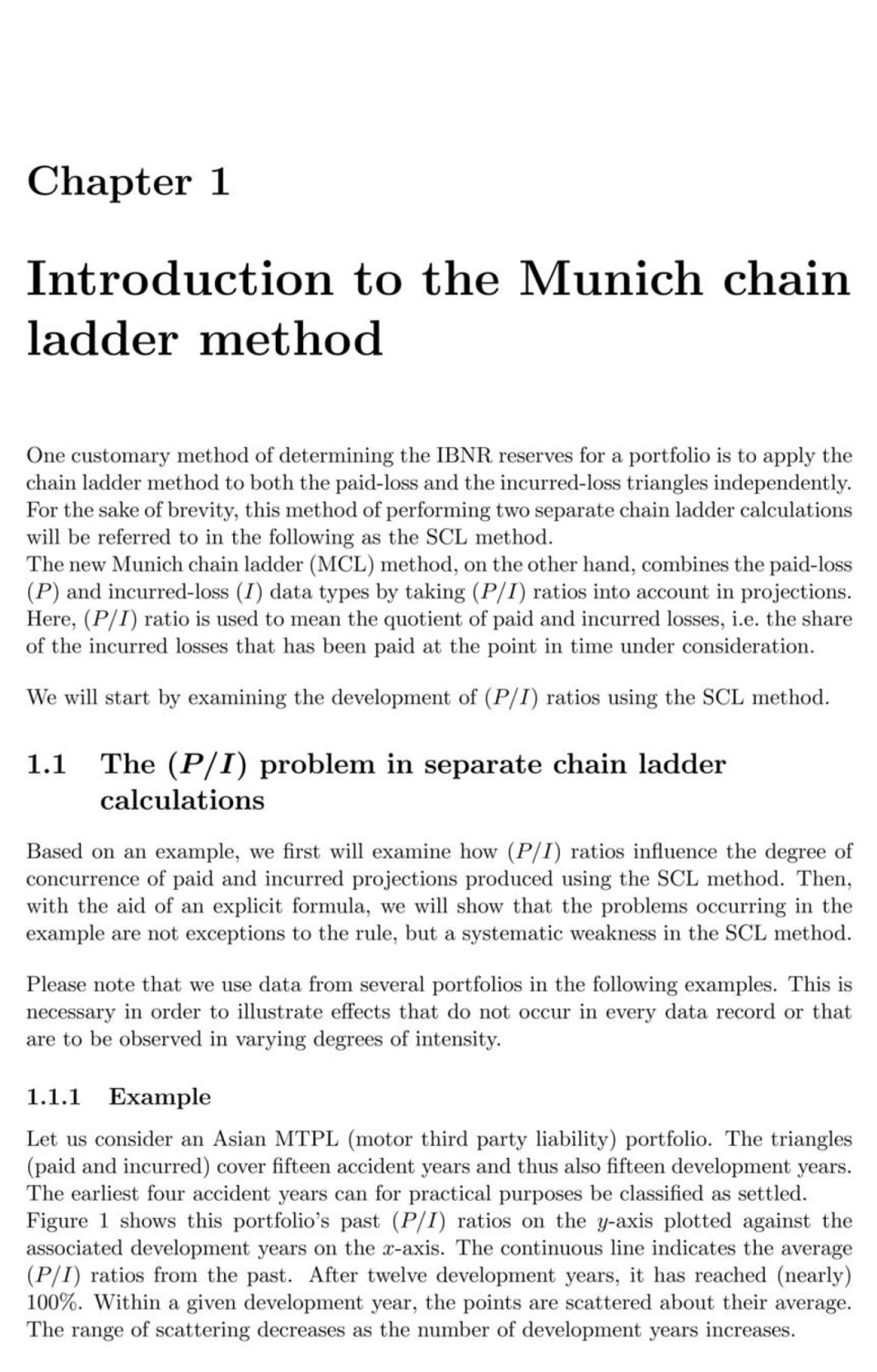

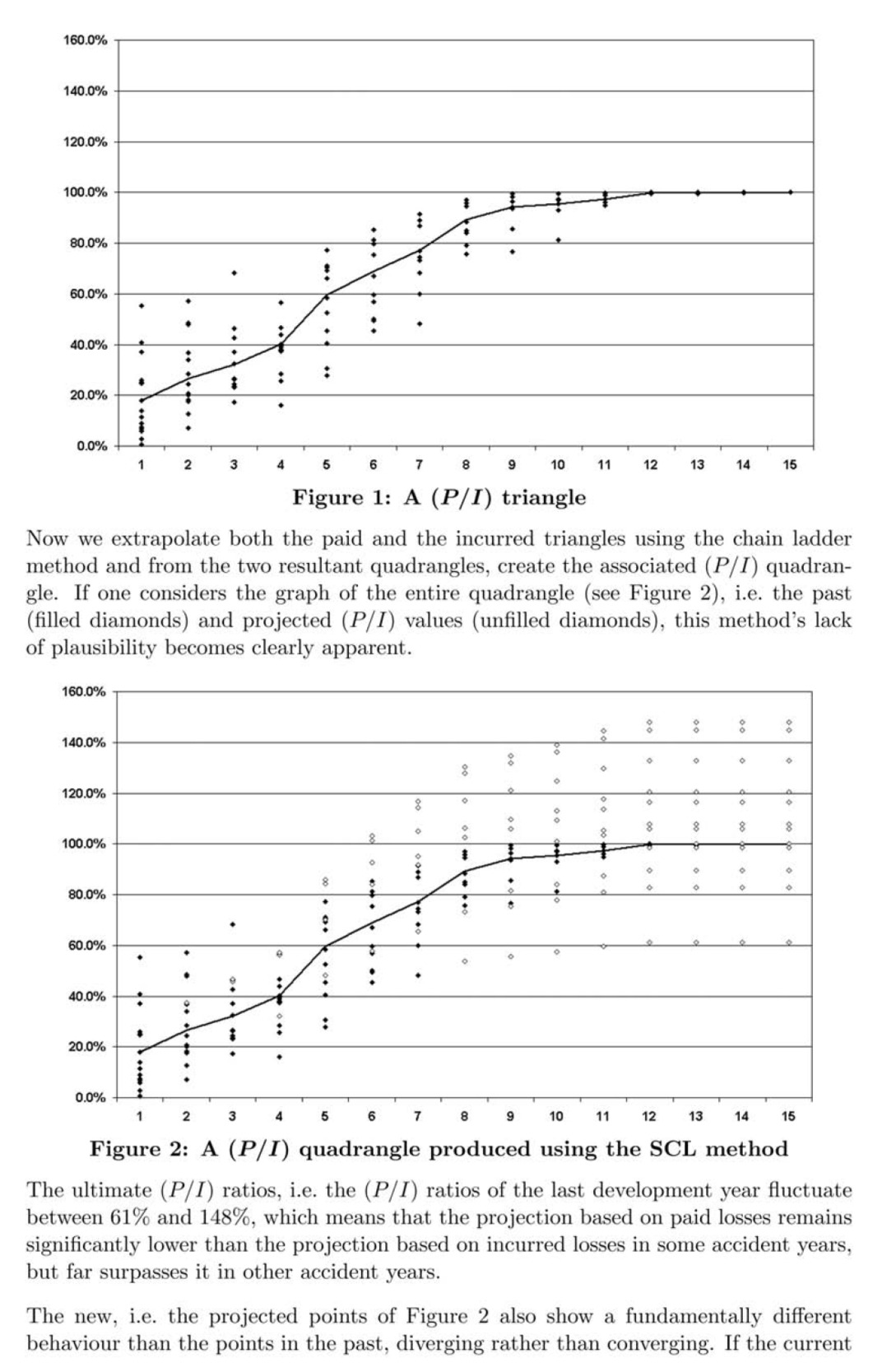

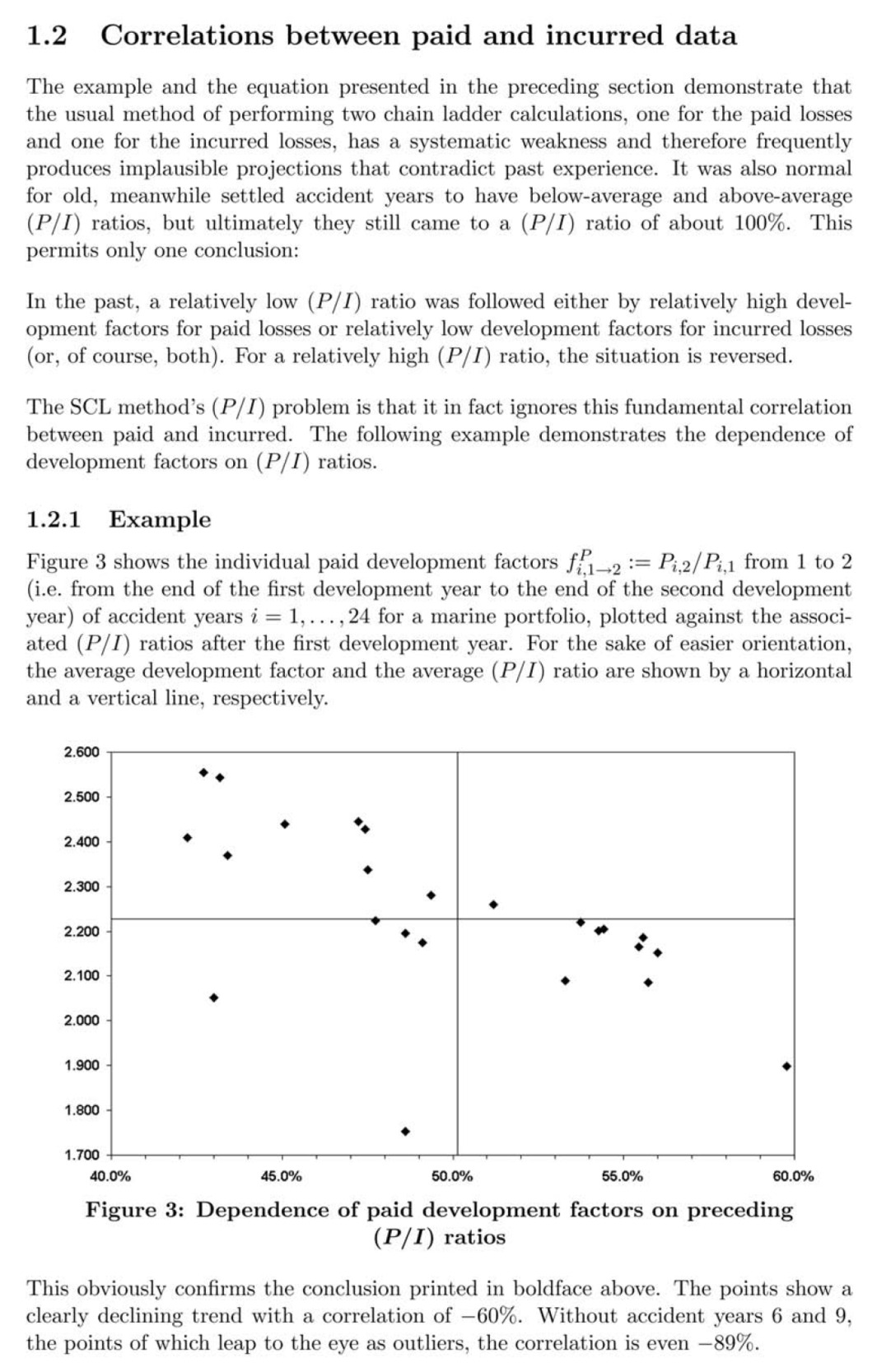

