1. Introduction

Many property-casualty insurance companies buy reinsurance protection to hedge their risk of sustaining unacceptably large losses. This act of hedging, however, gives rise to another type of risk: reinsurance credit risk. We describe reinsurance credit risk as the risk that an insurance company’s counterparty reinsurers will not fulfill their contractual obligations to indemnify the insurance company for its losses. Reinsurance credit risk deservedly influences many aspects of how an insurance company chooses to buy its reinsurance protection.

How should an insurance company measure, monitor, and manage its exposure to reinsurance credit risk? In particular, how should the company’s approach to reinsurance credit risk affect the company’s reinsurance purchasing decisions? First, I will describe certain common aspects of industry practice. The purpose of this description is not to provide a comprehensive inventory of all the complexities of current practice, for that task would be beyond the scope of this paper. Rather, the goal is to summarize with reasonable accuracy those salient aspects of common practice that could be improved with respect to reinsurance credit risk. After identifying some ways in which current practice can be improved, I will propose an alternative approach to reinsurance credit risk and describe the ways in which this alternative approach improves upon current methods.

2. Background

2.1. Common current practices for managing reinsurance credit risk

Current practice in the property-casualty insurance industry for buying reinsurance and for managing reinsurance credit risk is complex, multifaceted, and varies across individual companies. As a result, any broad summary of current practice is bound to be subject to caveats, limitations, and exceptions; I shall therefore describe certain general practices in the industry, with the understanding that there are many exceptions.

When an insurance company seeks to purchase reinsurance, it often seeks to evaluate the creditworthiness of the reinsurer counterparties with whom it might do business. This process often entails having an internal company credit risk committee that decides, based upon various credit risk factors, which reinsurer counterparties are “approved” for transacting reinsurance business; other reinsurers are labeled “not approved.” Then, internal compliance ensures that all reinsurance business transacts only with approved reinsurers. By prudently restricting the list of reinsurers with which it transacts business, the company attempts to contain reinsurance credit risk to an acceptably low level. Ultimately, “the ‘approved list of reinsurers’ at most primary insurers remains among the most important and inviolable guides for cedent underwriter behavior” (Conning Research and Consulting 2012, 65).

There are many variations on this theme of an approved list. For example, a company might have a separate approved list of reinsurers for short-tail business, such as property catastrophe business, and a different list of approved reinsurers for long-tail excess of loss casualty business. Or, a company might have several categories, such as “approved,” “not approved,” and “it depends.” In general, these variations do not materially affect our discussion.

In addition to evaluating reinsurers based on general creditworthiness, companies also typically monitor their accumulated amount of credit risk exposure to any individual approved reinsurer. If a property-casualty insurance company accumulates, through various reinsurance agreements, a significant amount of exposure to a particular reinsurer, this exposure may encroach upon a previously defined risk limit set by the company. As a result, the company may choose to disfavor or even bar the particular reinsurer from further transacting business with it, even if the reinsurer would otherwise be creditworthy.

Finally, companies manage reinsurance credit risk by sometimes requiring counterparty reinsurers to “collateralize.” The reinsurer can post collateral for the full amount of the reinsurance limit, but typically, rather than actually posting collateral, the reinsurer will pay for a letter of credit (LOC) from its bank, which serves as a guarantee that the reinsurer will pay its obligations. Historically, companies have required collateralization for reinsurance recoverables from foreign (“alien”) reinsurers. This practice was related to statutory accounting of the reinsurance recoverables rather than a specific determination related to credit risk management, and recent reforms are transforming this area of practice. In general, the recent reforms seem likely to make the use of collateral in these situations much less prevalent than in prior decades. Meanwhile, in most other situations that do not involve a foreign reinsurer, primary companies typically require reinsurers to collateralize only when there appears to be a significantly greater credit risk than usual.[1] Therefore, despite the occasional use of collateral to reduce credit risk, in many situations collateral is not used and reinsurance credit risk remains.

2.2. Drawbacks of current practices for managing reinsurance credit risk

Given the complex process of buying reinsurance and given the variation of practices across companies, are there any general observations one can make about these common practices for handling reinsurance credit risk? I believe that one can identify three disadvantages of common practice.

-

Divergence in time. The credit risk committee decides about reinsurers’ creditworthiness first; afterwards, the business unit seeking to buy reinsurance, together with the ceded re department and reinsurance broker, solicits reinsurance quotes, often from only the approved reinsurers. As a caveat, there can be exceptions in which the process comes full circle: after receiving the first round of reinsurance quotes, the credit committee is asked to reconsider certain reinsurers for approval. Nevertheless, often the process of purchasing reinsurance displays a crucial inter-temporal problem: the evaluation of reinsurers’ credit risk occurs prior to and separately from the evaluation of the reinsurance transaction price.

-

Divergence in personnel. Credit risk analysis requires special expertise; consequently, the credit risk committee deciding whether or not to approve a reinsurer is often not the same group of executives who are running the business unit that is purchasing reinsurance. Again, while there are caveats to this characterization, all too often this divergence in personnel is real; sometimes, it can lead to a divergence in interests and can result in a fragmentation between evaluating reinsurers’ credit risk and evaluating the reinsurance transaction price.

-

Divergence in metric. The business unit buying reinsurance evaluates quotes for a given reinsurance cover based on dollar cost, whereas the credit risk committee’s evaluation of reinsurers’ creditworthiness mostly uses different metrics. For example, the credit risk committee might assign, for a certain reinsurer for a particular segment of business, a categorical metric such as approved versus not approved. While some committees might use more refined categories, and some might even go so far as assigning individual creditworthiness rankings to individual reinsurers, these more granular evaluations of credit risk still do not seamlessly translate into a dollar cost metric to assign to each reinsurer. Again, the result is that the evaluation of reinsurer’s credit risk and the evaluation of the reinsurance transaction price are not easily integrated.

The crucial theme shared by all of these aspects of common practice is that the company typically does not have a systematic quantitative framework for evaluating the trade-off between reinsurance credit risk and reinsurance transaction price, which leads to several undesirable consequences.

First, the company cannot properly evaluate the trade-off in price between two approved reinsurers of greater and lesser financial strength. As a result, the company lessens the price incentive for it to prefer a stronger approved reinsurer to a weaker approved reinsurer or, alternatively, to extract price concessions from the weaker approved reinsurer.

Second, the company cannot properly evaluate the proposition of getting a better price from a reinsurer of lesser financial strength that might otherwise be an unapproved reinsurer. If the credit risk is worse but the price is better, is the trade-off worth it? In general, current practices do not provide a suitable framework for resolving this question.

Third, using accumulation limits on exposure also fails to present a trade-off between risk and reward. Given that the company has a concentrated exposure to a certain reinsurer, placing more business with that reinsurer is undesirable and risky. But if that reinsurer is offering the best price, is it worth taking additional risk exposure to this particular reinsurer if doing so can generate a significant financial benefit for the company? Again, common practices do not provide a suitable framework for resolving this question.

