vary the parameters α and β in increments of 0.05. But what if management applies other increment sizes, e.g., changes α and β by 0.1 or, alternatively, only makes 0.01-increment-size changes? To discover the effect of the interval length on our results, we varied the intervals of α and β from 0.01 to 0.1 in steps of 0.01. The results are shown in Figure 3.

Again we find our results to be robust with respect to our findings in Section 5.2. All basic relations between the strategies remain unchanged. While the expected gain stays almost unchanged with no strategy, the solvency strategy, and the high-risk strategy, we find a higher return applying the growth strategy. This increased return is because, with increasing step length, the positive effect of a growth in β on the expected gain rises. Similar results are found with respect to the ruin probability.

5.3.4. Variation of starting values

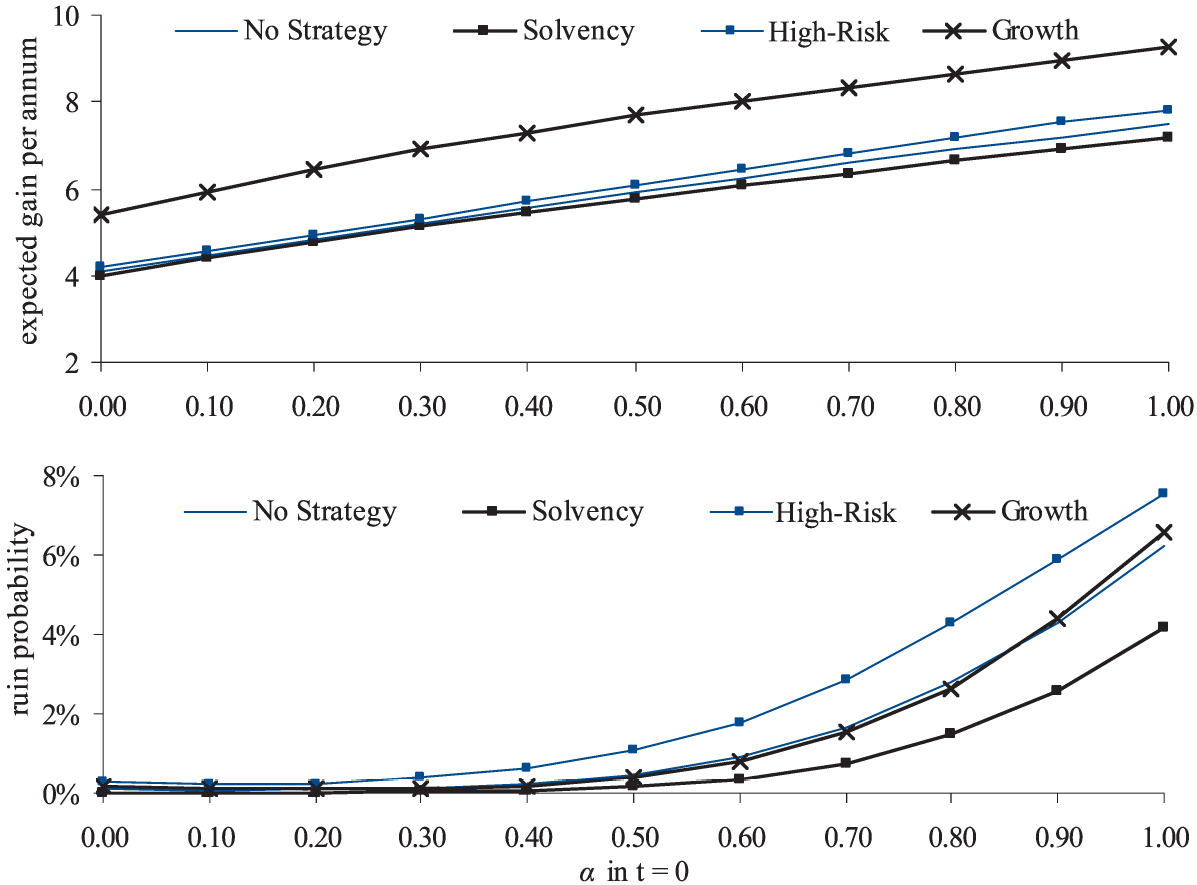

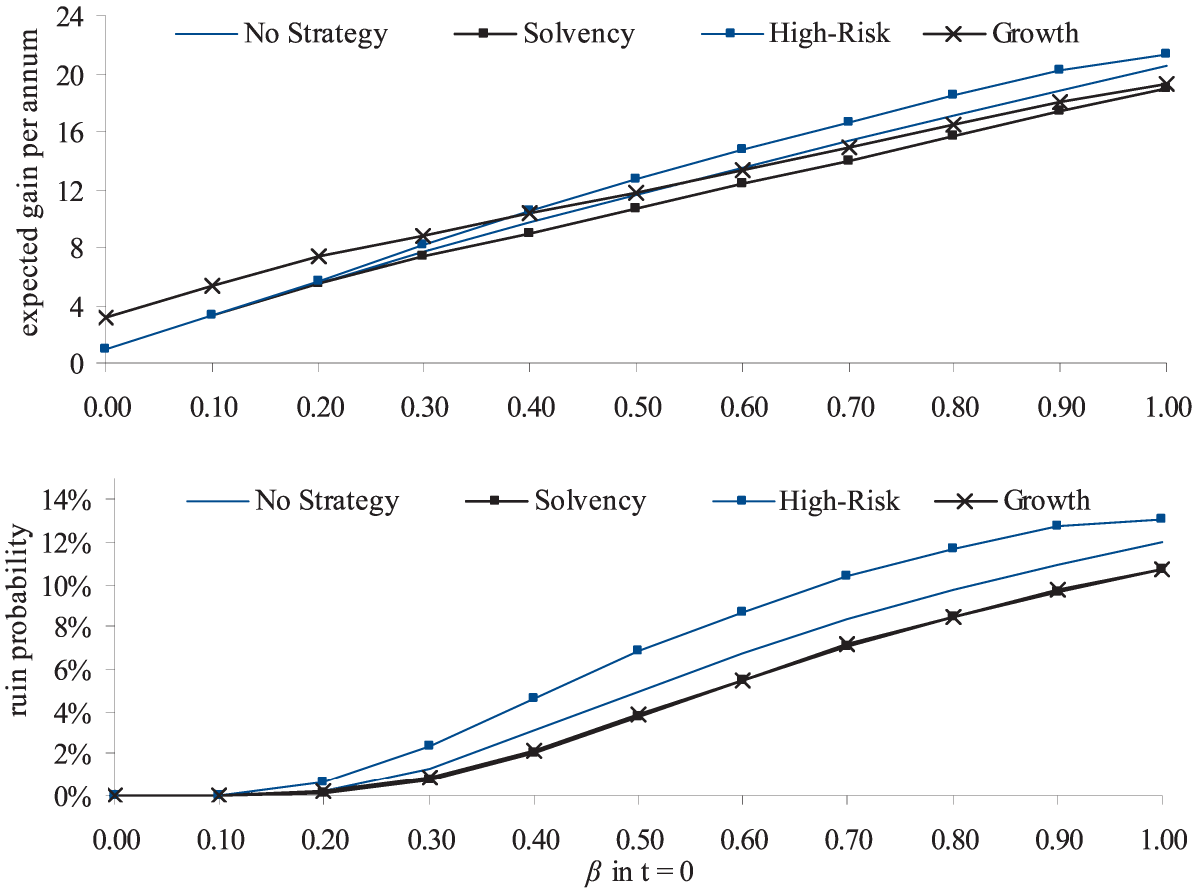

In Section 5.2, the share of risky investment (in t = 0) was set to α0 = 0.4, while the share of the relevant market was β0 = 0.2. To consider companies with more or less risky assets or with a smaller or larger stake in the underwriting market, we carried out a robustness test by varying these starting values from 0 to 1 and examining their influence on our findings. Figure 4 shows the results if α0 is varied from 0 to 1 for β0 = 0.2.