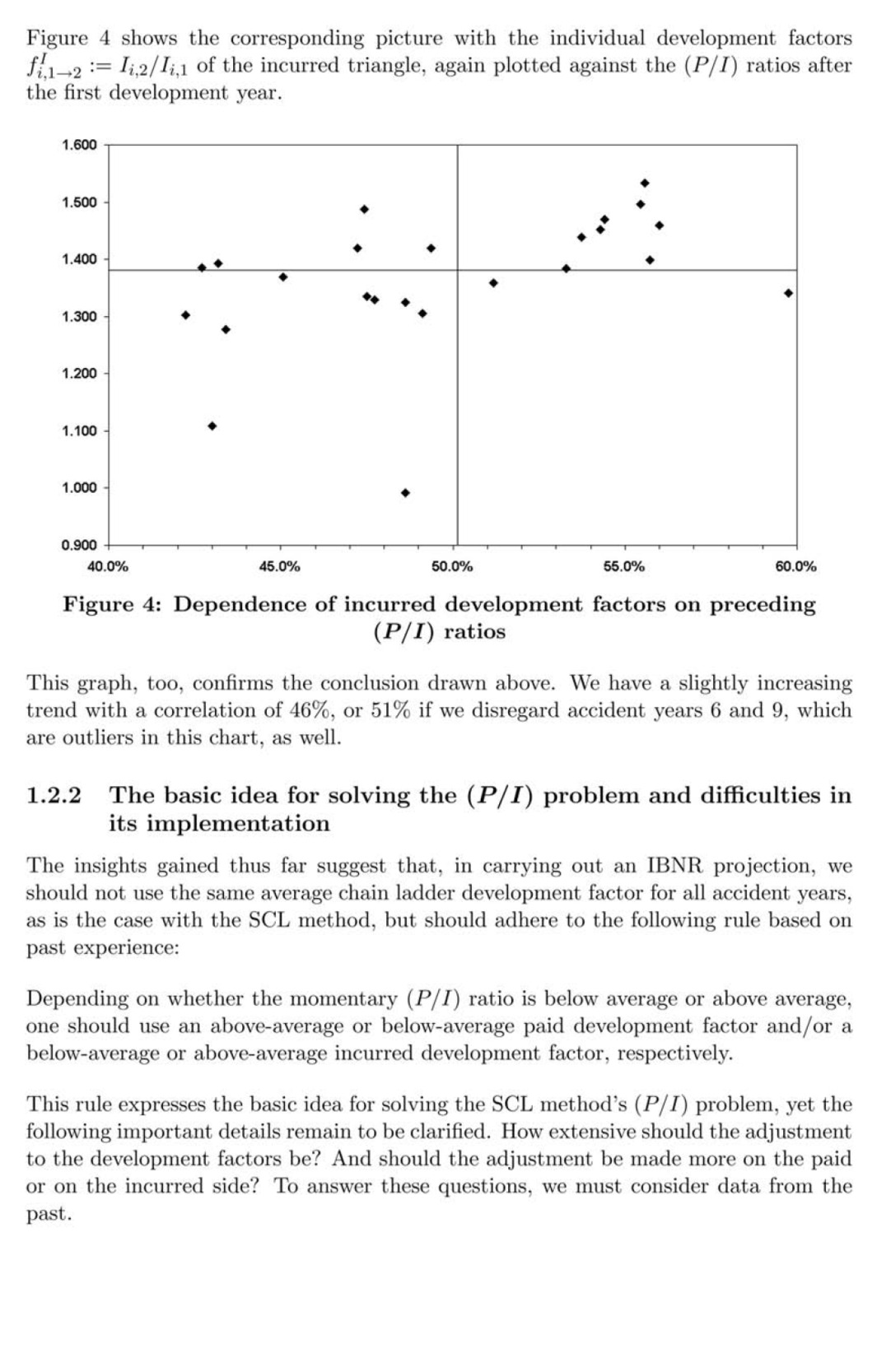

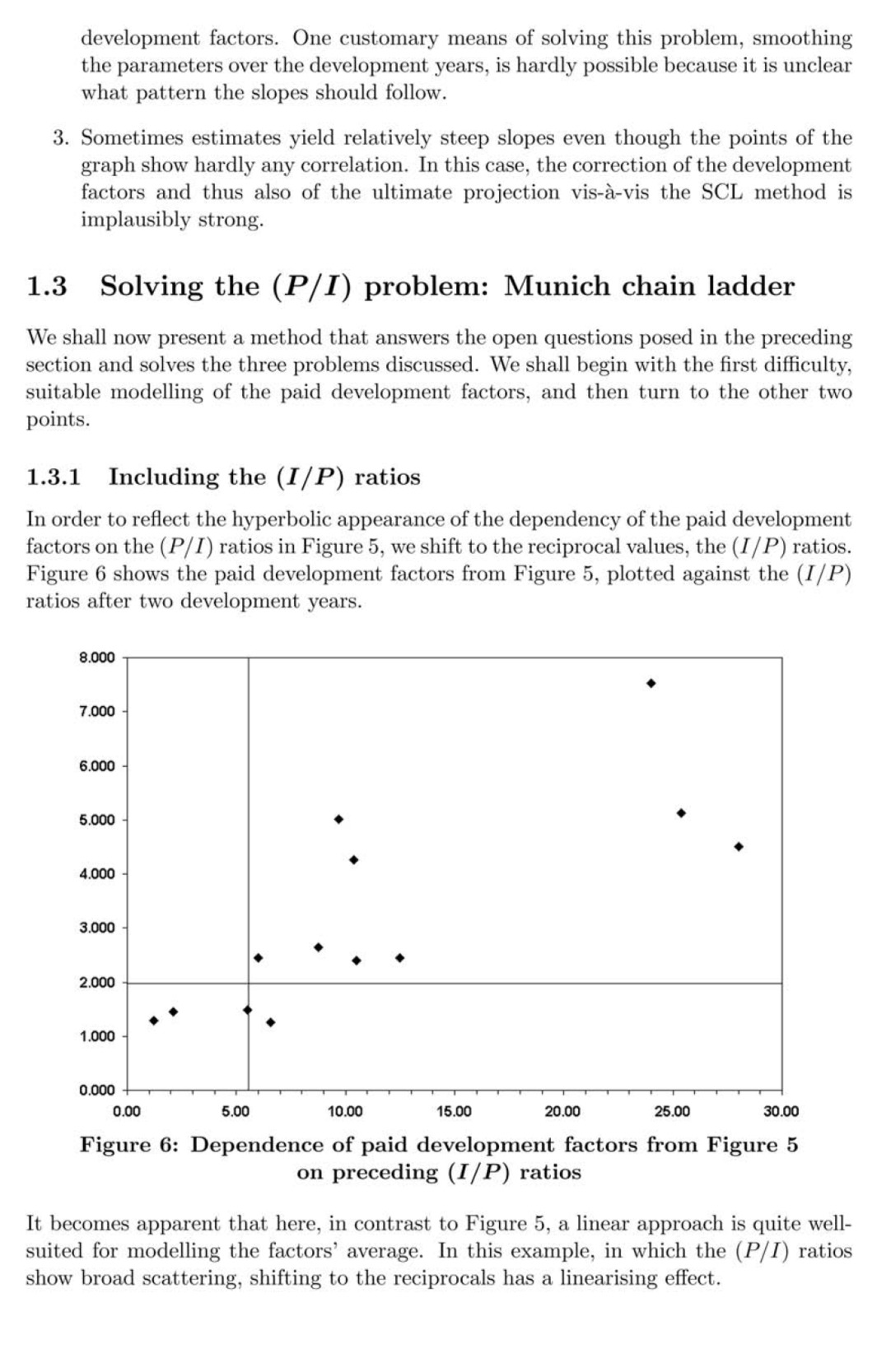

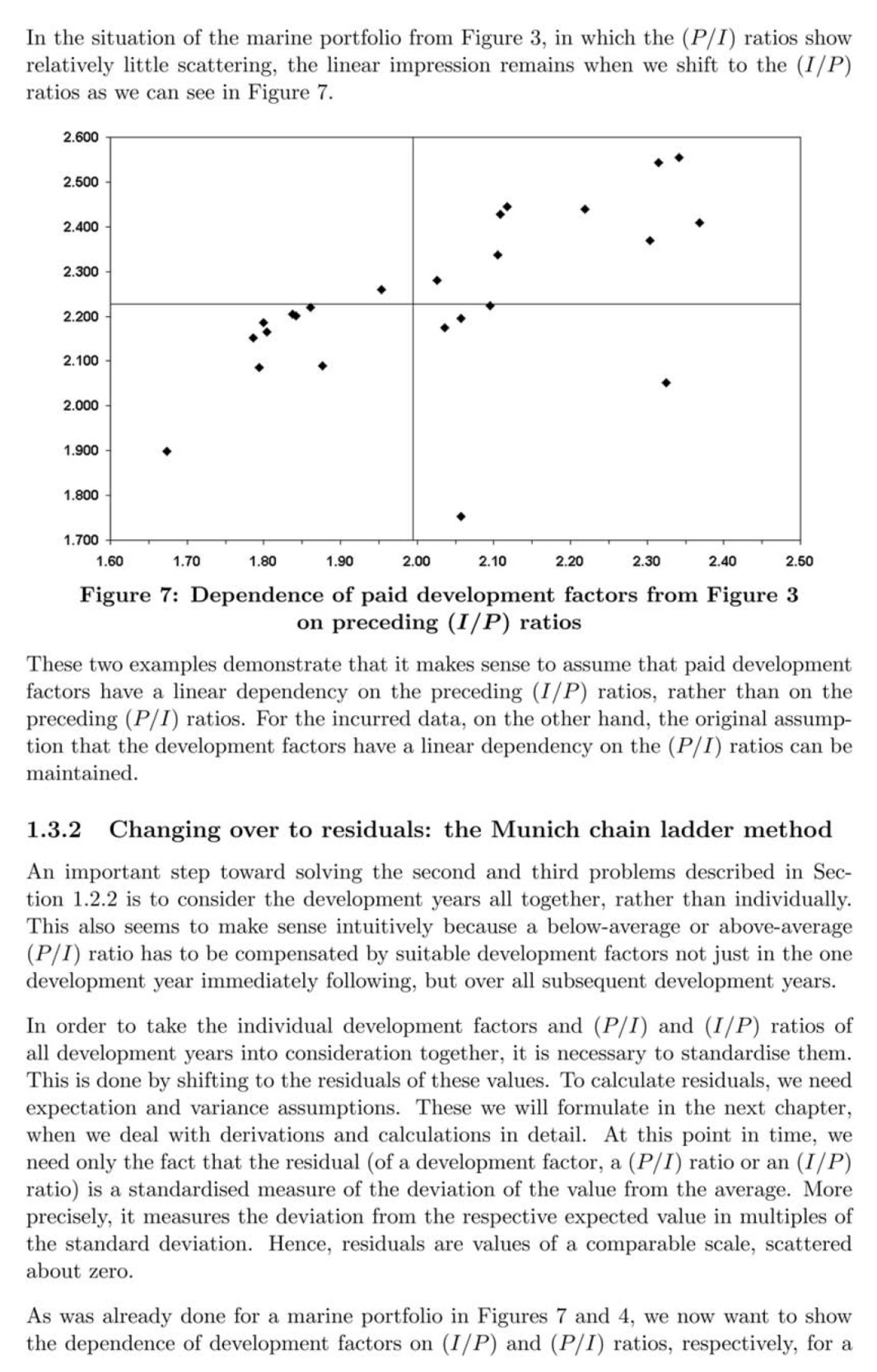

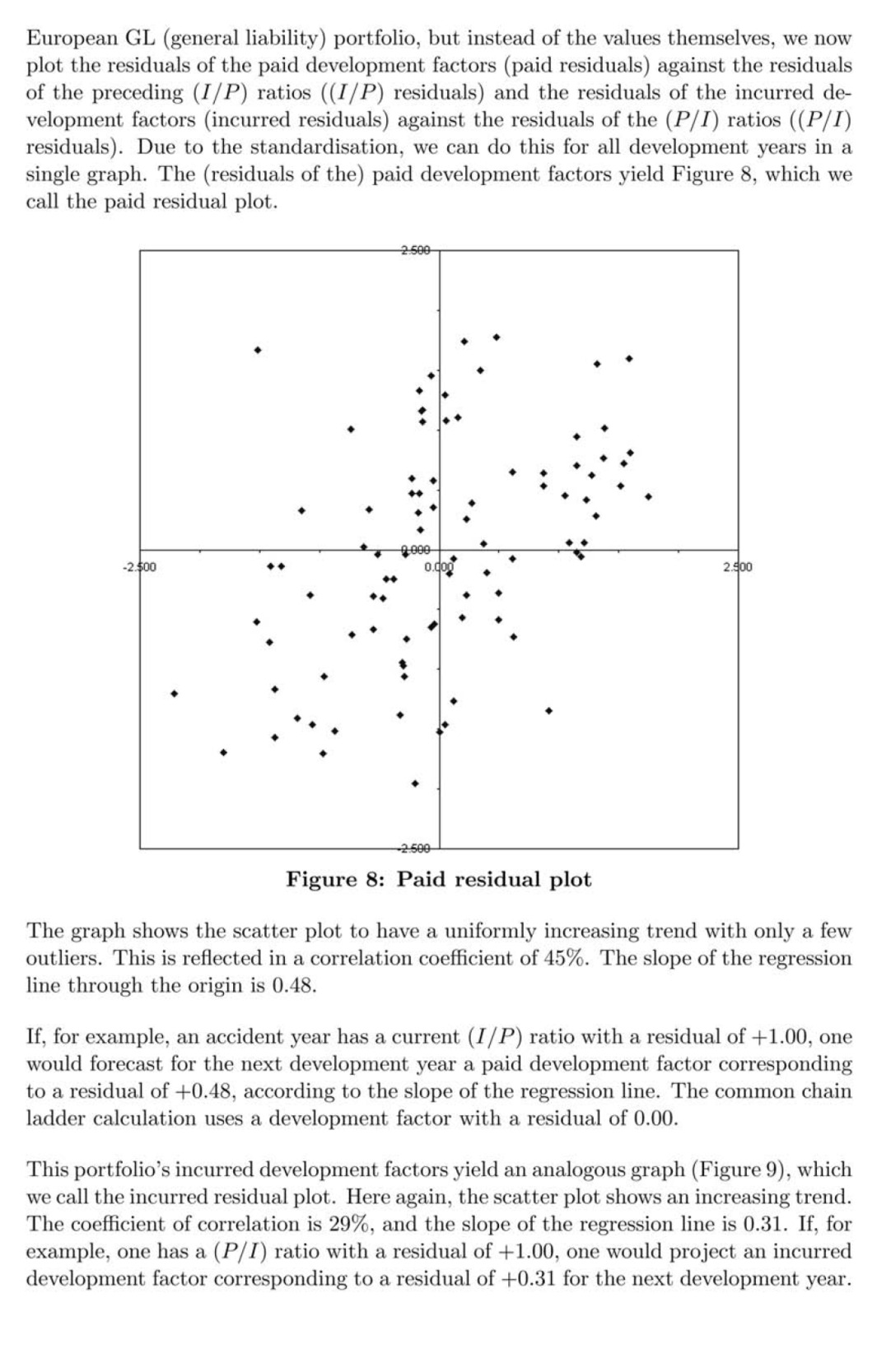