Fourth, current practices do not provide a suitable framework to evaluate the trade-off between traditional reinsurance products and alternative “zero credit risk” reinsurance products, such as cat bonds and collateralized reinsurance. If a cat bond has lower credit risk than traditional reinsurance but also costs more, does the cat bond’s lower credit risk justify the higher cost or not?

3. A proposed alternative approach to managing reinsurance credit risk

In order to improve upon these aspects of common practice, I propose a framework that enables one to translate reinsurance credit risk into a “cost of risk” that can be quantified and assigned to any given reinsurer. Under this paradigm, one embraces the probabilistic perspective that all reinsurers, no matter how creditworthy they are, manifest some amount of credit risk; the difference among reinsurers is simply the quantum of risk, which in general will vary based upon the likelihood of default for a particular reinsurer. Or, similarly, one can say that the difference among reinsurers is simply the different cost of hedging each reinsurer’s credit default risk. Fortunately, market instruments such as credit default swaps (CDS) can provide market-based pricing information about the cost of hedging the credit risk of various (though not all) reinsurers.[2] By harnessing this information, one can establish a common basis for evaluating reinsurers’ price quotes on an “apples-to-apples” basis. As a result, one can evaluate the trade-off between the higher prices charged by reinsurers of higher credit quality and the lower prices charged by reinsurers of lesser credit quality.

In order to deploy this proposed methodology, one needs to establish a common metric for comparing the cost of various reinsurers’ price quotes. Thus we define:

Credit risk adjusted reinsurance price =reinsurance price+cost of credit risk

Using a market-consistent paradigm, we rewrite Equation 3.1 as follows:

Credit risk adjusted reinsurance price =reinsurance price+cost of credit default protection.

Equations (3.1) and (3.2) highlight that the total economic cost to the buyer of reinsurance is the cost of the reinsurance cover’s price and also the cost of buying credit protection on the counterparty reinsurer; as a result, price quotes and firm order terms should be evaluated on the basis of this total cost rather than simply the nominal reinsurance price.

In order to more fully describe the proposed approach, we now show examples via simplified case studies.[3]

3.1. Simplified case study 1: Evaluating reinsurance quotes by using CDS price information

In this case study we deal with an insurance company seeking to buy property catastrophe reinsurance. The company solicits price quotes from reinsurers with varying degrees of creditworthiness.

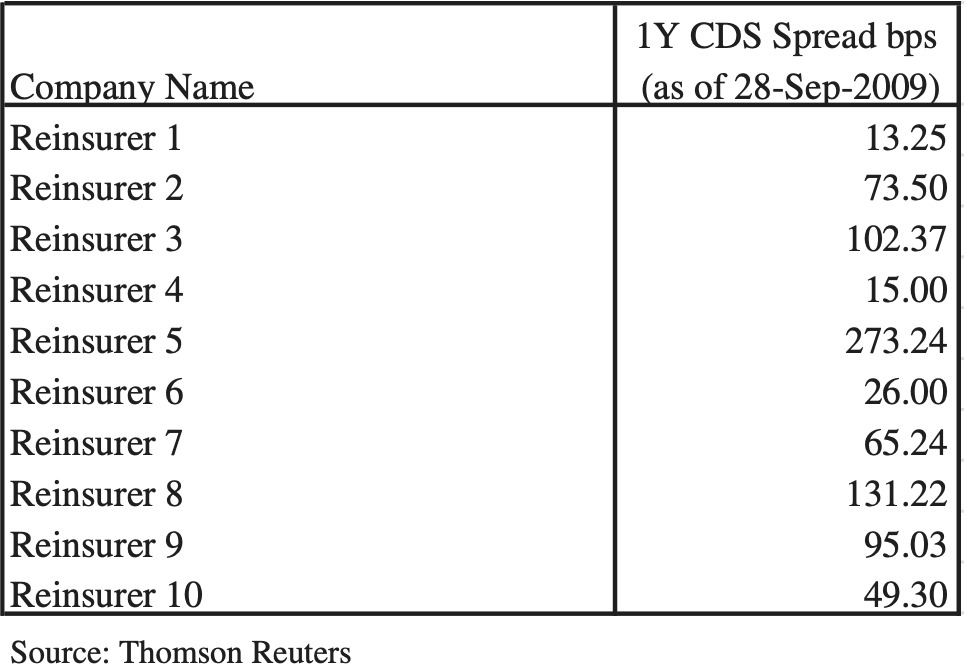

Exhibit 1 shows CDS price data for selected reinsurers via the Thomson Reuters “TRX P Reinsurance Index” as of September 28, 2009.

First we will examine a simplified case in which only two reinsurers of varying creditworthiness offer price quotes. Let’s assume, for illustrative purposes, that Reinsurer 1 quotes a price of 6.0% Rate on Line (RoL), where Rate on Line equals price divided by limit; Reinsurer 8 quotes a price of 5.5% RoL. Let’s assume that each reinsurer is an “approved reinsurer” for the buyer and each reinsurer is willing to write 100% of the reinsurance cover. Now initially it appears that Reinsurer 8’s quote is lower and thus a better choice for the buyer. Incorporating the cost of credit risk, however, illuminates that Reinsurer 1’s quote is actually the lower price, as shown in Exhibit 2.

Exhibit 2 shows an example in which a higher quote from a more creditworthy reinsurer turns out to be the lower cost choice. It also shows how this type of measurement framework provides an incentive for reinsurers to enhance their financial strength. Moreover, this approach could provide a primary company with powerful information to show to a reinsurer of lesser credit quality (as judged by the CDS market) in order to extract a lower price. In this case, the buyer of reinsurance can say to Reinsurer 8 that its price quote needs to be reduced by $700,000 because otherwise it would effectively be the higher priced option.

3.2. Simplified case study 2: Transcending the “approved” list

In this case study, we will examine a situation which shows how using CDS information can help a company optimize its purchase by transcending the limitations of a restrictive “approved reinsurers list.” Exhibit 3 shows a list of reinsurers and, simply for the illustrative purposes of this case study, their status as approved or not approved.

Exhibit 4 shows a hypothetical case in which each of the reinsurers quotes a price for the cover and is willing to accept 50% of the exposure of the cover.

If the primary company buying the reinsurance cover uses restrictive categories such as approved and not approved, then in this case the company will unnecessarily pay more for its reinsurance cover. This result occurs because the low price from Reinsurer 8, which is not an approved reinsurer, is nugatory; therefore the market clearing RoL to place 100% of the cover is 8.65% (on an adjusted basis). But if the primary company buying the cover embraces the framework proposed in this paper, then Reinsurer 8’s quote could be considered for participation in the reinsurance program; then the market clearing price for 100% placement would be 7.95% (on an adjusted basis), resulting in cost savings for the buyer. In this case, the company that insists on restricting reinsurers to an approved list would squander several hundred thousand dollars on just this single transaction.