With regard to expected gain, the various strategies exhibit a robust relationship—a positive link between α0 and return, and this result is also found in respect to the ruin probability of the company. Figure 5 shows the results if β0 is varied from 0 to 1 for α0 = 0.4.

Regarding the expected gain per annum, the growth strategy turns out to be the best strategy, given a low market share, but not given a high market share. This is the first instance where the growth strategy has not produced the highest return. The main reason for this change is that, for higher market shares in the insurance market the equity capital of 15 million at is no longer adequate (i.e., the insurance company bears a higher investment and underwriting risk, but remains unchanged). As a consequence, management rules are more often triggered due to low equity capital levels. The result is that the growth strategy behaves very similarly to the solvency strategy, often reducing the values of and Note that for the growth strategy corresponds very closely to the solvency strategy because cannot be further increased. The growth strategy thus produces the same risk and return as the solvency strategy in all simulations unless is first decreased (for Trigger) and then again increased (because Trigger). In the context of management strategies, ruin probability is thus delimited for the growth strategy, but not for the high-risk strategy and no strategy. This makes the latter two strategies more risky, but also means that they are likely to deliver a higher absolute return level.

5.3.5. Variation of the consumer response factor

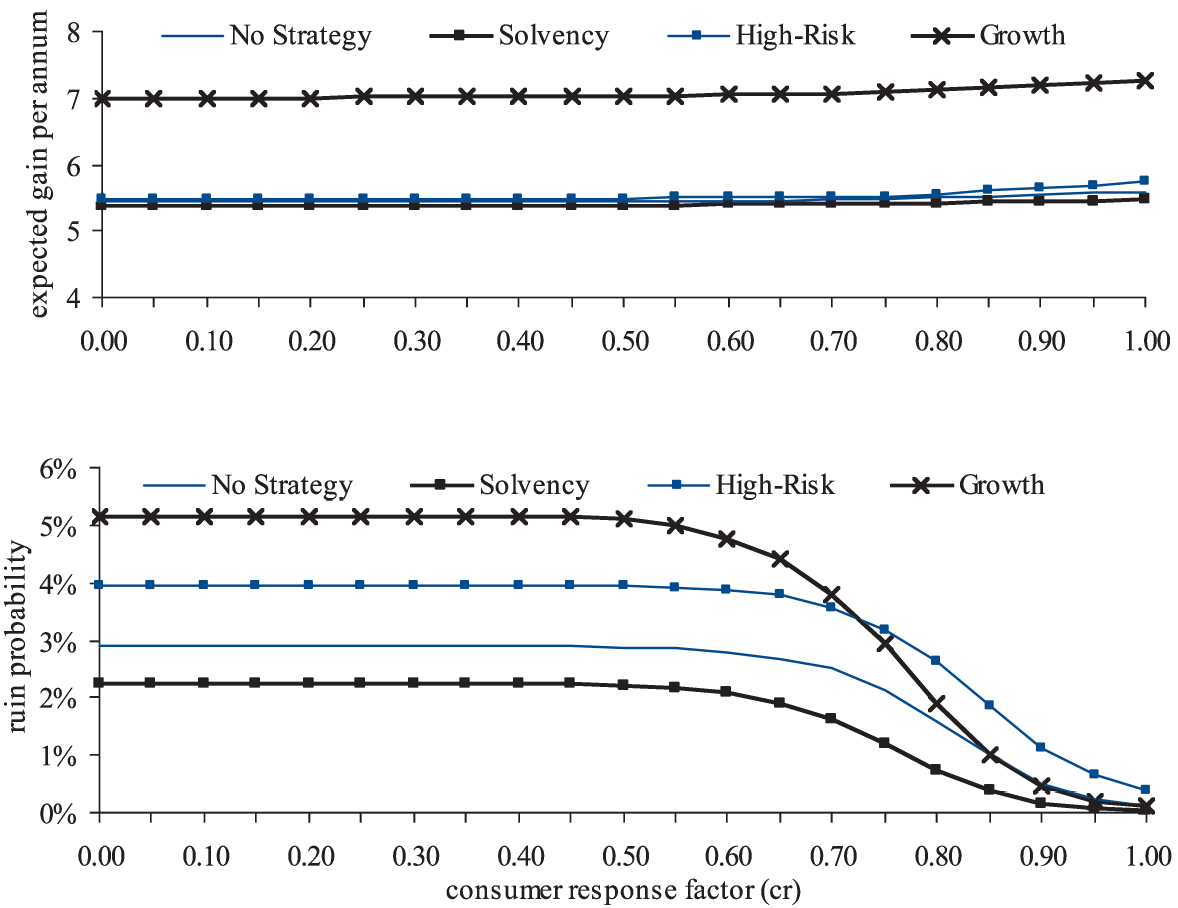

The consumer response factor determines the willingness to pay a certain premium for a defined amount of insurance. We implemented a reduction of the premium by the factor 0.95 for an insurance company in a distressed financial situation, but consumers may be expected to be reluctant to pay even this much, so the reduction in premium can be viewed as conservative (Wakker, Thaler, and Tversky 1997). Assuming that the insurance company is also willing to sell insurance coverage for premiums priced below its cost of expected claims, we examined the influence of consumer response factors ranging from 0 to 1 on our model results (see Figure 6).

In Figure 6, one can observe a small decline in the expected gain per annum with a decreasing consumer response factor, which illustrates the increasing negative effect of this factor. However, the influence of consumer response on ruin probability is far more interesting. The probability of ruin increases until a certain level, after which the value stays fixed. This phenomenon is explained by the fact that consumer response has a very strong influence on the next year’s performance due to reduced premiums. As a result, the insurance company goes bankrupt every single time the consumer response is triggered. This means that once consumers notice the company’s financial distress (i.e., Trigger), they all reduce premium payments to a large extent and management cannot avoid insolvency.