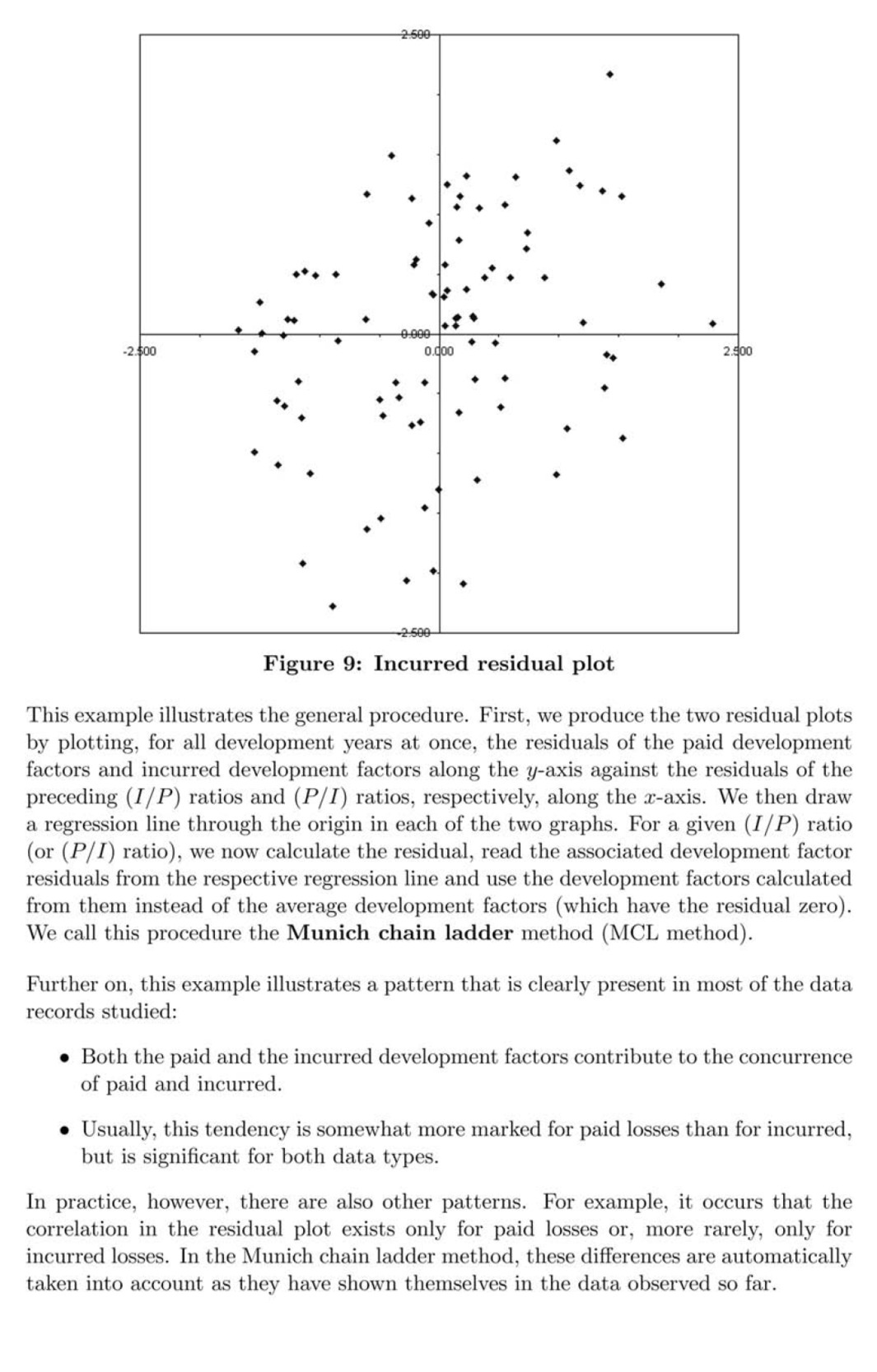

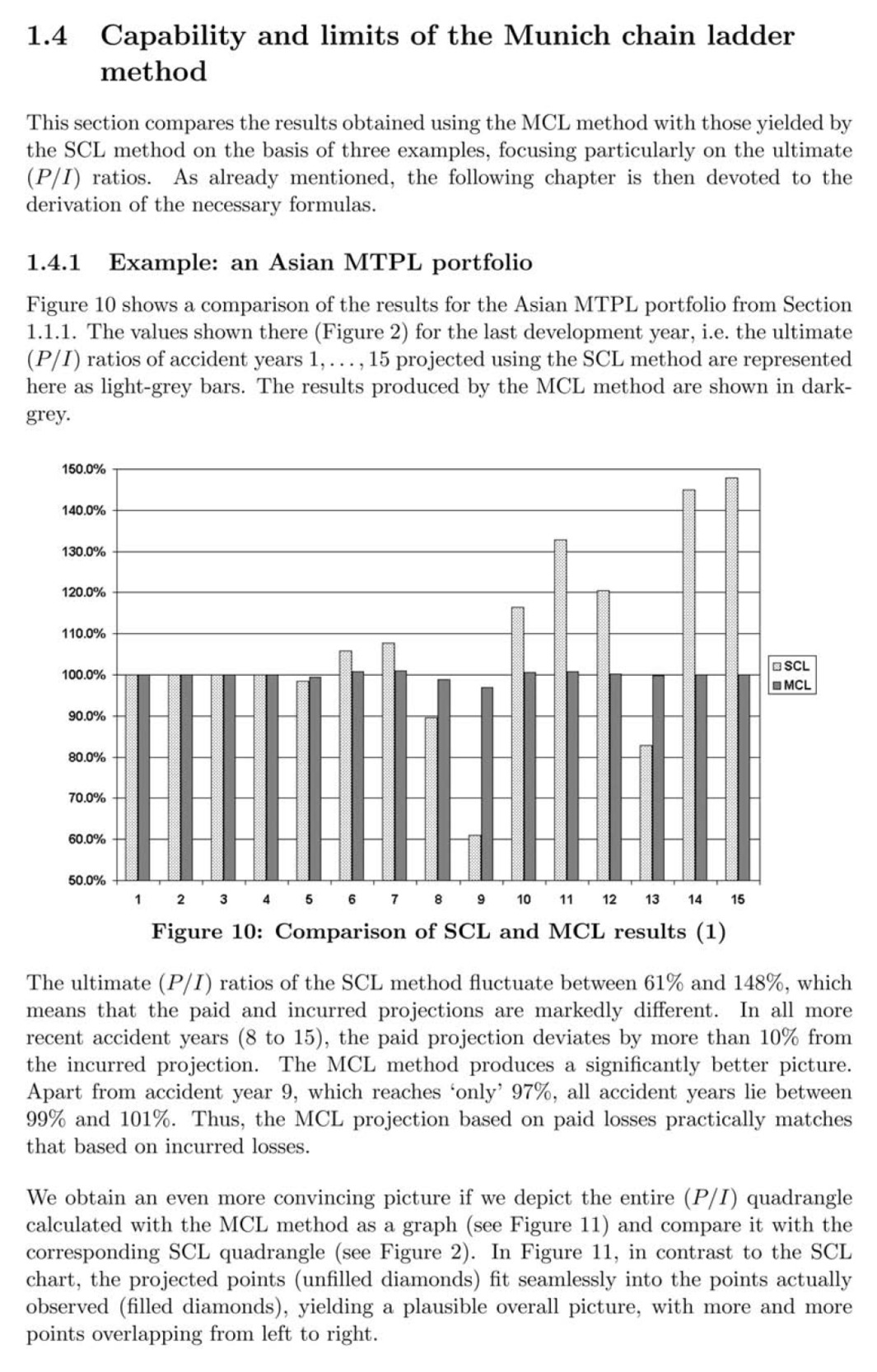

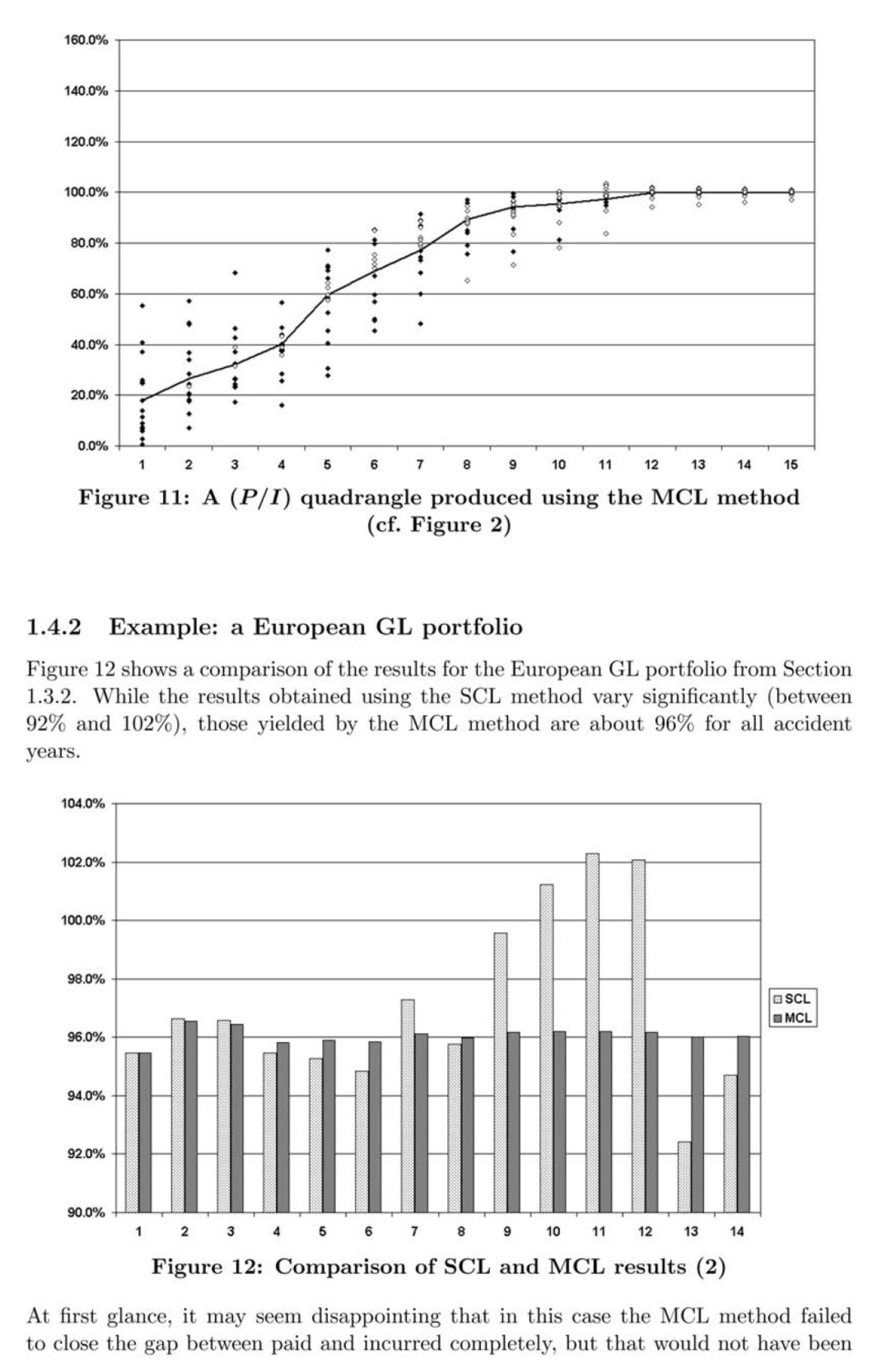