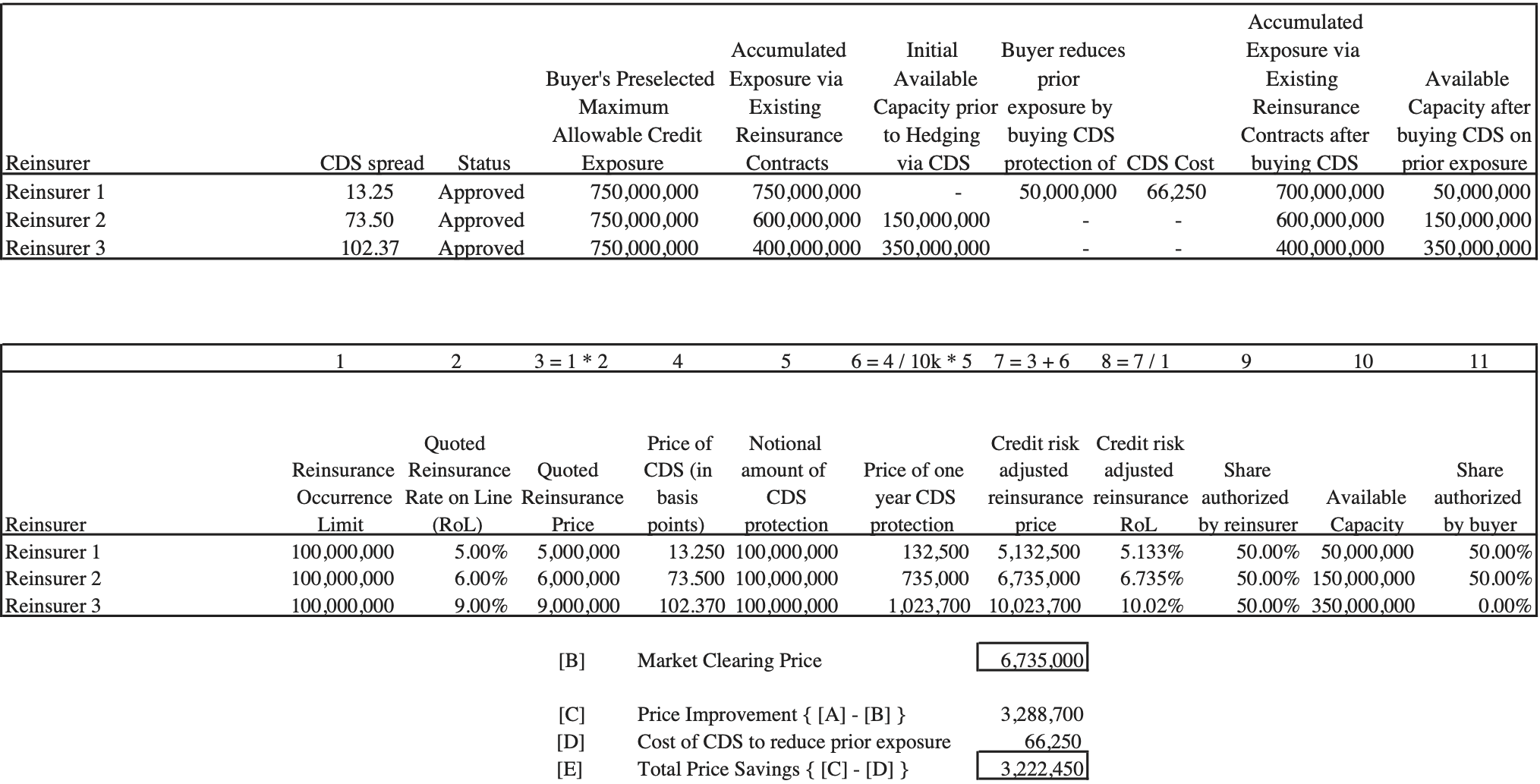

3.3. Simplified case study 3: Transcending “reinsurance exposure limits”

While the prior case study described a situation in which a reinsurer is approved or not approved, a similar situation can occur when a reinsurer is approved but is bumping up against the company’s maximum exposure limits. In such a situation, a primary company finds that one of its approved reinsurers has taken on a certain amount of the primary company’s reinsurance exposure; the primary company is not willing to concentrate any additional exposure with this single reinsurer. Now what happens if the primary company is now seeking to buy reinsurance cover and this particular reinsurer provides the most favorable quote? The current approach to reinsurance credit risk would require the buyer to disqualify the reinsurer from the bidding and thus ignore its quote, leading to a higher price. Or, the primary company could try to enter into a commutation agreement to finalize any outstanding exposure from prior contracts; this action reduces the total exposure concentrated with the reinsurer, thus allowing the reinsurer to once again qualify as “approved” for providing the prospective reinsurance. This approach, too, extracts a price from the buyer by forcing it to close out the prior reinsurance contracts for a fixed amount before all the risk has ebbed, possibly for a lower payment than deserved. In contrast, the proposed paradigm for managing reinsurance credit risk would take a wholly different approach. If the primary insurance company feels that its credit exposure to a particular reinsurer is beginning to exceed a comfort level, it now has a new solution: reduce the existing credit exposure by hedging the risk via CDS, thus allowing the reinsurer to quote and participate on the new prospective reinsurance cover. Here we emphasize that the goal of hedging in this case is not simply to reduce risk per se, but rather to optimize risk: by hedging the current concentration of exposure, the primary company can potentially buy new cover from this low priced reinsurer, leading to savings on the reinsurance purchase. Exhibits 5a and 5b compare the approaches.