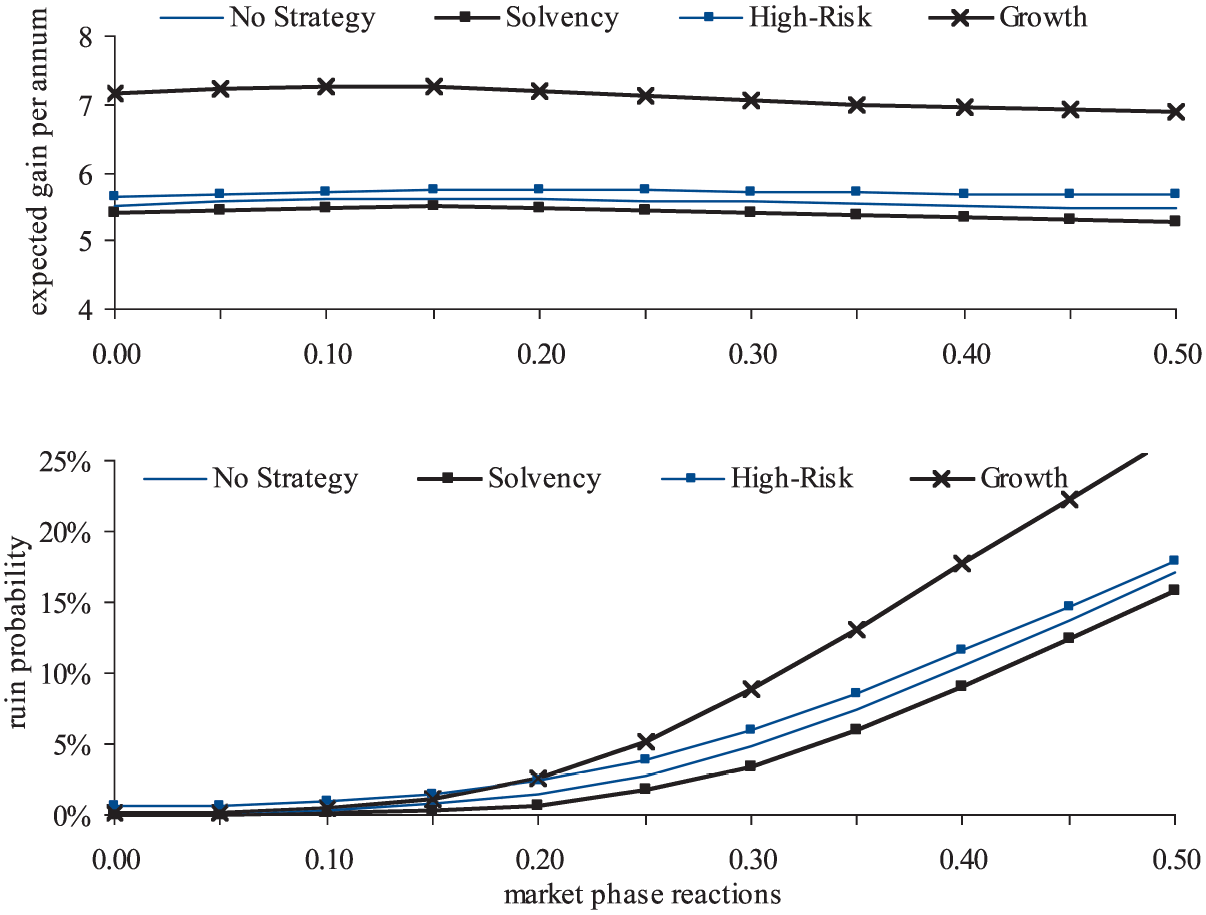

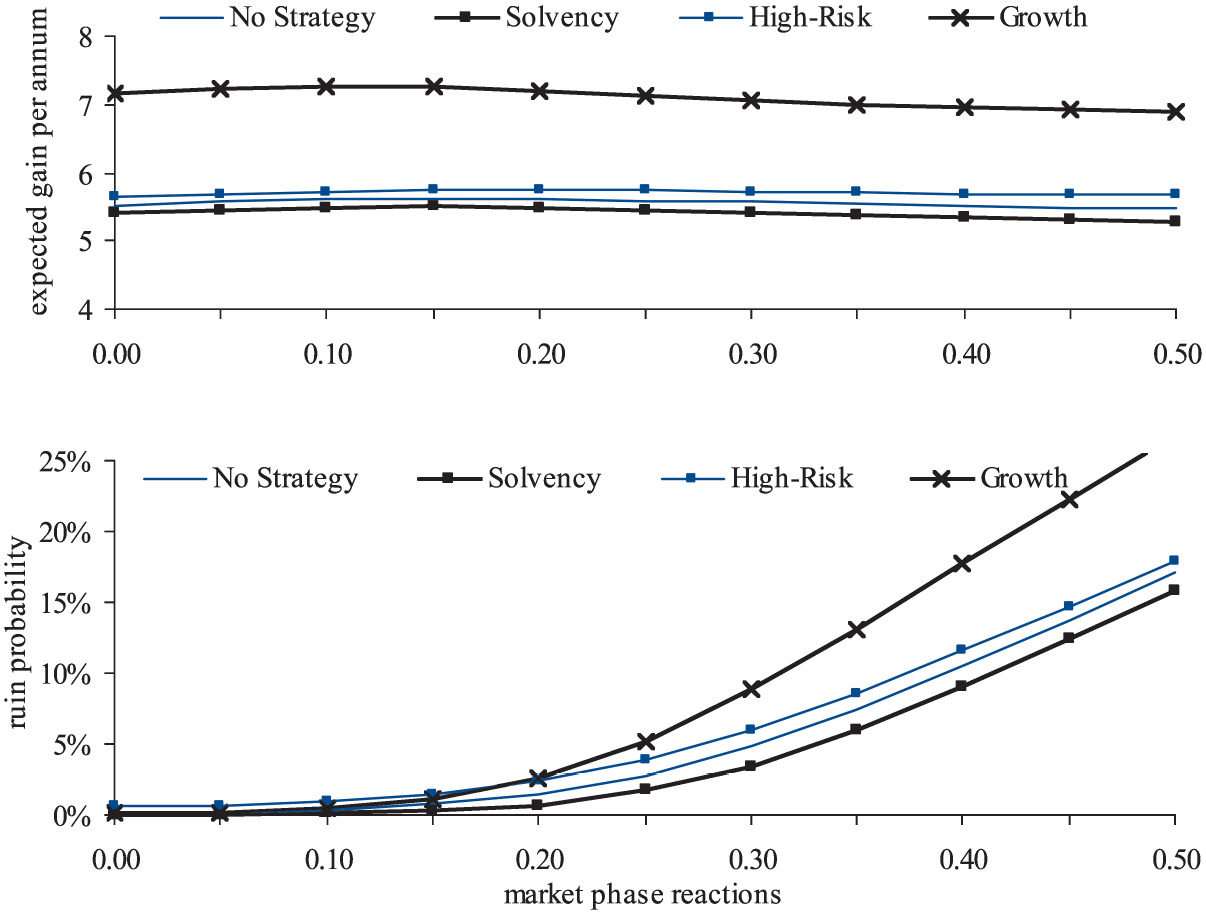

5.3.6. Variation of market phase reactions

Finally, we want to examine the influence of the market phase on our model. In the model assumptions set forth in Section 5.1, we assumed a reaction of 0.05, which corresponds to πs of 1.05 (0.95) for the advantageous (disadvantageous) market phase. To check the robustness of our results, we varied the market phase reactions for values ranging from πs up (down) to 1.5 (0.5). The results are shown in Figure 7.

Figure 7 illustrates that varying the market phase has only a small influence on the expected gain. However, there is a sharp increase in ruin probability in the case of more severe market reactions, which can be explained by the Increasing negative effects on premiums that occur in a disadvantageous market phase. Another interesting question in this context is the influence of the transition probabilities introduced in Equation (5.1). Robustness checks not presented here showed that the expected gain is improved and ruin probability is decreased when there is a higher probability of remaining in a good market phase and vice versa, which makes intuitive sense.

6. Conclusion

The aims of this paper were to implement management strategies in DFA and to analyze the effects of management strategies on the insurer’s risk and return position. We found that the solvency strategy—reducing the volatility of investments and underwriting business in times of a disadvantageous financial situation—is a reasonable strategy for managers desiring to protect the company from insolvency. Our numerical examples showed that the ruin probability can be effectively lessened by reducing volatility of investments and underwriting business. The growth strategy of combining the solvency strategy with a growth target is an interesting alternative for managers pursuing a higher return than offered by the solvency strategy and who are also willing to take higher risks.

The DFA model presented in this paper embraces only a fraction of the elements necessary to truly model an insurance company. Furthermore, we confined our analysis to a small range of possible management strategies. Nevertheless, the numerical examples illustrate the benefit of applying management rules in a DFA framework, especially for long-term planning. Thus, for further research we suggest implementing management rules in a more complex DFA environment. We also propose to search for optimal management strategies within our model framework and to compare the optimization results with our heuristic management rules and the underlying simulation results. Both of these research ideas will provide more insight into the effect of management strategies on the insurer’s risk and return.