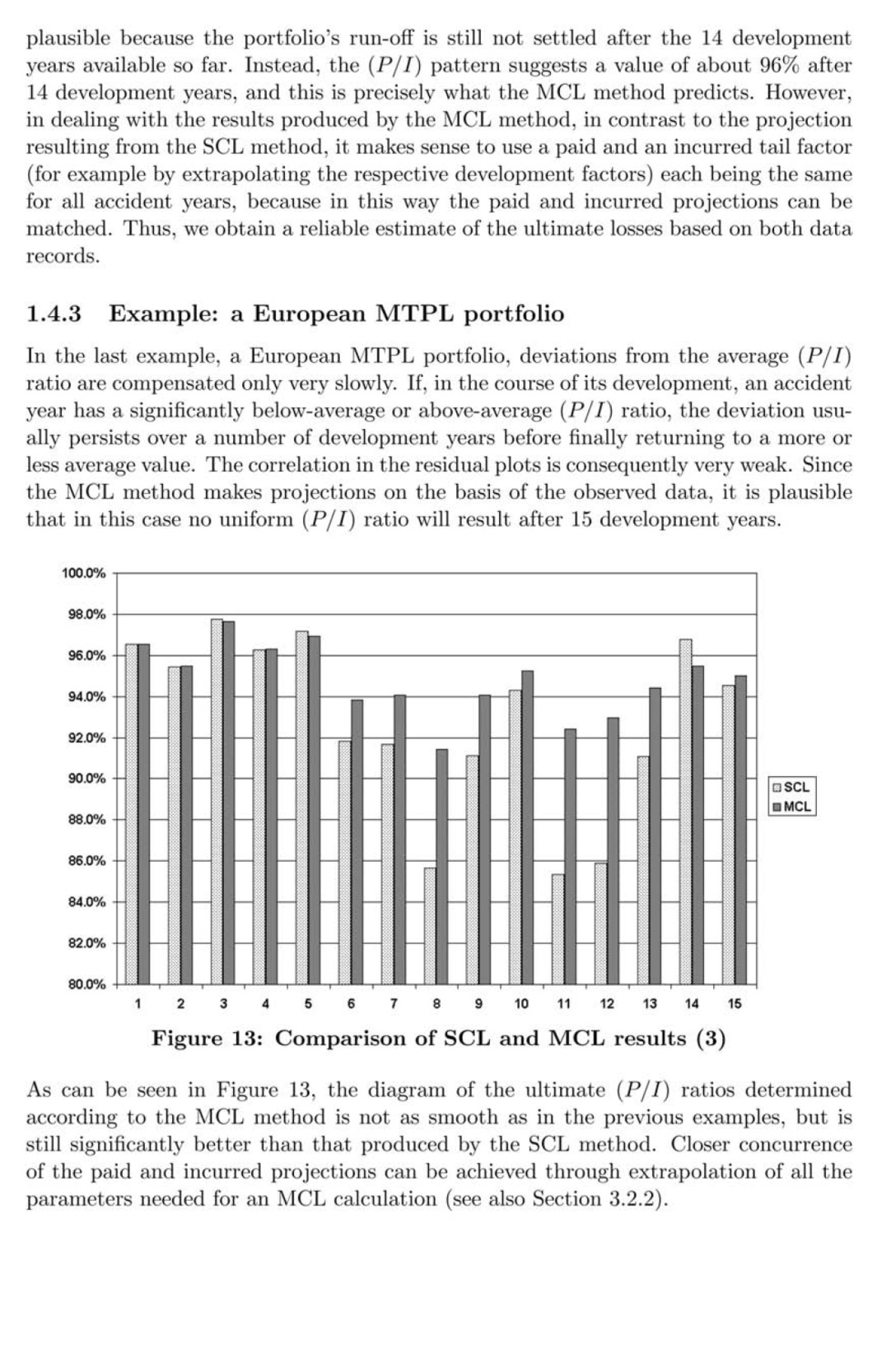

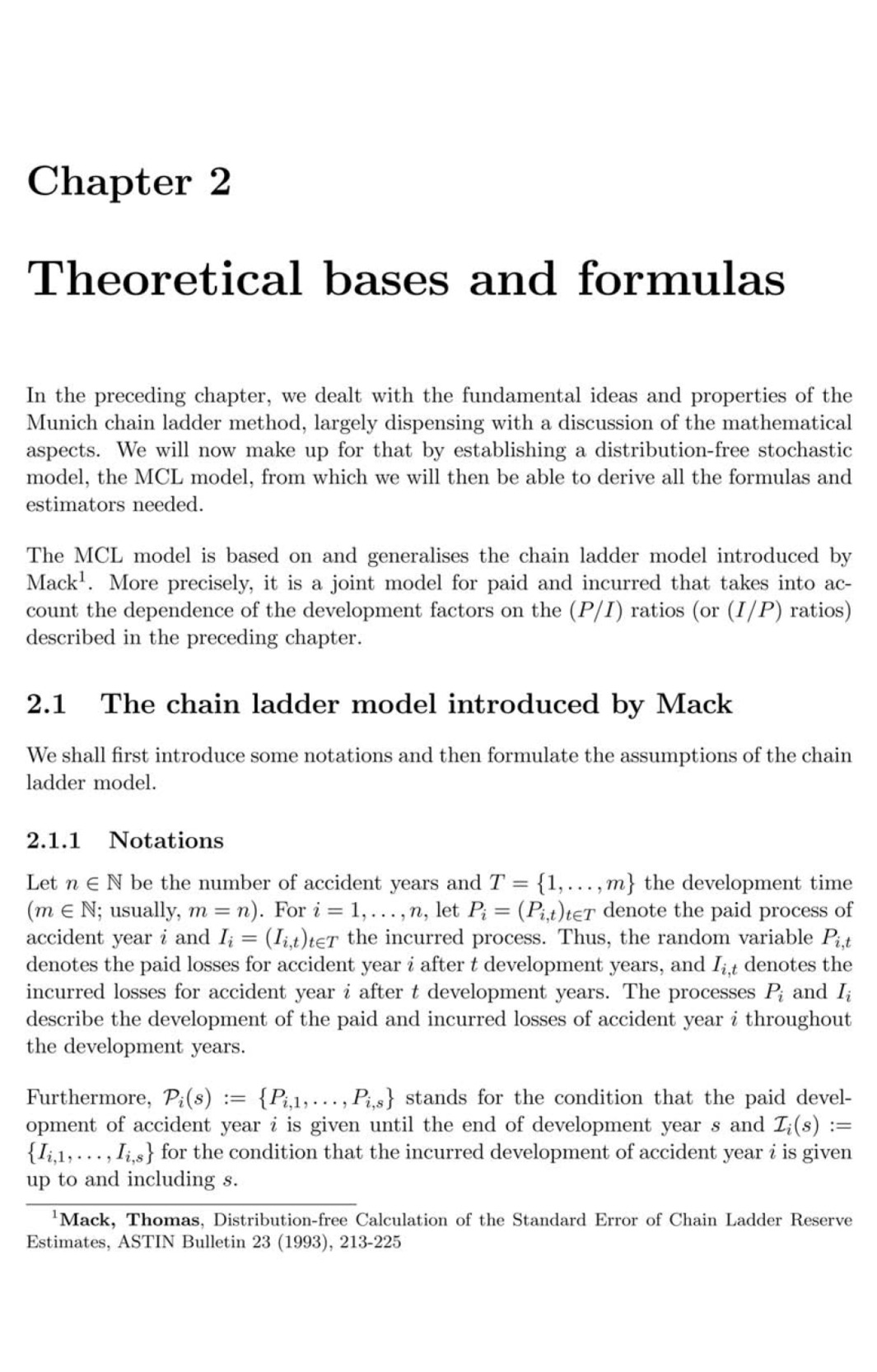

“Munich Chain Ladder” by Dr. Quarg and Dr. Mack is being reprinted in Variance to give this important paper wider visibility within the actuarial community. The editors of Variance invited the authors to submit their paper for republication because we believe that the techniques described in their work should be known to all actuaries doing reserve analysis. We also hope to stimulate further research in this area. This paper is reprinted from Blätter der Deutschen Gesellschaft für Versicherungsund Finanzmathematik, volume 26, number 4, 2004, pages 597–630. We thank the editors of that journal and the authors for allowing Variance to publish the paper.