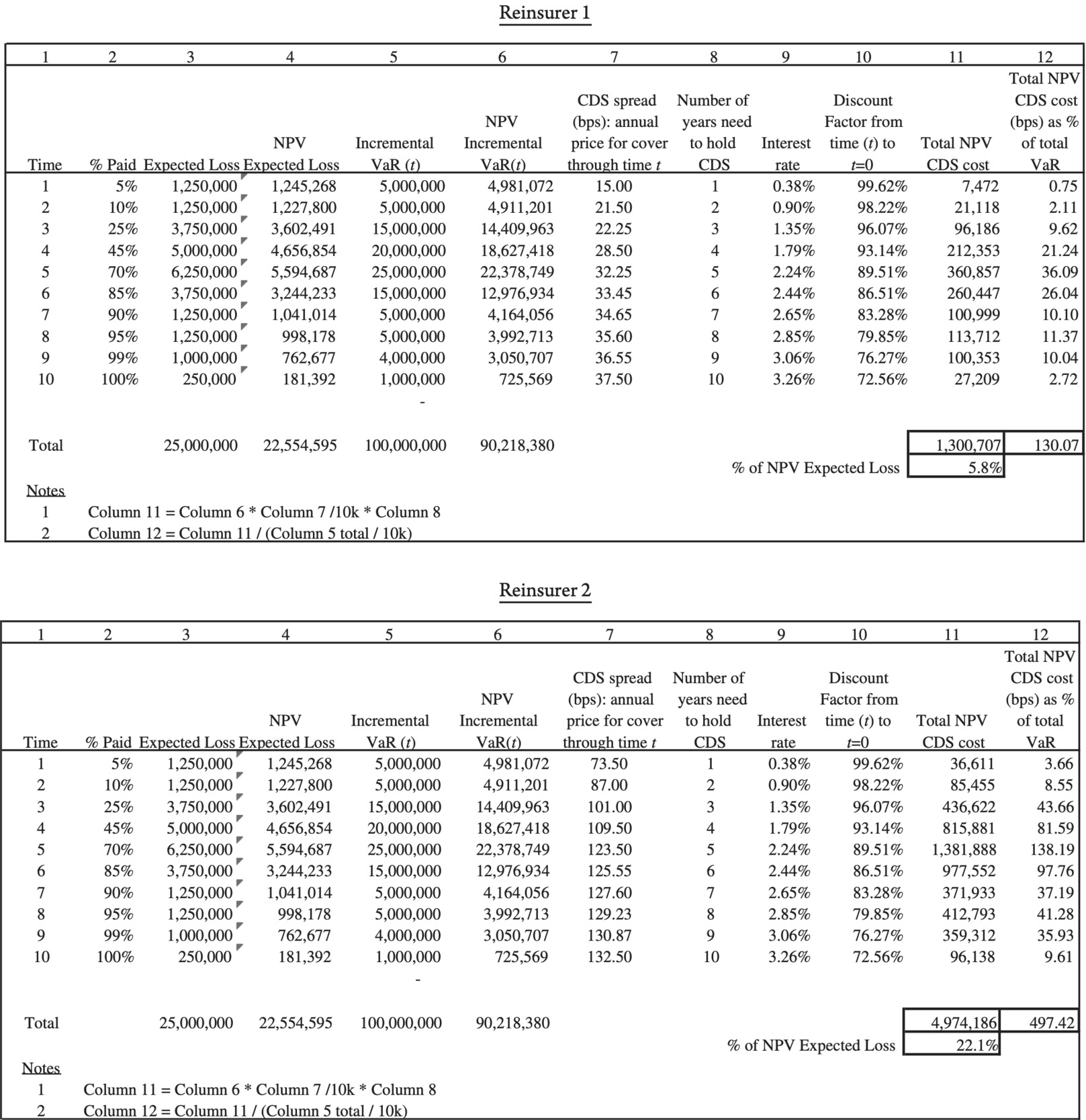

3.4. Simplified case study 4: Long-tail casualty lines of business

Until now we have simplified the problem by assuming a single year time period. What happens, however, if there is a significant lag between the time when a claim occurs and the time when the primary company pays the claim and seeks reimbursement from its reinsurer? Now one ought to calculate the cost of credit risk protection across more than a single period. When one analyzes multiple time periods, one confronts two complexities:

-

The notional amount of needed protection varies across the different time periods; the current price of CDS protection also varies for different years across the time horizon. Therefore one needs to calculate the CDS costs now for each period of the time horizon; the calculation depends upon current CDS prices and the projected payment pattern of reinsured claims.

-

Typically the buyer does not pay the entire cost of credit protection up front. Rather, the buyer pays for CDS protection each period, but these payments are contingent, not definite. The payment for each period is contingent on the fact that the reference entity (for example, the reinsurer) has not yet experienced a “credit event”; when a credit event occurs, the buyer ceases making payments. Thus the probability that the buyer makes a payment at time t is always 1-P(t), where P(t) is the cumulative probability that the entity has defaulted by time t.

In Exhibit 6, we oversimplify the analysis by treating the purchase payments as definite rather than contingent; we do so in order to focus on the key issue at hand, which is how a small difference in credit default risk per year can compound into a substantial difference over the multi-period time horizon.

In Exhibit 6, the price of credit risk is different for the two reinsurers. Although the difference in the CDS spreads is a small number in absolute terms, the accumulation of risk protection charges across multiple future years generates a significant difference between the credit risk charges of the two reinsurers. For Reinsurer 1, the total cost today of future CDS costs is approximately $1.3m or 5.8% of NPV Expected Loss; for Reinsurer 2, however, the total cost today is approximately $5m or 22.1% of NPV Expected Loss, a significant difference. Essentially this difference means that if both reinsurers quote the same reinsurance price, then the “credit risk adjusted reinsurance price” quoted by Reinsurer 2 would be significantly higher than the “credit risk adjusted reinsurance price” of Reinsurer 1.

4. Risk strategy: Hedge or retain?

4.1. Company strategy

Until now we have focused mainly on using CDS data for informational purposes, which facilitates the comparison of reinsurance prices. Should, however, a primary company actually buy CDS protection to hedge its reinsurance credit risk? Or should it retain the risk and price for it and model it and hold capital for it? Or, analogous to its handling of underwriting risk, should the company retain some reinsurance credit risk, but hedge part of it to protect against unusually large losses? In order to answer these questions, we identify five perspectives.

-

Perspective 1: “Rely on quantitative modeling and risk capital.” According to this school of thought, the firm can accurately model the risk of reinsurance credit risk and can hold capital to absorb any downside losses arising from reinsurer credit events. As a result, CDS should be used only for informational purposes for comparing reinsurance prices, but would not be needed for hedging; the company will retain the reinsurance credit risk completely. The company would need to accurately estimate the default probabilities and recovery rates for various reinsurers; the correlations of these parameters among various reinsurers; and the correlation between the company’s own losses (from both underwriting losses and asset portfolio losses) and reinsurers’ defaults.

-

Perspective 2: “Focus on the tail event.”

A proponent of this perspective notes that although the company can accurately model its reinsurance credit risk, a tail event of extreme severity will threaten the firm. Therefore the company should only worry about an extreme loss: for example, a large property-casualty event that creates large underwriting losses and simultaneously causes more than one reinsurer to fail to pay its obligations. The company ought to forego purchasing CDS protection on individual reinsurers and instead buy a custom CDS that pays off only in the joint scenario in which:

a. There is a large loss to the company.

b. Several of its reinsurers are unable to pay claims.

-

Perspective 3: “Be wary of epistemological and methodological uncertainty.” Our ability to accurately model anything complex is inherently problematical; there is a very large risk of error. Moreover, modeling the credit risk of one’s counterparty is exceptionally difficult, because one cannot truly know the types and quantities of risk exposure that a counterparty has taken upon its own balance sheet. Additionally, modeling the correlations of reinsurer defaults is quite crucial and yet highly uncertain. Therefore, an advocate of this point of view argues for some amount of hedging, even if the company judges that it has sufficient capital to retain reinsurance credit risk on its balance sheet.

-

Perspective 4: “Add value based on the theory of the firm.” A firm ought to identify the risk-taking activities in which it has a competitive advantage, leading to strategic decisions about which risks the firm wants to take and which risks are better left to others. Investors, too, construct a particular narrative (with guidance from company management) about what the firm’s core activities are, what types of risk it takes, and how the firm’s competitive advantage creates value. Therefore, even if the company can accurately model its reinsurance credit risk, and even if it has enough capital to absorb most credit risk losses, it might be preferable for the company to hedge and buy protection on all of its reinsurance credit risk, especially if it has been expanding the range of acceptable credit quality of its counterparty reinsurers.

-

Perspective 5: “Combine long-term strategy with short-term tactics.” According to this approach, a firm ought to choose a general strategy from among perspectives 1, 2, 3, and 4. Yet while the selected strategy would serve as a lodestar, the firm could deviate from it based on short-term tactical considerations. For example, a firm might choose to follow a strategy of hedging its reinsurance credit risk, stipulating that during potential short-term episodes of dislocation in the market for credit risk protection, in which the firm evaluates the market price of protection to be excessively pricey, it could choose to scale back its purchases as a short-term tactical maneuver.

Each of these perspectives suggests a different strategy for if, how, when, and to what extent the company should hedge its reinsurance credit risk.

4.2. The problem of “drift”

One additional factor should be considered in deciding whether to hedge, which is especially relevant to long tail casualty lines of business. Namely, even if the company is comfortable now with its retained level of reinsurance credit risk, will it remain comfortable in its position if the creditworthiness of its reinsurer counterparty were to “drift,” i.e., to deteriorate after the inception of the reinsurance contract? If the company chooses to hedge the reinsurance credit risk at contract inception, then the CDS hedge would protect the company if the reinsurer’s creditworthiness drifts downward in the future. On the other hand, if the company relies too much on its initial vetting of the reinsurer and chooses not to hedge, then it could find itself in a situation in which its reinsurance credit risk is higher than anticipated and is uncomfortably large in relation to the company’s risk preferences. This discussion suggests that risk of “drift” bolsters the case for hedging versus retaining reinsurance credit risk.[4]

5. Incentives

5.1. Accounting

Under U.S. statutory accounting rules, a primary company presents its loss reserves as a liability, but is allowed to deduct from this liability the losses ceded to its reinsurers. Thus the primary company presents its loss reserve liability on its balance sheet on a “net of reinsurance” basis; yet, the very existence of reinsurance credit risk highlights that receiving reimbursements from reinsurers is not a definite proposition. Treating uncertain reinsurance recoveries as a certainty tends to reduce the incentive for companies to hedge reinsurance credit risk. The statutory balance sheet does have a reduction in equity capital via the “provision for reinsurance” connected to Schedule F, but this penalty does not reflect the varying credit risk among reinsurers as judged by the credit markets; thus, statutory accounting often provides no incentive for the ceding company to distinguish between reinsurers of lesser and greater financial strength.

Under U.S. GAAP accounting rules, a primary company books its gross loss reserves and books a corresponding asset for its reinsurance recoverable.[5] This is an improvement over statutory accounting, because it explicitly disaggregates the company’s direct liability to its policyholders from the company’s right to collect reimbursements from its reinsurers. Moreover, the explicit listing of the reinsurance recoveries as an asset allows for writing down the value of this asset to reflect the risk that the reinsurers might not fulfill their promises. In theory, the financial statements showing reinsurance recoverables as an asset should be written down for the small probability that the reinsurer might not fulfill its promises; indeed, this would be the approach in a market-consistent or fair value type of system. If primary insurers had to post a reduction in the reinsurance recoverables asset even for a small risk of nonperformance, then there would be a larger incentive to measure and charge reinsurers for their variations in credit risk and, potentially, to hedge this risk. However, since current GAAP accounting does not impose this regime on insurers, there is less of an incentive for United States insurers to be concerned with these low levels of reinsurance credit risk and less of an incentive to hedge this risk.

5.2. Organizational structure

When considering incentives, one must pay attention to the organizational structure of the company. Specifically, the issue of organizational structure arises because the underwriting group, or at least one business unit within the underwriting group, seeks to purchase reinsurance for the purpose of reducing underwriting risk. Yet the company’s credit risk management group bears the responsibility of dealing with the credit risk that emanates from this reinsurance purchase. Thus we have a situation in which an action (buying reinsurance at a better price from reinsurers who are riskier) creates a benefit for one group (the underwriting group), while the downside accrues to another group (the credit risk department). As a result, the underwriting group has an incentive to push for the broadest possible range of approved reinsurers, while the credit risk group has an incentive to reduce the scope of the approved reinsurer list.

If one wanted to address this problem of non-aligned incentives, how could one do so? And would the proposal to use market-consistent quantification of reinsurance credit risk be helpful in any way?

Let’s recall Equation (3.2):

Credit risk adjusted reinsurance price =reinsurance price+cost of credit default protection.

We can rewrite this equation as follows:

Reinsurance price =Credit risk adjusted reinsurance price− cost of credit defaultprotection.

As highlighted in Equation (3.3), the proposal to use market-consistent measurement of the cost of reinsurance credit risk allows one to envision the real-world reinsurance price as the combination of two quantities:

-

The ceding company pays the credit risk adjusted (i.e., zero-credit-risk) reinsurance price to cover the underwriting indemnification.

-

The reinsurer pays back to the ceding company an offsetting discount to this full price to reflect the cost of reinsurance credit risk.

This framework facilitates the following organizational proposal:

-

The underwriting unit that enjoys the benefit of indemnification via reinsurance should pay reinsurance cost based on the zero-credit-risk reinsurance price.

-

The credit risk, as well as the offsetting price discount to reflect the cost of reinsurance credit risk, would flow to the credit risk management group.

This proposal seeks to modify the current organizational structure depicted in Exhibit 7 to a new arrangement depicted in Exhibit 8.

If, as proposed, the credit risk management unit were to receive monetary payment to reflect the reinsurance credit risk of the reinsurers, then incentives would change. The credit risk management unit could enable a broader range of reinsurers to vie for business; the question would shift away from “Does this reinsurer present an acceptably low credit risk?” and move towards the question of “Are we receiving the appropriate payment for accepting the specific reinsurance credit risk of this particular reinsurer?”

Also noteworthy is how this proposal highlights the importance of using market-consistent pricing for reinsurance credit risk. Since the credit risk department will be managing reinsurance credit risk for the company, it might choose to hedge this risk via CDS counterparties. Since the dollar outflow from the credit management group to these counterparties will be based on the market price of credit risk, it is appropriate that the credit management group take in funds for credit risk on the same basis. This symmetry ensures that if the credit risk management group decides to hedge all reinsurance credit risk, the inflow of funds will match the required outflow to pay the cost of hedging; the credit management group will match risk-based-costs and risk-based-revenues. Such an approach is diagrammed in Exhibit 8.

Further, the credit risk management group could choose to engage in active credit risk taking activities. For example, while taking in reinsurance credit risk exposure and commensurate risk-based revenues via multiple reinsurance transactions, it could choose to retain, rather than hedge, the exposure. Then, it could structure its credit risk portfolio into tranches or other efficient structures and hedge only some of this exposure. Such an approach could transform the reinsurance credit risk management unit from solely a cost center into a profit center. Since this profit-center approach to reinsurance credit risk could lead to too much risk taking and possible over-exuberance, it should be scrutinized carefully and monitored closely.

6. Market price and appraisal value

This paper has argued two main points:

-

A ceding company should evaluate reinsurance price quotes by incorporating the cost of reinsurance credit risk.

-

The cost of reinsurance credit risk can be quantified via market instruments such as CDS.

These points lead to further questions. Should market-consistent quantification be the only method for measuring reinsurance credit risk? Are there any other methods that one may use? Is the market-consistent approach better than other methods? Should there be a difference when one is measuring the cost of risk as part of a market transaction versus when one is measuring the probability of default for internal risk management purposes?

6.1. No-arbitrage pricing: Law of one price

The theory of no-arbitrage pricing indicates that it is unwise to offer to buy something at a price higher than the market price and also unwise to offer to sell something below the market price. While the technicalities of the theory may relate to the presence of active arbitrageurs in the market, the broader point transcends these mechanics: the Law of One Price indicates that prices ought not to deviate from market prices. As a result, using market price is not dependent upon believing that the market price is “correct.” Rather, even if the market price is high or low, it is incongruous to charge a price that is different than the market price. Therefore, even if a company believes that the market price of reinsurance credit risk is high or low, this would not affect how much the company should charge its reinsurance counterparties for the cost of credit risk. Similarly, the cost of credit risk that would be recorded on financial statements would be based on market-consistent pricing because of the Law of One Price. So is there any role for non-market-based views? In the next sections, we explore the role of non-market-based estimates in the following situations:

-

When making decisions about the quantity of credit risk hedging and directional risk taking for short-term tactical purposes.

-

When estimating parameters for enterprise risk modeling.

-

When the market price exhibits traits that demonstrate that it is problematic.

6.2. Appraisal value of reinsurance credit risk and directional risk taking

According to Ingram (2010), it is reasonable for any market participant to develop a multifaceted understanding of value that includes non-market-based methods, which we will refer to as “appraisal value” methods (Bodoff 2010). Doing so would be an essential starting point for any company hoping to evaluate whether the market price of risk is overstated, understated, or about right. Such an evaluation would then be crucial to determining whether the company wants to purchase more than usual or less than usual in response to price behavior. Of course, this approach only makes sense if the company believes it has an “edge” or competitive advantage over the market in accurately evaluating credit risk.

In summary, a company could choose to:

-

Evaluate reinsurance credit risk using expert analysis to determine a non-market-based appraisal value for reinsurance credit risk.

-

Compare its appraisal of the price of risk versus the market’s price of risk.

-

Determine whether or not it has an edge over the market in estimating reinsurance credit risk.

-

Determine whether the market price of risk is overstated, understated, or approximately right.

-

While the Law of One Price indicates that steps 1 through 4 would not lead the company to offer a price lower than the market, it could influence the company’s decision to take a directional position in reinsurance credit risk. For example, when the company evaluates the market price as too high, it could choose to retain more risk by decreasing the amount of credit risk protection it buys in the CDS market.

Ultimately, this type of approach would be needed if the company wanted to adopt short-term tactics to respond to changes in the market price of risk.

6.3. Market-implied parameters for modeling of reinsurance credit risk

Until now we have focused on using market information to quantify the cost of risk for evaluating reinsurance prices. Could market prices also be used to extract information about the market’s view of likelihood of default? Such an approach could lead to market-consistent estimates of key parameters for use in enterprise risk modeling.

In theory, the promise of market-implied parameters derives from the fact that we can view market price as a function of risk-adjusted likelihood of default:

Market price of risk=market-risk-adjusted probability of default∗ market estimate of loss given default.

Equation (6.1) shows that one could attempt to use market prices to infer the likelihood of default. Moreover, if this market-implied likelihood of default is different from the company’s non-market-based appraisal value of likelihood of default, then perhaps one should prefer the market-implied value. After all, one would not want to adopt appraisal values for modeling parameters that would imply a market price that contradicts the observed market price.

In reality, although one ought to use market prices for determining the cost of risk for pricing transactions, one might use a different approach when estimating parameters for enterprise risk modeling. As noted in Ahlgrim, D’Arcy, and Gorvett (2004), parameters and models that do not necessarily replicate market pricing, despite being unsuitable for pricing market transactions, may in fact be suitable for use in other situations such as insurance company enterprise risk modeling. Thus both market-implied estimates as well as non-market-based estimates of risk parameters could be useful in enterprise risk modeling.

6.4. Market price versus appraisal value: Drawbacks of market price

Given the importance of the Law of One Price, could there be situations in which market pricing is problematic, leading one to prefer an appraisal value of credit risk?

Answering this question is not a simple task. Because using market price imposes a certain amount of discipline on valuation and takes away some flexibility in placing value on risk, it can become a magnet for unfair criticism; thus one needs to carefully consider which arguments, if any, are indeed rooted in cogent logic.

For example, one criticism is that market prices are overly volatile and respond to market sentiment. Well, given that the market is attempting the difficult task of estimating the likelihood of future events, a change in sentiment about a firm’s ability to pay its future obligations should, in fact, affect the market’s estimates of likelihood of default and thus the price of the CDS. Moreover, arguments demonstrating that the market is not “efficient” do not invalidate market pricing; after all, the argument in favor of using market pricing does not derive from the Efficient Markets Hypothesis but rather from arbitrage-free pricing and the Law of One Price.

One also hears a critique that the market for CDS is not as liquid as other markets and that pricing reflects liquidity risk; the phrases “liquidity” and “liquidity risk” are sometimes mentioned without precision. Let’s assume that this means that it could take a longer time to find a counterparty to buy and sell such credit risk instruments; while this might be an important nugget of truthful information, and while this fact might affect the company’s approach to risk management, it is unclear why this fact should invalidate the Law of One Price.

Perhaps we can re-formulate the argument of “liquidity risk” in a way that better supports the argument against market price.

Let’s revisit Equation (6.1) and re-write it more granularly:

Market price=market estimate of probability of default∗ market estimate of loss given default∗ market loading for credit default risk∗ market loading for illiquidity and transaction costs.

One can argue that when liquidity ebbs, this could drive up transaction costs, as manifest in wide bid-ask spreads. Then following Equation (6.2), the market price in this situation would be higher not because of a revised view in the market of a higher likelihood of default, but rather simply because of higher transaction costs. So then following this line of reasoning, we can say that when liquidity dries up, market prices could become somewhat less valid for quantifying the cost of risk because of the problem of transaction costs; in most cases, though, the market price should be the basis for quantifying the cost of risk for purposes of pricing a transaction.

For enterprise risk modeling purposes, however, Equation (6.2) indicates why market-implied parameters may be imperfect in a broad range of situations. This is because the market price has various risk loadings, which are appropriate to be included when evaluating a market transaction, but would not be appropriate when estimating parameter values such as likelihood of default for use in simulation modeling.

6.5. Appraisal value: Methods of estimating reinsurance credit risk

Although the main focus of this paper is on market-consistent methods, the discussion in the prior section suggests that one might want to also have methods for estimating reinsurance credit risk parameters via non-market based appraisal value methods. What options are available? While a full discussion is outside the scope of this paper, some approaches include:

-

Statutory Annual Statement Schedule F

-

Rating agency information

6.5.1. Statutory annual statement Schedule F

The statutory annual statement’s Schedule F plays a role in reinsurance credit risk management and could serve as an input into quantifying risk in certain situations.

As indicated previously, Schedule F has historically played an important role because, among other things, it imposed on insurers a penalty for reinsurance recoverables from “unauthorized” reinsurers; this penalty generally extended to all of their unsecured recoverables, a very steep penalty. Recent reforms are changing this aspect of Schedule F, so that ceding companies will not receive a blanket penalty of 100% of unsecured recoverables for all unauthorized reinsurers; rather, the penalty will vary based on the reinsurer’s financial strength rating.

Overall, Schedule F credit risk penalties are rooted mainly in a regulatory solvency view rather than a forward-looking economic view. Still, like several aspects of managing an insurance company, one would need to evaluate the impact of one’s financial decisions relating to reinsurance credit risk from the standpoint of an economic risk-based view and, simultaneously, from the viewpoint of regulatory impact as well.

Could any aspect of Schedule F assist in quantifying risk on a forward-looking basis? One possibility relates to the dual aspects of reinsurance credit risk: a reinsurer’s ability to pay and a reinsurer’s willingness to pay. Market hedging instruments and market-consistent information typically relate to ability to pay (i.e., default), while they provide almost no help in quantifying reinsurance credit risk relating to willingness to pay (i.e., dispute). One might use the schedule of payments detailed in Schedule F, which are used to identify certain reinsurers as “slow-paying reinsurers,” as an indicator of which reinsurers are riskier with respect to willingness to pay. This appraisal value of reinsurance credit risk relating to willingness to pay would then run parallel to and supplement the quantification of reinsurance credit risk relating to ability to pay.

6.5.2. Rating agencies

Rating agencies such as AM Best, S, and others publish rating statistics that could be used to quantify credit risk via non-market based appraisal value methodology. As noted in Flower et al. (2007), one ought to use caution in using rating agency tables of default probabilities because they often relate to corporate default events in general, rather than applying specifically to reinsurance default. One notable example of default rates specific to reinsurers can be found in the monograph published by A. M. Best in 2011 (see A. M. Best, exhibit 5).

7. Caveats, hurdles to implementation, and areas for further research

7.1. Residual credit risk via counterparty

If a primary company were to buy CDS protection to hedge its reinsurance credit risk exposure, it would then face the residual credit risk that the counterparty provider of the CDS protection might not fulfill its promises. One way to mitigate this risk is to require the provider of CDS protection to post collateral each night based on the market movement of the CDS contract that day. In such a situation, the buyer would be exposed to no more than the one day drift in the market price of the CDS. However, the “event-driven” nature of property catastrophe risk underscores a drawback to this remedy; it is possible that a one-day movement in the CDS market price could be very substantial and thus dwarf the collateral funds previously collected via nightly collateralization. For example, on the day when a massive earthquake hits, there could be large jumps in the prices of CDS for reinsurers. The fact that the primary company had required the CDS counterparty to post collateral the previous night would not necessarily serve as foolproof protection against the new price of CDS post catastrophe. While this scenario might be unlikely, it is not impossible. In general, the purchaser of CDS ought to carefully consider the reliability of the counterparty, with emphasis on the counterparty’s financial strength being uncorrelated with property catastrophe risk.

Another aspect of counterparty credit risk to consider is the recent change in the federal regulatory landscape. Current regulatory initiatives following the passage of the Dodd-Frank law may culminate in having CDS contracts traded on exchanges with clearinghouses. Such a change could reduce the counterparty credit risk of the CDS contracts and potentially make them more attractive to buyers, although the regulations have not been finalized.

7.2. Basis risk: Bond default versus reinsurance default

A reinsurer’s default to its cedents is not exactly the same as a “credit event” that triggers a CDS payment; this imprecise alignment generates “basis risk.” Basis risk is a significant issue that one must analyze when evaluating whether or not to hedge via CDS.

One important example of basis risk would arise when a reinsurer is an operating subsidiary within a larger conglomerate; the reinsurer might default on its obligations even as the parent company is able to pay its debts, thus not triggering a CDS credit event.

Yet basis risk could be less problematic than it appears at first blush because of the interim stages that arise when a reinsurer transitions from a state of health to a state of financial distress. When a reinsurer begins to sustain financial distress of any sort, its ultimate financial health is unknowable; its debt creditors forecast an increased likelihood of default and simultaneously its customers worry about collecting their reinsurance recoveries. The worry about receiving recoveries tends to incent the companies claiming reinsurance recoverables to “take a haircut” and settle for cents on the dollar via commutation agreements; thus, uncertainty about possible ultimate future inability to pay generates definite settlement losses in the present. Simultaneously, as creditors forecast an increased likelihood of default, the market value of the CDS protection would likely increase significantly; the primary insurer can sell the CDS contract and collect the proceeds to offset the haircut loss on the reinsurance recoverables. Thus the primary insurer need not wait until the ultimate resolution of the reinsurer’s financial health; rather, when the reinsurer’s financial distress first manifests, the insurer can monetize the credit risk by simultaneously taking a haircut loss on the reinsurance recoverables and also realize an offsetting gain on the CDS position. Of course, at this early moment in the unfolding financial distress of the reinsurer, basis risk lingers: since the likelihood of bond default may be different than the likelihood of reinsurance default, the gain on the CDS could differ from the haircut loss on reinsurance recoverables. One way to address this lingering problem would be to initially forecast the behaviors of the CDS asset and the reinsurance recoverables asset and to incorporate these forecasts into the CDS buying strategy. If the insurance company buyer initially forecasts that potential future reinsurer financial distress will lead to a gain from CDS protection that will over-indemnify its loss on reinsurance recoverables, then the buyer can “under-hedge” by purchasing somewhat less CDS notional coverage than its exposure. On the other hand, if reinsurer financial distress would likely lead to a smaller gain on the CDS than the loss on the reinsurance recoverables, then the buyer ought to “over-hedge” by purchasing somewhat more notional coverage than its exposure. Finally, this entire strategy depends upon the ability to exit the position by selling the CDS, but if one could not easily sell the CDS instrument, one would need to reevaluate the effectiveness of this strategy, in which case significant basis risk could remain.

Basis risk could be reduced if the CDS protection related directly to the debt of the reinsurance operating company rather than the parent conglomerate holding company. This suggests that primary insurance companies buying reinsurance could strengthen their risk management options by encouraging reinsurance operating companies to issue (moderate amounts of) debt in order to spur creation of CDS hedges that generate less basis risk to the reinsurance credit risk protection buyer.

This analysis of basis risk and the issue of how much to over-hedge or under-hedge require further research.

7.3. Basis risk: Priority of payments and recovery rates

Another source of basis risk relates to recovery rates and priority of payments. When a default occurs, creditors can often recover some portion of their claims against the defaulting company. Some classes of creditors recover a larger share of their loss than other creditors; the recovery rate varies based on the creditor’s priority in receiving payments. An example of various recovery rates across different categories of bonds can be found in Hull (2000) Table 1.

A ceding company acting as creditor seeking reinsurance reimbursements from a financially distressed reinsurer may have different priority in different legal jurisdictions; this would likely affect the projected recovery rate on the reinsurance recoverables. Meanwhile, the CDS hedge would typically pay based on the recovery rate for a senior unsecured bond, which could be different than the recovery rate for reinsurance. This discrepancy in recovery rates introduces basis risk between bond default and reinsurance default. One way to address this problem is to project the recovery rates for bond default and reinsurance default in order to suitably modify one’s CDS purchase. For example, since the reinsurance recovery rate might be higher than the bond recovery rate, the overall loss to a reinsurance creditor should be less than the loss to a bond creditor; this would suggest that a reinsurance creditor should under-hedge by purchasing an amount of CDS protection that is less than 100% of the notional exposure.

This analysis of basis risk and the issue of how much to over-hedge or under-hedge require further research.

7.4. Willingness to pay

Sometimes the reinsurer is able to pay but is unwilling to pay because of a disagreement about whether the reinsurance contract covers the disputed claims or not. In this situation, CDS will not help the buyer of the protection. Therefore, if an insurance company chooses to use CDS to hedge reinsurance credit risk, it would still need to evaluate the claim payment practices and trustworthiness of potential reinsurer counterparties, and it would also still need to scrutinize its contract wording in order to reduce the likelihood of claim disputes.

As noted in section 6.5.1, one could attempt to use non-market based appraisal value to estimate the likelihood of credit risk arising from disputed claims, perhaps via data in Schedule F identifying slow-paying reinsurers.

7.5. Other practical considerations

CDS prices can be volatile. This could introduce operational complexity, because the process of transacting a reinsurance purchase can take a significant amount of time. During the process of buying reinsurance, the CDS prices and thus credit risk charges relating to some reinsurers might change. If there is significant time lapse between evaluating reinsurance quotes and signing the reinsurance contract, then the volatility of market pricing could cause operational challenges.

Another practical problem is that there may be no active CDS market for some reinsurers. One solution to this problem would be for the primary company to not approve a reinsurer whose credit risk cannot be easily measured and hedged. Or the company could choose to do business with such a reinsurer by evaluating the risk charge based on other non-market based methods. In addition, the primary company would need to acknowledge that it could not hedge its exposure to these reinsurers even if it desired to do so, which would then require the ceding company to apply more substantial credit risk charges against these reinsurers when evaluating their quoted prices.

8. Conclusion

This paper proposes that property-casualty insurance companies should deploy a new framework in managing reinsurance credit risk. The proposal advocates using market-based information to quantify the cost of reinsurance credit risk; doing so facilitates the evaluation of the trade-offs of different price quotes from multiple reinsurers of varying creditworthiness. Applying such a framework would assist companies to more accurately measure the cost of reinsurance credit risk and make better decisions relating to purchasing reinsurance and to measuring and managing risk.

This greater risk could relate to the reinsurer’s likelihood of default, for example, if a reinsurer has a low credit rating, or this greater risk could relate to the potential severity of loss, for example, if the company has a concentrated exposure to a particular reinsurer.

For background, see D’Arcy (2009) and Merrill Merrill Lynch (2006)

The following case studies make certain simplifications. The first simplification is to assume for brevity’s sake that price quotes from reinsurers are presented as final offers from which the reinsurers will not budge. The second simplification is that all reinsurers quote their prices, as is common practice, under the stipulation of “best market terms.” This assumption means that reinsurers who participate on a transaction do not do so at different prices; rather, a single market clearing price applies to the deal and all the participating reinsurers receive that price.

A counterargument notes that a company buying reinsurance typically requires that the reinsurance contract contain a “special termination clause.” The special termination clause states that if the counterparty reinsurer’s creditworthiness drifts downward below some crucial threshold, then the ceding company may take corrective action: for example, demanding that the reinsurer post collateral for unpaid obligations such as incurred but unpaid reinsured claims. Essentially one of the fundamental features of the special termination clause is this “contingent collateral call”; but there are significant problems with a contingent collateral call. The first problem is that the ceding company is seeking a redress via its direct counterparty, but the counterparty is already financially weakened and in no position to provide financial remedy; seeking compensation from a third party (such as a CDS protection provider) would be more reliable. The second problem is that the strategy of relying on special termination suffers from “competitor neglect”; namely, it fails to anticipate that all of the other ceding companies who bought reinsurance from this reinsurer will simultaneously seek to execute their own rights under the special termination clause. When all these demands fall on the reinsurer, it is unlikely that the reinsurer can make good on all of them. So at best, the special termination clause will be ineffective at solving the problem it was intended to solve; at worst, it can exacerbate the situation by being pro-cyclical and causing a situation that is far worse [such as a feeding frenzy of claimants that destroys the viability of the reinsurer]. These problems ought to be eminently imaginable on a prospective basis; or, in the alternative, one can examine various episodes that occurred during the financial panic of 2008–2009 that show the destructively pro-cyclical problems created by contingent collateral calls. In the author’s view, the insurance industry has not sufficiently appreciated this applicability of the lessons of the financial panic of 2008–2009.

A similar approach appears in the statutory Schedule F Part 8.